Merchant Aggregators, Merchants of Records and Payment Service Provider what’s the difference?

Payment Service Provider – is a company, which provides payment gateway and related services (like antifraud tools) to merchants. PSP is a representative of one or several acquiring banks. The merchant signs an agreement with the acquiring bank and PSP. The acquiring bank provides a merchant account and secures settlements for merchant’s transactions directly to the merchant’s bank account. Payment Service Provider secures delivery of the merchant’s transactions to the acquiring bank and some related services like fraud scrubbing and recurring transactions. The merchant has an own merchant account with this model.

Merchant Aggregator – is a company, which uses one merchant account to process transactions from many merchants. Merchants don’t have any agreements with an acquiring bank, but with the merchant aggregator. You get quick setup and get shut down quickly. Most aggregators are hard to get hold of, they don’t have human customer support. The problem with this model is, it’s not intended as a long-term, scalable solution to accepting payments and they can freeze your account or hold your money if anything unusual happens.

Merchants of Record – are a merchant, who use services of payment service provider (PSP) or merchant aggregators to accept payments on their websites for goods or services they sell. Merchant of record role requires an array of administrative responsibilities, such as managing a merchant account with a payment processor, paying associated credit card rates & fees for the transactions and other responsibilities like complying with PCI DSS Standards.

Merchant account services can help you focus more on your business operations and identify flaws in your business. They can also help you manage your business finances and help you improve operations, while cutting down on costs. Not accepting credit cards can hurt your bottom line. Having a merchant account can help you make more money.

Not accepting credit cards can hurt your bottom line

Businesses that don’t accept credit cards are missing out on a lot of business. Credit cards offer convenience and rewards, and most customers prefer them to cash. Not only does this mean more business, it also protects your business from fraudulent charges. Lastly, by accepting credit cards, you don’t have to worry about handling cash, which makes it less tempting for thieves.

If you have decided not to accept credit cards for your business, it is important to remember that you need to have a merchant account to receive credit card payments. This account holds the money you collect from customers. However, you may have been reluctant to accept credit cards because you think you don’t need them or don’t want the added hassle of accepting them.

Many customers are switching to cashless payments, particularly high-income consumers and people under 45. According to the Federal Reserve’s 2022 Diary of Consumer Payment Choice, cashless payments will account for 57% of all consumer payments in 2021, 55% in 2020, and 53% in 2019. The trend is even more prominent among high-income consumers and those under 45.

Not accepting credit cards can also hurt your business’s bottom line. Instead of storing cash, credit card payments go directly into your bank account and can be integrated with your accounting software. Additionally, the security of holding large amounts of cash is a huge concern, and businesses may lose money if a thief tries to steal the money. Businesses that accept credit cards may also have an established customer base.

If you run a small rural business without access to credit cards, you’re missing out on a lot of customers and profits. It’s estimated that businesses in rural areas are losing billions of dollars every year because of their inability to accept credit cards. This is partly because of poor internet connection or other issues. However, there are affordable credit card processing options available that help businesses accept more customers and boost their profits.

Getting approved for a merchant account

There are many things to consider before getting approved for a merchant account for your business. First of all, you must have the proper documentation to back up your business. This will include financial statements, business bank account information, and routing numbers. Some merchant account providers will also require you to provide a business license.

Having a good credit history is also essential. You should work to improve your credit rating and eliminate any past credit issues. To get your credit report, you can get a copy from TRW or the major credit agencies. If you have any negative items on it, you should ask the company to remove them. By maintaining good credit, you can increase your chances of getting approved for a merchant account for business.

After researching different merchant account providers, you should make an informed decision. Make sure to choose one that offers the right payment services and features for your business. For example, some merchant account providers have specific features for specific industries and specialize in certain types of transactions. You should do some comparison shopping online and get recommendations from people in your industry. You can also try looking for a merchant account provider through a bank. Banks may offer merchant accounts to new business owners, and they are usually more willing to approve them.

When choosing a merchant account provider, it is important to understand that the fees and rates they charge will be deducted from your business funds. It is also important to consider the quality of customer service you receive from your merchant account provider. If you find a company that provides poor customer service, move on to another provider.

Before choosing a merchant account provider, you should compare the fees, hardware costs, customer support, and contract length. The standard merchant account contract is three years, but you should compare terms and penalties before signing a contract. In addition, make sure your prospective processor provides you with clear answers to all your questions, including how long the approval process will take. You should avoid any merchant account provider that makes promises you can’t keep. Get all your paperwork in order.

