August 18th, 2015 by Elma Jane

NFC stands for near-field communication, it allows two devices to share data.

You’ve likely used it already, even if you haven’t realized it. It’s embedded in computer cards, print ads, smart cards and it is featured in many Android phones, Windows phones and the new iPhone.

NFC works in two ways:

The first is two-way communication, where two devices can read and write each other – like transferring contacts or photos from one device to another. The second is one-way communication where a device can read and write to an NFC chip – similar to using an NFC enabled card to pay for something using an NFC terminal.

Sure there are other technologies, like Bluetooth, that can do things similar to NFC, but NFC uses less power and is better for your smartphone’s battery life. NFC is also less complicated to use than Bluetooth and doesn’t need to be paired with anything.

NFC is extremely secure. Intercepting payment information from an NFC device is very difficult because of how the process works. To use NFC for payments, the payment application is first launched on a phone that is then tapped on a terminal. The customer then enters a code or scans a fingerprint to approve the transaction. A secure element (SE) then authorizes the payment and sends the information to the NFC modem. The payment is then processed like a credit card swipe.

NFC is likely to continue to grow in popularity in the mobile payments space, to learn more about NFC payments and how you can prepare your business with National Transaction Corporation, visit www.nationaltransaction.com or give us a call at 1-888-996-2273

Posted in Best Practices for Merchants, Near Field Communication Tagged with: credit card, Mobile Payments, Near Field Communication, nfc, NFC payments, payments, swipe, terminal

July 23rd, 2015 by Elma Jane

The digital payments landscape is changing at a rapid pace. Consumers are finally adopting digital wallets, like Apple Pay and Android Pay.

The deadline for merchants to become EMV compliant, the global standard that covers the processing of credit and debit card payments using a card that contains a microprocessor chip, is quickly approaching.

Today’s consumers show an increasing desire to use new payment methods because they’re convenient. However, this presents a challenge to merchants, as many have not made the switch to the modern technology required to accept these methods since they’re generally hard-wired to resist technology changes.

Merchants must evolve with technology or they’ll find themselves unable to compete and in danger of losing customers.

Looking long term, the benefits of adopting new payment technology will outweigh the cost of transitioning. The fact is that new payment technology will reduce fraud risk due to counterfeit cards, provide greater insight into shoppers with sophisticated data and will ultimately lower costs for merchants over time.

The value merchants will get out of new payment methods:

Security

Investing in new payment technology will help reduce the risk of fraud. EMV, as an example. Beginning in October 2015, merchants and the financial institutions that have made investments in EMV will be protected from financial fraud liability for card-present fraud losses for both counterfeit, lost, stolen and non-receipt fraud.

EMV is already a standard in Europe, where fraud is on the decline. In turn, American credit card issuers are being pressured to replace easily hacked magnetic strips on cards with more secure “chip-and-PIN” technology. Europe has been using Chip, and Chip & Pin for years.

There’s nothing that can guarantee 100 percent security, but when EMV is coupled with other payment innovations, like tokenization that separate the customer’s identity from the payment, much of the cost and risk of identity theft is eliminated. If hackers get access to the token, all they get is information from one transaction. They don’t have access to credit card numbers or banking accounts, so the damage that can be done is minimal.

As card fraud rises, there’s a strong case to upgrade to a payment system that works with a smartphone or tablet and accepts both EMV chip cards and tokens.

Insight into Customer Behavior

In addition to added security, upgrading to new payment technology opens up a door to greater customer insights, improved consumer engagement and enables merchants to grow revenue by providing customers with receipts, rewards, points and coupons. By collecting marketing data at the point of sale a business can save on that data that they only dreamed of buying.

Investment Outweighs the Cost

New technology does have upfront costs, but merchants need to think about it as an investment that will grow top-line revenue. Beware of providers offering free hardware. Business can benefit by doing some research on the actual cost of the hardware.

By increasing security, merchants are further enabling mobile and emerging technologies, which will make shopping easier.

Customers will also be more confident in using their cards.

