Category: Best Practices for Merchants

January 6th, 2016 by Elma Jane

A company is teaming up with MasterCard to help other companies integrate mobile payments into their fitness devices, smart watches, jewelry, or clothing. Anything and everything that can fit an NFC chip inside it.

The program is a small iteration on something MasterCard announced last October, in which MasterCard was setting up essentially the same thing: Tokenized payment systems device makers could embed in virtually anything.

To start, the two companies have partnerships set up with Atlas, Moov and Omate, all of whom make wearable or fitness devices. The idea is that if you’re out for a run, you can just use the fitness band you’ve already got on you to buy something. That makes sense, but it also may mean you’ve got yet another payment system to set up and think about, one that presumably isn’t fully integrated either into your Apple Pay or Android Pay setup.

http://www.theverge.com/2016/1/6/10704812/coin-mastercard-partnership-ces-2016-atlas-wearables-moov-ornate

Posted in Best Practices for Merchants Tagged with: Mobile Payments, nfc, payment system

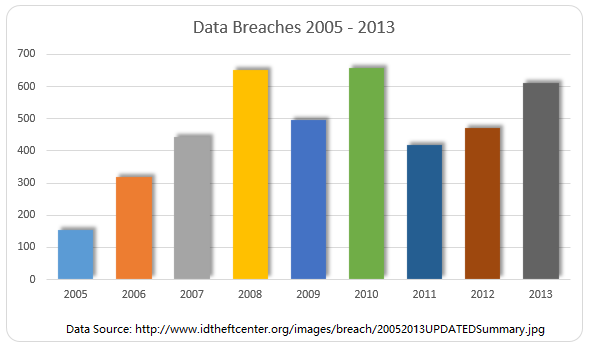

December 28th, 2015 by Elma Jane

Major data breaches were acknowledged by another hotel chain and another brand popular with kids.

Hyatt discovered the intrusion on Nov. 30, which targeted Hyatt-managed properties (not those owned by franchisees), but did not disclose exactly how many properties were affected or how many records may have been exposed. The malware used in the attack targeted payment-card information including cardholder names, PANs, expiration date and CVV/CVC information.

Separately, a security researcher discovered a leaked database from Sanrio, the Japanese company that designs, licenses and produces the popular hello Kitty character. The database reportedly contains account data for 3.3 million users of Sanriotown.com and other Sanrio-owned Websites including hellokitty.com. The company has not yet acknowledged the extent of the breach publicly but said it is investigating.

If so, it is the second network intrusion made public putting the personal information of young people at risk after the Vtech Toy Company Data Breached. Almost 5 million parents and more than 200,000 kids was exposed. The hacked data includes names, email addresses, passwords, and home addresses of 4,833,678 parents who have bought products sold by VTech.

Posted in Best Practices for Merchants Tagged with: card, card information, data, data breaches, payment

December 21st, 2015 by Elma Jane

Chargebacks is a major problem for merchants, rules and regulations surrounding chargebacks can be confusing; becoming educated about these policies, which also includes the release of a new and upcoming regulations will help merchants to empower themselves.

Visa will make major changes to its chargeback rules document in January of 2016.

Traditionally, Visa has had two different excessive-chargeback programs for merchants:

1. For Domestic U.S. transactions – known as the U.S. Merchant Chargeback Monitoring Program.

2. For international transactions – called the Global Merchant Chargeback Monitoring Program.

Each program had a different threshold and monitored transactions in different geographic regions (each with unique risk profiles), it has been possible for a merchant to qualify for one program but not the other.

http://cardnotpresent.com/articles/displaylogin.aspx?id=12785

Posted in Best Practices for Merchants, Visa MasterCard American Express Tagged with: chargebacks, merchants, visa

December 21st, 2015 by Elma Jane

You will think United States or China are the two world’s biggest market when it comes to digital payments and other cashless spending systems. But according to a study, the answer is a less likely source: Sweden is actually on its way to becoming a fully cashless society.

Several factors have come together to give the Swedes an unexpected edge, a combination of IT awareness, and a growing number of useful mobile payments solutions.

The entire country currently only has about 80 billion Swedish crowns in circulation, and as users more often turn to mobile payment systems, the need for cash only declines. About 20 percent of all purchases made in cash in Swedish retail, and that number is falling off almost daily.

Some transactions can only be carried out by digital payments, since the mobile apps are convenient, free to use, and generally regarded as secure, there’s not much impediment for users to turn to such systems.