If you have an online store, a merchant account provider can help you set up the payment processing system. The merchant account provider will need information about your business, and may also need a credit card number to make automatic deposits. Make sure you review the terms and conditions and the PCI data security standard before signing any paperwork.

Choosing a merchant account provider

Choosing a merchant account provider is an important decision for your business. It can have a significant impact on the rate you pay and the quality of service you receive. Choosing the right one can also help you gain a competitive edge. Here are some tips to keep in mind when choosing a merchant account provider.

– Choose a merchant account provider that offers a variety of payment options. Online businesses need a merchant account provider that supports the variety of payment methods you accept. If you only accept cash, you may want to opt for a cashback system. This will reduce the need for clients to make an in-person trip to the ATM and incur additional fees. Alternatively, you may want to choose a provider that offers ACH processing. In either case, it’s important to consider future funding needs.

When choosing a merchant account provider, you should also consider the fees that come with their services. Some merchant account providers may charge monthly minimums. This is not ideal if you plan to only sell items during certain seasons. You should also take into account the annual PCI Compliance Fee and early termination fees. While this may seem like a small fee, they can add up.

Lastly, don’t be afraid to ask questions. Ask about their fees and the kind of processing they offer. A merchant account provider should be able to answer any questions you have. A good account provider should be flexible and responsive to your needs. Your business is different, so you need a service that will be best suited to it.

A merchant account provider’s fees can vary significantly, so it’s important to compare them side-by-side. It’s important to look for a fee structure that is transparent and fair. Lastly, choose a merchant account provider that’s ethical. If you choose an unreliable merchant account provider, you’ll face ongoing account maintenance and other fees that may be unavoidable.

Merchant account providers provide the services that enable businesses to accept credit card payments. They store the money from customers and process it for the business. They also provide services such as PCI compliance and customer service. There are many different types of plans available. You should compare these to determine the best fit for your business.

Setting up a merchant account with low rates and fees

Many merchant services providers offer low rates and free trials, so you don’t have to worry about paying thousands of dollars for a merchant account. These services let you accept credit card payments online and through invoicing. While free accounts may be the most attractive option for new businesses, many established businesses also find lower-cost alternatives.

When applying for a merchant account, you should carefully review the contract with the service provider. Some providers have hidden fees and long-term contracts. They also often charge a cancellation fee if you decide to cancel the account. To ensure that you have the lowest fees and lowest risk, read the terms and conditions and ask questions before signing on the dotted line.

Merchant accounts should be PCI compliant. This means the provider must have strong security measures and protect sensitive customer data. Additionally, a good merchant account provider should offer fast funding options and 24-hour in-house support. You can also choose a provider that offers an all-in-one solution.

A merchant account is a vital part of a business’s infrastructure. It allows it to accept payments by credit cards from customers. After the credit card issuer approves the transaction, the merchant account provider transfers the money to the business’s bank account. This way, the business owner doesn’t have to wait for their customers to receive their money.

Finding a merchant account that is affordable can be difficult, but it can be done. There are many different merchant account providers and a merchant’s needs depend on the type of cards and sales volume. For instance, a flat-rate pricing model may work well for smaller businesses, but for high-volume businesses, a lower-cost option may be much more profitable.

When applying for a merchant account, you must provide all of the necessary information. These include your business’s tax ID number, financial statements, and credit card information. Some providers also require an application fee.

When it comes to software, businesses face a fundamental choice: open or proprietary systems. Each offers distinct advantages and disadvantages, and understanding these differences is crucial for making informed decisions that align with your specific needs and goals.

Proprietary Systems: Control and Support

Proprietary systems, like Microsoft Windows or Adobe Photoshop, are owned and licensed by a specific company.The source code is typically kept secret, giving the vendor tight control over the software’s functionality, distribution, and licensing.

Benefits:

Strong Support: Vendors often provide comprehensive customer support, including documentation, training, and dedicated help desks.

Ease of Use: Proprietary software is often designed with user-friendliness in mind, offering intuitive interfaces and streamlined workflows.

Integration: Proprietary systems may integrate seamlessly with other products from the same vendor, creating a unified ecosystem.

Regular Updates: Vendors typically release regular updates, including new features, bug fixes, and security patches.