As an added bonus to merchants, most EMV-enabled POS equipment will include contactless technology, allowing merchants to accept contactless and mobile payments. This will result in a quicker check-out experience so merchants can handle more transactions.

Faster customer checkout.

The best system for is the one that makes the merchant as efficient and profitable as possible, as well as improves the customer checkout experience.

Retail climate is competitive, merchants have two choices:

Do nothing or embrace the fact that payments are changing. Transitions from old systems to new ones require work and risk, but merchants who use modern technology are investing in the future and will certainly outperform those who choose to do nothing.

Posted in Best Practices for Merchants, EMV EuroPay MasterCard Visa, Mobile Payments, Near Field Communication, Point of Sale Tagged with: American credit card, card, card present, chip, Chip and PIN, contactless technology, credit, data, debit card, digital payments, Digital wallets, EMV, EMV compliant, EMV EuroPay MasterCard Visa, merchants, Mobile Payments, payment innovations, payment methods, payment technology, payments, point of sale, POS, provider's, smartphone, tablet, token, tokenization, transaction

July 7th, 2015 by Elma Jane

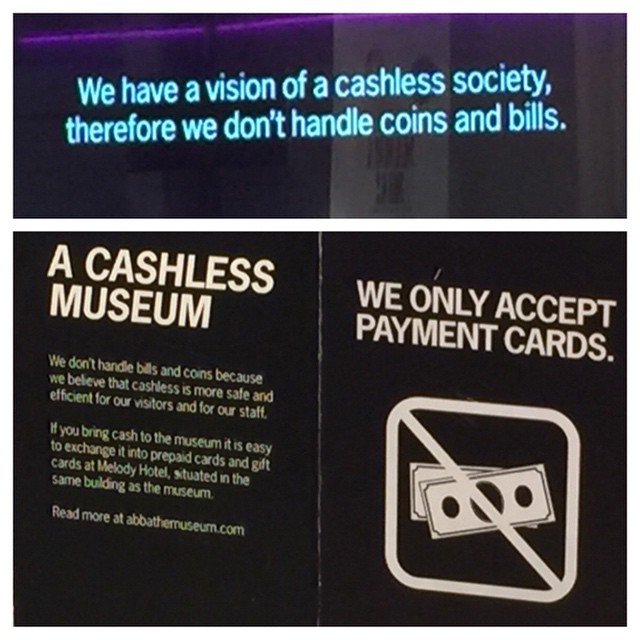

Cashless society is about to happen, hard to believe for some. We are all unable to decide on the edge of a new, cashless world where mobile payments reign supreme. If so, is this a bad thing? For some people yes, because for them change can be scary.

Every revolution needs a good crisis in order to grow its seed. The cashless revolution is the same. Current global financial conditions serves as the potential crisis, and truly the cashless revolution is upon us. Society is on the brink of great economic change, which will likely usher in a new era of worldwide, electronic currencies. The cashless society is coming.

Advances in mobile payment options as evidence of this impending cashless society, consider the practical benefits of mobile payments for the consumer. The most obvious is convenience. Many people prefer to swipe their smartphone atop a scanner to carrying around a stack of cash. Electronic payments are traceable, which is useful for tracking one’s spending and can add a sense of security. Also, carrying around large stacks of cash isn’t always feasible or safe.

Mobile payments also offer interested individuals a way to incorporate social media into their purchases; they can check-in to a site and tell all their friends about an exciting new product they bought, or announce their presence at a new coffee shop, all with that same initial swipe of an NFC-enabled phone. Add to this the many practical benefits of mobile payments as far as business owners are concerned, and it’s easy to see why so the technology is becoming so widespread.

And yet for all the benefits of mobile payments and point of sale technology, the two don’t necessarily exclude cash. Other company focuses on blending cash transactions with POS. This allows technologically savvy businesses to incorporate POS and mobile payment technology into their business, without excluding potential customers who prefer to use cash.