Drawbacks:

Cost: Proprietary software often requires licensing fees, which can be a significant expense, especially for smaller businesses.

Vendor Lock-in: Reliance on a single vendor can limit flexibility and create dependency.

Limited Customization: Modifying proprietary software is generally restricted, making it difficult to tailor to specific needs.

Open Systems: Flexibility and Collaboration

Open systems are based on open standards, allowing different software components to interoperate and communicate with each other.Open-source software, like Linux or the Apache web server, takes this a step further by making the source code freely available.

Benefits:

Cost-effectiveness: Open-source software is often free to use, distribute, and modify, reducing upfront costs.

Flexibility and Customization: Users have the freedom to adapt the software to their specific needs and integrate it with other systems.

Community Support: A vibrant community of developers and users often contributes to the development, support, and documentation of open-source projects.

Increased Security: With many eyes reviewing the code, vulnerabilities can be identified and addressed quickly.

Drawbacks:

Support: While community support is often available, dedicated support may be limited or require a paid subscription.

Usability:Some open-source software may have a steeper learning curve or lack the polished user interface of proprietary alternatives.

Compatibility: Ensuring compatibility with existing systems and infrastructure may require additional effort.

Making the Choice: Factors to Consider

The decision between open and proprietary systems depends on several factors:

Budget: Open-source solutions can be more cost-effective, especially for startups and small businesses.

Technical Expertise: Open systems may require more technical expertise for installation, configuration, and maintenance.

Customization Needs: If extensive customization is required, open-source software offers greater flexibility.

Support Requirements: Consider the level of support needed and whether community support or paid support options are available.

By carefully evaluating these factors, businesses can make informed decisions about the software that best aligns with their unique requirements and long-term goals.

To Set up your payment processing merchant account call 888-996-2273 now or go to NationalTransaction.Com

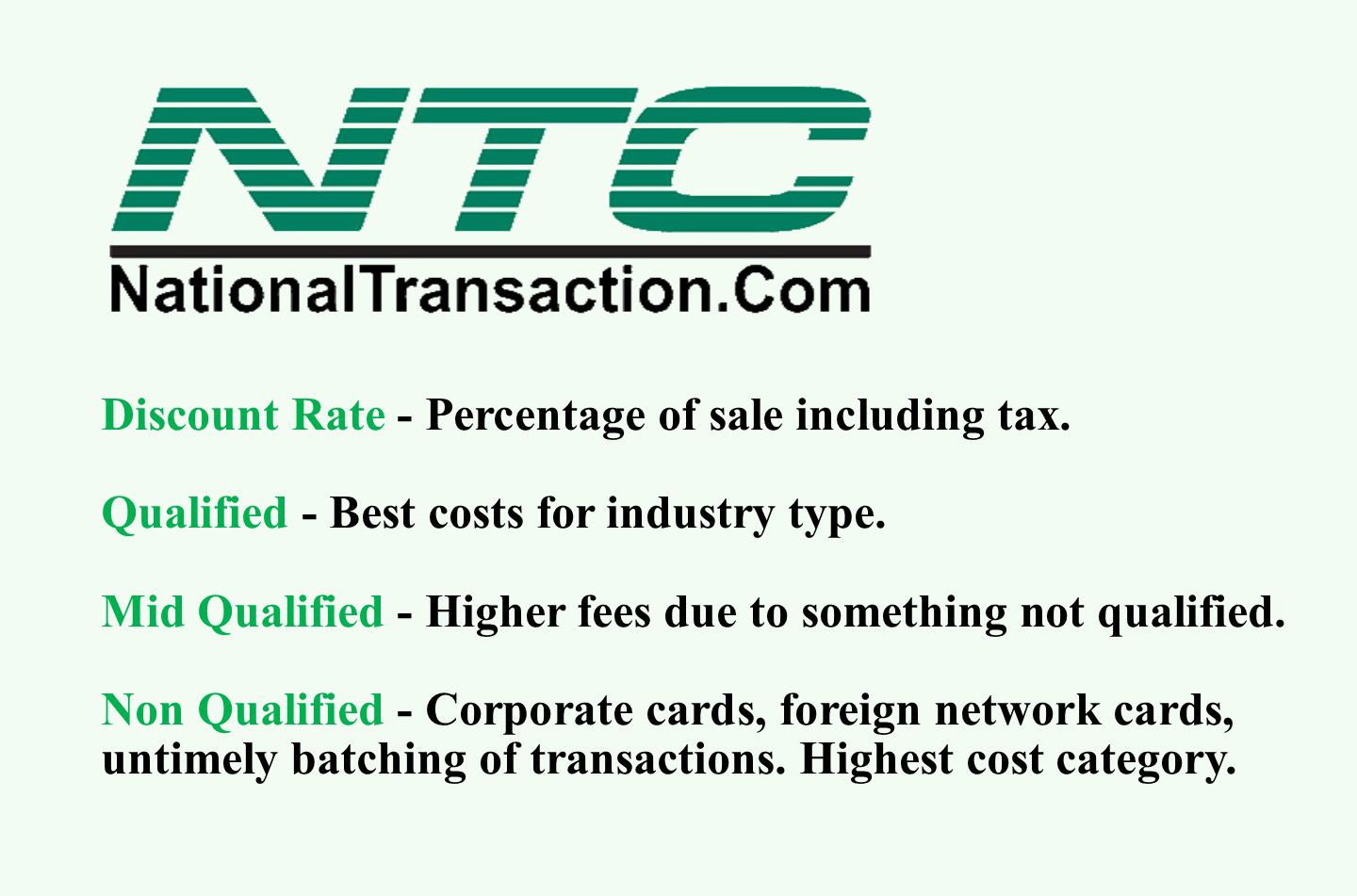

Credit card transaction types are categorized based on the level of risk and processing cost associated with them. Here’s a breakdown of the common types:

1. Qualified

Definition: These are considered the “safest” and least expensive transactions for processors to handle.They typically involve traditional credit or debit cards processed in person with a physical card swipe or chip insertion.

Characteristics:

Card is present during the transaction

Cardholder’s signature is captured (if required)

AVS (Address Verification Service) matches the billing address on file

CVV (Card Verification Value) is provided and matches

Transaction meets all security protocols and risk assessment criteria set by the card issuer and processor.

Examples:Swiping a standard Visa or Mastercard credit card at a retail store.

2. Mid-Qualified

Definition: These transactions fall in between qualified and non-qualified in terms of risk and processing cost. They often involve card-not-present transactions or cards with higher reward structures.

Characteristics:

Manually keyed-in transactions (online, over the phone, or mail order)

Rewards cards with higher cashback or points benefits

Business or corporate cards

Transactions where AVS or CVV information is not provided or doesn’t match

Examples: Entering your credit card details online to purchase something, using a rewards card with travel benefits.

3. Non-Qualified

Definition: These transactions are considered the riskiest and most expensive to process.They often involve international cards, manually keyed transactions without proper security measures, or cards with very high reward programs.

Characteristics:

International credit cards

Manually keyed transactions without AVS or CVV verification

High-risk businesses like online gambling or adult entertainment

Keyed transactions for business or corporate cards

Examples: Using a foreign-issued credit card, manually processing a transaction without verifying the cardholder’s address.

Why does this matter?

Processing Fees: Merchants are charged different fees for each transaction type.Qualified transactions have the lowest fees, while non-qualified transactions have the highest.

Tiered Pricing: Many payment processors use tiered pricing models, categorizing transactions into these types and charging accordingly. This can sometimes be confusing or lead to unexpected costs for merchants.

Interchange Fees: The card networks (Visa, Mastercard, etc.) also charge interchange fees for each transaction, which vary based on factors similar to those used for transaction type categorization.

Understanding these transaction types is crucial for merchants to:

Negotiate better processing rates: By understanding the factors that influence transaction categorization, merchants can negotiate better fees with their processors.

Optimize payment processing: Merchants can take steps to minimize the number of mid-qualified and non-qualified transactions, such as encouraging in-person payments or using address verification systems.

Control costs: By being aware of the different transaction types and their associated costs, merchants can better manage their payment processing expenses.

Remember: The specific criteria for each transaction type can vary depending on the payment processor, card network, and individual merchant account. It’s always best to clarify with your payment processor to understand their specific categorization rules and fee structures.

To establish a merchant account for your business call now 888-996-2273 or click here NationalTransaction.Com

To be responsive to the needs of our merchants and to meet that needs NTC offers next day funding. This is a value added service for customers and businesses that need to have their funds available quickly.