We aren’t necessarily evolving towards a cashless society, but towards a society with a plethora of payment options. POS technology is all about options. Want to pay with a swipe of your credit card? Swipe your credit card. Want to tap your NFC-enabled phone against a console. Tap and go. Want to pull a crisp twenty-dollar bill from your wallet and walk away from the counter with milk and eggs in your hand and a handful of coins jingling in your pocket? Go for it.

The question is: Will we ever become a truly cashless society? Maybe, maybe not, but as mobile payments become increasingly common, cash may very well fall into the retro category.

Posted in Best Practices for Merchants, Mobile Payments, Near Field Communication, Point of Sale Tagged with: credit card, electronic currencies, electronic payments, Mobile Payments, nfc, point of sale, POS, swipe

June 26th, 2015 by Elma Jane

As you can tell from the name, Android Pay playbook is remarkably similar to Apple Pay. Android Pay will use an on-board Near Field Communication (NFC) chip and tokenization services from the major networks to deliver a token from the phone to an NFC-enabled point of sale. Just like Apple Pay. Android Pay is supported by more than 700,000 merchant locations and Android Pay will provide APIs for app developers to take in-app payments from the on-board wallet. Both Apple Pay and Android Pay have fingerprint scanners on phones, you can enable payments with just a fingerprint scan.

While details are barely sufficient, rumor has it Google won’t charge banks a fee as Apple does on the transactions and that’s the difference. Additionally, technical differences in the operating systems underlying the payment system exist, but they won’t affect how every day users experience the system. Android Pay will suffer a slower upgrade path than Apple Pay, due to the lack of hardware support for the newer operating system (it can take Android twice as long to get users upgraded).

There is no war between Apple and google. NFC won the war! We are seeing all of the armies gather together under its flag. As consumers, we love to see better products. When it comes to payments, we need standards and reliability.

With the alignment of the two operating system platforms on NFC, on user experiences like fingerprint unlocking and on both in-app and retail payments, consumers, retailers, and app developers can build an ecosystem we can all understand. Credit cards work great because they are ubiquitous. Everyone can use them everywhere, and every retailer has incentives to be a part of the system.

An NFC-based mobile payments experience will have this same effect. Over the next five years more and more retailers will add NFC-capable terminals. More phones will be fully capable of NFC payments with fingerprint sensors. More consumers will carry those phones.

So if it’s not a war, are there any losers? Companies focused on plastic cards, but not NFC. Transitory technologies like Samsung Pay’s MST (magnetic secure transmission) also have a strong transition period as they enable payments at non-NFC enabled terminals. MST (magnetic secure transmission) is a strong player because the user experience is very similar (hold a phone to a reader), even if the technical method is not the same.

Posted in Best Practices for Merchants, Near Field Communication Tagged with: banks, chip, credit cards, merchant, Mobile Payments, Near Field Communication, nfc, NFC payments, NFC-capable terminals, NFC-enabled, payment system, payments, point of sale, tokenization

June 15th, 2015 by Elma Jane

Merchants Provided Access to Digital Payments Innovations for Store-Branded Cards through Partnerships with Synchrony Financial and Citi Retail Services

Purchase, NY – June 15, 2015 – MasterCard today became the first payment network to provide tokenization services to private label (store-branded) credit card issuers, enabling merchants to take advantage of the latest digital payment innovations. BJ’s Wholesale Club, Kohl’s and JCPenney will be among the first retailers to bring mobile payments to their private label cardholders later this year. The company also announced partnerships with some of the largest private label credit card issuers in the U.S., including Synchrony Financial and Citi Retail Services, to enable consumers to use their eligible credit cards within participating mobile payment and digital wallet services.

According to Equifax’s National Consumer Credit Trends Report, the number of open retail credit card accounts exceeded the 195 million mark by the fall of 2014. As the only network to offer private label support for wallet service offerings, MasterCard continues to enable consumers to pay when, where and how they want – and on the device of their choice.