With more than 20 years of experience, National Transaction offers a variety of electronic payment services and technology for Retail and Ecommerce industries. From Travel, Medical Industry, Charitable Institution and Franchise.

Our services include:

Loans/Funding Program

Credit and Debit Card Processing

Currency Conversion

Electronic Checks

Electronic Invoicing

Gift and Loyalty Card Programs

Mobile and Online Solutions

Shopping Cart E-commerce Payment Gateway

NTC e-Pay – is an Electronic Invoicing that made simple with NTC e-Pay! Free Setup, nothing to integrate; secure and fast.

Invoice customers Electronically with NTC e-Pay. Our e-Pay Platform can help Merchants bring new customers and encourage repeat business.

Our Virtual Merchant Gateway – accept payments your way! Online, In-Store and On the Go. A payment platform that flexes with your business.

NTC Business Loans – Fast, Affordable, and Simple Application Process.

MediPaid – a medical health insurance claims payment. Delivering paperless, next-day deposits for Health Insurance Payments.

NTC provides services to thousands of customers. NTC maintains a one on one relationships with all its merchants providing them with 24/7 customer service and technical support!

To know more about our product and services give us a call at 888-996-2273

Tokenization is a powerful security feature that allows a merchant to support all of their existing business processes that require card data without the risk of holding card data and without any security implications, because tokens are useless to criminals, they can be saved by the merchant as they do not represent any threat.

The liability and costs associated with PCI compliance is substantially reduced and the risk of storing sensitive data is eliminated.

Tokenization applies to credit card and gift card transactions.

Imagine a world where you could accept credit card payments without actually storing any sensitive cardholder data. No more worrying about data breaches, PCI compliance headaches, or the crippling costs of a security breach. That’s the power of tokenization.

Here’s how it works:

Instead of storing sensitive credit card information on your systems, each card number is replaced with a unique, randomly generated “token.” This token is useless to hackers, but it can be used to process payments securely on the merchant account that created the token.

Think of it like a valet ticket:

You hand over your car (the sensitive data) to the valet (the tokenization provider), who gives you a unique ticket (the token). The valet keeps your car safe, and you can use the ticket to retrieve it when needed.

The benefits are immense:

Ironclad Security: Reduce your PCI DSS scope and minimize the risk of costly data breaches. With tokenization, even if your system is compromised, the actual card data remains safe.

Effortless Compliance: Simplify PCI compliance and avoid hefty fines. Tokenization helps you meet the stringent security requirements for handling sensitive cardholder data.

Recurring Billing Made Easy: Securely store tokens for recurring billing or future transactions. This allows you to charge customers later without having to store their sensitive information.

Improved Customer Trust: Demonstrate your commitment to data security and build customer trust. Knowing their information is protected encourages repeat business and loyalty.

Streamlined Checkout: Offer a frictionless checkout experience with saved payment information. Tokenization enables faster and more convenient payments for your customers.

Tokenization is not just a security measure, it’s a strategic advantage:

Reduce costs: Minimize the expenses associated with data breaches and PCI compliance audits.

Boost efficiency: Streamline your payment processes and reduce administrative overhead.

Enhance your reputation: Position your business as a leader in data security and customer trust.

In conclusion:

Tokenization is a game-changer for businesses that accept credit cards. It offers unparalleled security, simplifies compliance, and unlocks new opportunities for growth. Embrace the future of secure payments with tokenization and watch your business thrive.

For Electronic Payments with Tokenization call now 888-996-2273 or click here NationalTransaction.Com

Visa 3-D Secure (3DS) is a security protocol designed to add an extra layer of protection to online credit card transactions.It aims to reduce fraud by verifying the cardholder’s identity before the transaction is authorized.Visa’s implementation of 3DS is called “Visa Secure.”

Here’s how it works:

Transaction Initiation: When a customer makes an online purchase with their Visa card, the merchant’s website communicates with the Visa network to initiate the 3DS process.

Risk Assessment: The issuer (the cardholder’s bank) performs a risk assessment based on various factors, such as the cardholder’s history, the transaction amount, and the merchant’s risk profile.

Authentication: If deemed necessary, the issuer challenges the cardholder to authenticate their identity. This usually involves a step-up authentication method, such as:

One-time password (OTP): Sent to the cardholder’s registered mobile phone or email.

Biometric authentication: Fingerprint scan or facial recognition.

Knowledge-based authentication: Security questions or personal information.

Verification: Once the cardholder successfully authenticates, the issuer confirms their identity to the merchant.

Transaction Completion: The merchant can then proceed to process the transaction with increased confidence that the cardholder is legitimate.

Integration and Implementation:

Merchants need to integrate 3DS into their online payment systems.This typically involves working with their payment gateway provider or acquiring bank to implement the necessary APIs and protocols.Visa provides detailed documentation and support for merchants to integrate Visa Secure.

Benefits and Features of 3DS:

Reduced Fraud: By verifying the cardholder’s identity, 3DS significantly reduces the risk of unauthorized transactions and chargebacks.

Improved Security: Adds an extra layer of security to online payments, protecting both merchants and customers from fraud.

Shift in Liability: In many cases, if a fraudulent transaction occurs after successful 3DS authentication, the liability shifts from the merchant to the issuer.This can save merchants significant costs associated with chargebacks and fraud disputes.

Increased Customer Confidence: Demonstrates a commitment to security and builds trust with customers, encouraging them to complete their purchases.

Enhanced User Experience: The latest version of 3DS (EMV 3DS 2.0) offers a smoother and more user-friendly authentication experience, minimizing friction during checkout.

Support for Mobile and Digital Wallets: 3DS is compatible with various payment channels, including mobile devices and digital wallets, providing a consistent and secure experience across all platforms.

In conclusion: Visa 3-D Secure is a powerful tool for merchants to enhance the security of their online transactions, reduce fraud, and improve customer confidence.

By implementing Visa Secure, merchants can protect themselves from financial losses and provide a safer and more trustworthy shopping experience for their customers.

For e-Commerce Electronic Payments set up with 3D Secure

In understanding Big Data for Merchants, NTC provided a general overview of how online merchants can use Big Data. Think about this application of big data as adopting a more intelligent use of data.

Keeping customers happy is the key to the travel industry, but customer satisfaction can be hard to gauge in a timely manner. Big data analytics gives these businesses the ability to collect customer data, apply analytics and immediately identify potential problems before it’s too late.

Collecting Big Data is the easy part. Storing, organizing, and analyzing it is much more complex.

One seam of data that several experts identify as a particularly rich, emerging source of information can be as diverse as a CRM and your own website. Mobile communications, including text messages and social media posts such as Facebook and Twitter.

A business could analyze data on visitor browsing patterns, login counts, phone calls, and responses to promotions.

In a shopping cart analysis, in which a merchant can determine which products are frequently bought together and use this information for marketing purposes.

AVirtual Terminal can capture email addresses at the Point-of-Sale (POS) into a database to assist merchants and consumer stay connected.

As more Big Data solutions for small online businesses come to market and more online merchants incorporate Big Data into their business tool set, employing Big Data will become a necessity for all Merchants.

Using data wisely has the potential to boost margins and increase conversions for online merchants.Application of big data is a more intelligent use of data.

You know WHO, WHAT, WHEN, AND WHERE a purchase took place.

Fighting chargebacks is important to a business. Whether you process transactions at a point of sale location or operate an e-Commerce business making sure you have implemented a process to dispute your chargebacks is critical.

Basic concepts that can be used to begin learning how to dispute chargebacks:

Keep accurate records of data that is easily accessible. Keeping track of your sales and products have a much easier time in collecting the information necessary to combat a chargeback.

Act quickly, don’t wait! You only have 10 days to respond to a chargeback or retrieval request. If you do not respond in 10 days you lose to a chargeback, and It gets worse; as you will not be able to re-present your case.

Compile and submit the documents to your processor. Make sure the documents have the original chargeback documents attached as well as the other supporting documents.

Follow up to make sure they have been received. Your processor may have an online system that allows you to submit documents directly into the processor chargeback system and some even allow you to view submitted documents in REAL TIME.

Monitor your chargebacks, this will help you understand what processes work for each specific chargeback type.