Tokenization support for private label issuers is made possible through the MasterCard Digital Enablement Service (MDES), which enables a connected device to be securely used for everyday shopping and payments. MDES supports contactless (NFC) payments with a mobile device at a physical point of sale, as well as from within a mobile app. Transactions are secured using industry-standard EMV cryptography and take full advantage of the most secure payments technology in the world.

“Thanks to our ongoing innovation and strategic partnerships, we are helping shape the future of how private label credit cards work in whichever digital wallet customers choose,” said Margaret Keane, president and CEO of Synchrony Financial. “It was recently announced that our retail partner, JCPenney, will be among the first to offer its private label credit cardholders the ability to checkout with Apple Pay later this year. We are committed to working with our retail partners, MasterCard, and key payments industry players to preserve the benefits of our private label credit cards and patented Dual Cards in third-party digital wallets.”

“We’re seeing significant momentum and innovation around digital wallets, and a key focus for MasterCard is that consumers can leverage these new offerings safely and securely. MDES was developed to ensure that any connected device can be used to make purchases, and deliver the simplicity, security and convenience people have become accustomed to when using a MasterCard account of their choice,” said Ed McLaughlin, chief emerging payments officer, MasterCard. “MasterCard is helping merchants capitalize on mobile payments, ensure the best possible consumer experience for their consumers and encourage both repeat business and customer loyalty.”

Since the announcement of MDES in 2013, millions of MasterCard accounts have been tokenized for use in popular digital wallet services. MDES currently provides tokenization services for credit, debit, co-brand, prepaid and small business cards, with private label tokenization beginning in the third quarter of this year.

Posted in Best Practices for Merchants Tagged with: credit cards, digital paymets, Digital wallets, merchants, Mobile Payments, payment network, technology innovation, tokenization

January 12th, 2015 by Elma Jane

Mobile Point of Sale (POS) systems have rocked the retail world and the trending topic when it comes to POS is all about the mobile kind. When one searches the term POS, nearly every article that comes up is all about mobile, and many seem to believe it will change the retail industry.

Is traditional POS on its way out? Not so fast.

While mobile POS is indeed a hot topic, it is likely to be an enhancement, rather than a replacement, to traditional POS

There is definitely a need and a place, for both.

Everyone was certain that dot.coms would eradicate brick-and-mortar stores; they are still alive and well, and traditional brick-and-mortar stores have, like traditional POS, embraced the Internet and allowed it to serve them in the capacity of extension.

Retailers everywhere have incorporated the Internet into their business model by creating multi-channel sales strategies, such as e-commerce, digital marketing, social media marketing, online product information, specifications, reviews and online customer service.

In addition to their online presence, these same retailers have started to bring the Internet in-house by integrating such services as customer centric promotions at point of sale, introducing loyalty programs and member registration, facilitating digital signage, offering e-receipts via email, and self check out centers; all at the traditional POS kiosk.

Why bother with mobile POS anyway?

While it is true that traditional POS systems won’t be going anywhere soon, and with good reason, mobile POS systems have allowed retailers to make great strides when it comes to efficiency and customer service, as well as customer satisfaction.

Since the advent of Mobile POS, companies have made big changes in the way they handle customer transactions in-store, thus affording faster checkout, waiting line reduction, consultative selling, and more.

The list of mobile POS benefits goes on and on:

Email Receipts: Better for the environment, more convenient for customers and faster to process. A digital purchase receipts sent via email tells the customer that you care about the earth and about them.

Expanded Reach: With mobile POS, your sales are no longer confined within the four walls of your brick and mortar store. Sidewalk sales, seasonal mall kiosks, and special sponsorship events are just a few examples of all the places you can take your retail sales to, with a POS in hand.

Inventory and Price Search: When customers can be assisted with finding an item color, size or availability on the spot, rather than having to wait in line to do so, it makes them happier. The same can be said for pricing. POS in the hands of store reps can go a long way toward customer satisfaction.

Inventory Return Stations: There is always a certain volume of returns, but that volume increases for retailers particularly after the holidays. The implementation of mobile POS allows for retailers to set up additional return stations in order to avoid long lines and customer frustrations.