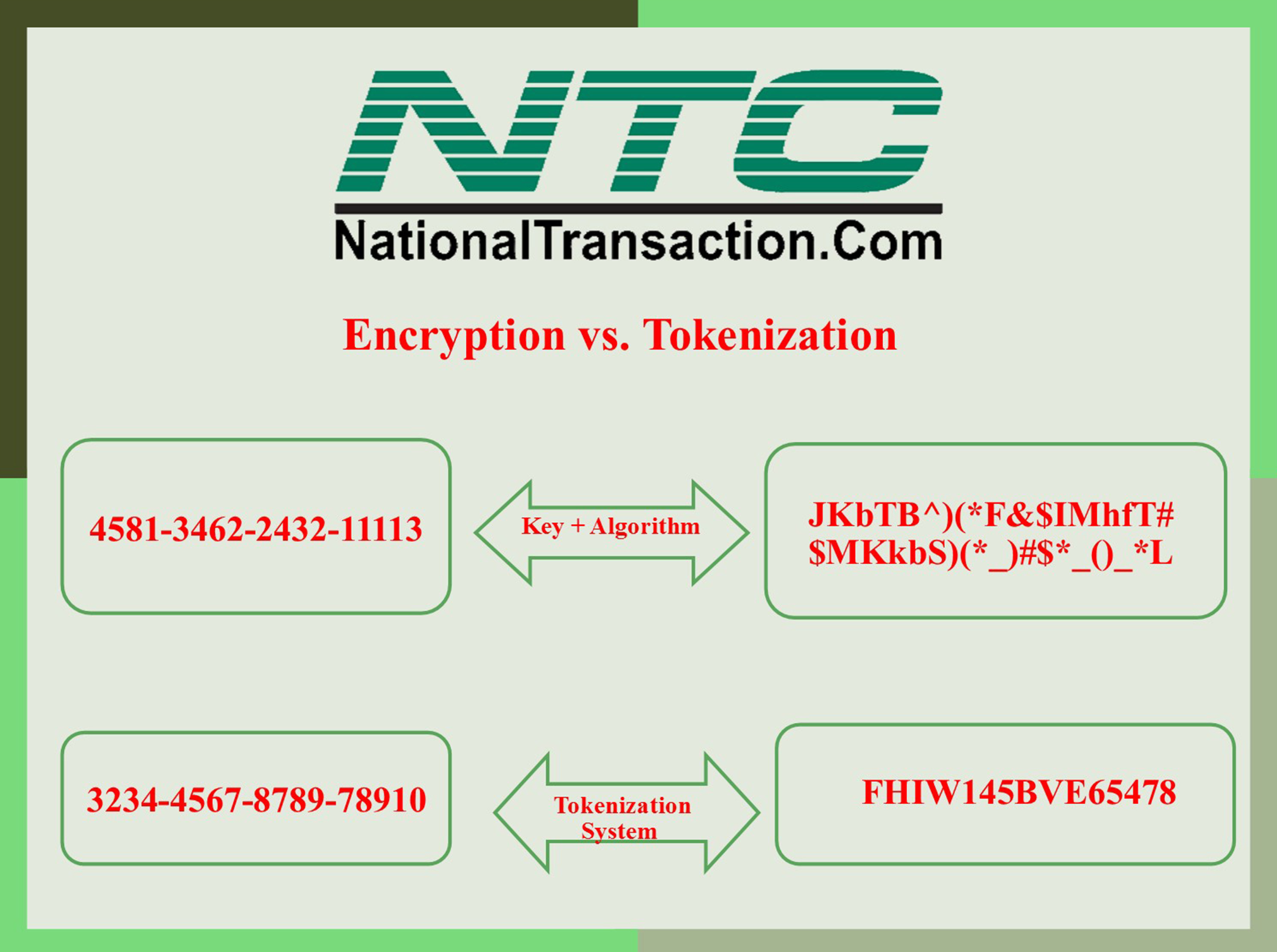

Encryption is reversible. Encrypted data can be returned back to its original, unencrypted form. The encryption strength is based on the algorithm it uses. A more complex algorithm will create stronger encryption to secure the data. Encryption is most often “end-to-end.”

PCI Security Standards Council and other governing compliance entities still view encrypted data as sensitive data.

Tokenization system replaces sensitive data and the token cannot be reversed into true data, it has no value. The real, sensitive information is stored in a secured offsite platform. An entirely different location. That means sensitive customer data does not enter or reside within your environment.

Unlike encryption, tokenization isn’t subject to issues with PCI/DSS compliance or other data security organizations, because tokens do not contain any real data.

If a hacker managed to steal your tokens they cannot be used for a fraudulent transaction.

Using tokens doesn’t change a merchant’s payment processing experience as it protects their valuable credit card information.