Mobile POS goes Mobile: Your investment in your company POS system doesn’t need to be one size fits all, regardless of store traffic volume in one location or another. Retailers may opt to have a blow out sale in one location, thus require additional checkout power for that location for a specific period of time. With mobile POS, devises and licensing can be utilized throughout different store locations on an as needed basis.

Optional Seasonal Subscription: The great thing about mobile POS is that you needn’t pay for a POS system year round if you’re not using it year around. Seasonal spikes in retail sales warrant the additional cost of extra POS licensing and hardware, but the rest of the year your budget shouldn’t need to encompass more than what is needed. Mobile lets you better manage your overall POS investment.

Storewide Promotion Opportunities: Mobile POS has allowed retailers to drive sales in various sections of the store by holding demonstrations or promotions in different departments to tout products or services. Customers can be marketed, and sold to, on the spot.

The growing industry of mobile payments doesn’t stop at in-store mobile POS. Digital wallets like Google Wallet and Apple Passbook, mobile-to-mobile cell phone transfers, Near Field Communication (NFC) payments, mobile device credit card swipe and other emerging technologies are quickly changing our cash and credit card world.

What about traditional POS?

Mobile payment systems are indeed terrific. So, when should you consider going with traditional POS? The reality is, in addition to the aforementioned benefits of traditional checkout kiosk functions, there times when mobile POS simply will not suffice.

Mobile POS is great when a customer wants to choose and pay for one item while on the sales room floor, but what about when the customer has a multitude of items? Ringing up and bagging groceries, removing anti-theft mechanisms, neatly folding and bagging clothing items and managing the sales of numerous agents, stations or departments are just a few examples of situations that often require the traditional POS checkout station.

By combining traditional POS strategies with mobile POS flexibility, retailers can leverage the command of a complex, and multi-dimensional, marketing and retail sales management system.

Posted in Best Practices for Merchants, Mobile Payments, Mobile Point of Sale, Point of Sale Tagged with: brick and mortar, credit card swipe, credit-card, customer service, digital marketing, Digital wallets, e-commerce, mobile device, Mobile Payments, mobile point of sale, mobile pos, multi-channel, Near Field Communication (NFC), POS, retail industry, social media

October 13th, 2014 by Elma Jane

Non-cash payments volumes are expected to increase by nearly 10% percent to reach 366 billion transactions in 2013, fueled by strong growth in developing markets and mobile payments.

Overall, more than half of global non-cash payment growth comes from developing countries despite them only making up one quarter of the market size at 93 billion transactions. China remains a relatively underdeveloped market for non-cash transactions but its population and growth rate suggest in certain conditions that it could soon outstrip the US and Euro-zone within the next five years.

China is one to watch over the coming years, with the report showing that if growth rates remain at the current high level, it could become the largest market for non-cash transactions within just five years. These soaring growth rates in key markets put pressure on the global payments arena to innovate to meet rapidly increasing consumer demand.

Increased use of tablets and smartphones is creating a convergence of e- and m- payments, posing new challenges for Payments Services Providers (PSPs). In 2015, m-payments are projected to grow at 60.8% while e-payments growth is forecast to decelerate to 15.9% annually over the next year, as more people use mobile devices to make payments.

This trend is adding to the pressure on PSPs to modernize their payments processing infrastructures, ideally based around a single integrated payments platform for corporate and retail payments and a central hub.

The growth of the industry coupled with the fast pace of new regulation requires flexibility from PSPs to adapt, initiatives such as real-time payments, pressure on card interchange fees and improved payments governance as examples of cascading regulation.

Posted in Best Practices for Merchants Tagged with: card, card interchange fees, consumer, e-payments, global payments, m-payments, Mobile Devices, Mobile Payments, Non-cash payments, payments platform, payments processing, Payments Services Providers, psps, real-time payments, retail payments, Smartphones, tablets, transactions

September 15th, 2014 by Elma Jane

Visa has taken advantage of the hoopla surrounding Apple’s application of digital account tokens to replace card numbers for online and mobile purchasing by initiating the roll out of its Token Service to US clients.

Visa Tokens will be made available to issuing financial institutions globally, starting with US banks next month, and followed by a phased roll-out overseas beginning in 2015. The technology has been designed to support payments with mobile devices using all major mobile platforms.

More than 750 staff from across the Visa organisation globally were involved in the effort, working closely with initial launch partners – financial institutions, merchants and processors to ensure the ecosystem was ready. Today, Visa is making these services available and believe it will help transform connected devices and wearables into secure payment vehicles.

Visa Token Service replaces sensitive payment account information found on plastic cards with a digital account number or token. Because tokens do not carry a consumer’s payment account details, such as the 16-digit account number, they can be safely stored by online merchants or on mobile devices to for e-commerce and mobile payments.

The release of the service has been given added urgency by a spate of successful hacks on merchant card data stores, such as the recent plundering of card account data at Home Depot and Target.

MasterCard has its own equivalent Digital Enablement Service, which will be released outside of the US in 2015.

Posted in Best Practices for Merchants, Credit Card Security, e-commerce & m-commerce, Mobile Payments, Visa MasterCard American Express Tagged with: account details, card, card account data, card data, data, digital account, digital account number, e-commerce, financial institutions, MasterCard, merchant card data, Merchant's, mobile, Mobile Devices, Mobile Payments, mobile platforms, online merchants, payments, processors, Token Service, tokens, visa, Visa organisation, Visa Token Service, wearables

July 21st, 2014 by Elma Jane

PayPal has begun testing a new loyalty program called PayPal Select that seeks to promote use of the digital-payments network by offering more rewards for its most active members. The program launched by invitation only based on users’ history on PayPal and follows by about 18 months the cancellation PayPal’s previous loyalty program, PayPal Advantage. As PayPal looks to continue to build its volume of use on mobile devices off of eBay, driving repeat use and loyalty will be key. The challenges for the offer part will be the same as any other deal/offer program – namely the quality of the offers and inbox-offer fatigue. Like any big-screen concept that gets downscaled onto mobile, there is the challenge of how to hook people in the first couple of screens. CreditCall is not involved with PayPal Select. The payment platform is a division of San Jose, CA-based online auction giant eBay. It offers both a mobile app and an m-dot site for mobile payments.

Posted in Mobile Payments, Smartphone Tagged with: CreditCall, digital-payments network, ebay, loyalty program, m-dot site, mobile, mobile app, Mobile Devices, Mobile Payments, PayPal, PayPal Advantage, PayPal Select, rewards

June 10th, 2014 by Elma Jane

David Marcus, president of eBay Inc.’s PayPal division, plans to leave the payments company to join Facebook Inc. The move is effective June 27. Marcus will oversee the social network’s messaging products division, including the Facebook Messenger app, which lets users send messages to their friends. Marcus had been in his position at PayPal since April 2012. Prior to working for eBay, he was founder and CEO of Zong, a mobile payments provider for gaming and social networking companies that eBay acquired in August 2011. As the head of PayPal, David helped make a great business better, reinvigorating product design and innovation and energizing the team to deliver compelling consumer experiences. Making the move was a difficult decision, Marcus writes in a Facebook post. After much deliberation, I decided now is the right time for me to move on to something that is closer to what I love to do every day. Facebook says it processes 12 billion messages daily and its Messenger smartphone app which consumers can use independently of Facebook even though it is integrated with the social network has more than 200 million users. We’re excited by the potential to continue developing great new messaging experiences that better serve the Facebook community and reach even more people and David will be leading these efforts. Marcus will oversee the social network’s messaging products division, which includes Facebook’s Messenger app. The mobile app has more than 200 million users.

Posted in Uncategorized Tagged with: eBay Inc., Facebook Inc, Facebook Messenger app, Messenger smartphone app, mobile app, Mobile Payments, mobile payments provider, payments company, PayPal, smartphone app