A truly cashless society is probably a bridge too far; there will always be those who’d rather handle cash. Only time will tell if the market shapes up looking like this, but even with lower actual results than projected, that’s still a lot of people turning to mobile payment and other cashless payment systems. There will still be a huge majority trending toward cashless society.

http://paymentweek.com/2015-12-18-world-leader-in-cashless-trading-an-unexpected-source-9182/

Posted in Best Practices for Merchants Tagged with: digital payments, mobile payment systems, Mobile Payments, mobile payments solutions, payment systems, payments solutions

December 18th, 2015 by Elma Jane

A leading provider of mobile point of sale and mobile payment technology, published today the EMV Migration Tracker.

Many merchants have deployed EMV capable terminals while cardholders have received cards with EMV chips, but not much data has been published about the real world use of EMV chip card technology in the U.S. Most published statistics rely on surveys or forecasts rather than real transactional data.

The EMV Migration Tracker shows new data and insights since the October 1 liability shift, including:

- Over 50% of all cards in use now have EMV chips on them. From October to November, the percent grew 5% as banks and card issuers accelerated their rollout of new chip cards.

- Over 83% of American Express cards have EMV chips, while Discover lags at 40%

- Over 63% of the cards used in Hawaii have EMV chips, but Mississippi sees just 11% penetration of chip cards.

While EMV chip card technology has been implemented in Europe years ago, the rollout of EMV in the U.S is just beginning. The rollout came earlier this year with the October 1 liability shift in card present transaction, meaning that merchants who have not upgraded their POS system can become liable for counterfeit card fraud losses that occur at their stores. This is an early step in an ongoing process that the Payments Security Task Force predicts will lead to 98 percent of U.S. credit and debit cards containing EMV chips by the end of 2017.

http://www.finextra.com/news/announcement.aspx?pressreleaseid=62506

Posted in Best Practices for Merchants Tagged with: American Express, banks, card issuers, card present, card technology, cardholders, chip cards, credit, data, debit, Discover, EMV, EMV chips, merchants, mobile payment, mobile point of sale, payment technology, point of sale, POS, provider

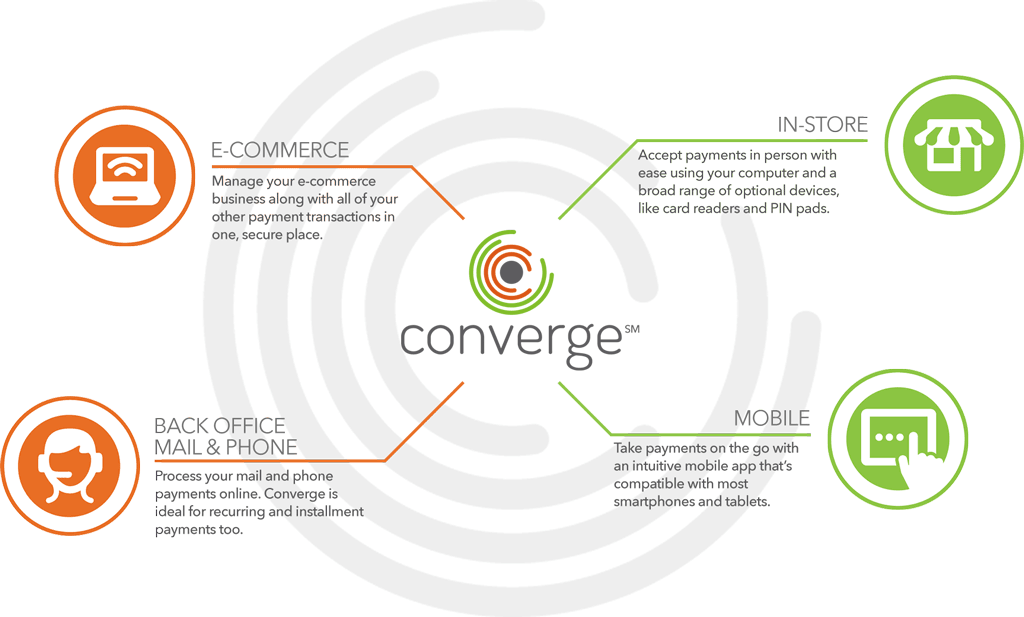

December 17th, 2015 by Elma Jane

We are pleased to announce that the new Converge Mobile App is now available for download in the App Store (Apple iOS devices) and Google Play (Android devices)!

Ingenico iCMP – Item code CICMP for Converge and Converge Mobile

With the launch of the new app, you can now order the Ingenico iCMP PIN Pad for Converge Mobile too!

Please use item code CICMP for those devices that will be used with Converge and Converge Mobile applications.

The Talech iCMP is configured differently and will not work properly without substantial reconfiguration work by our support teams. This creates a negative customer experience and is avoidable when you use the right code – CICMP!

Posted in Best Practices for Merchants Tagged with: Converge, Ingenico iCMP, mobile, Talech iCMP

December 17th, 2015 by Elma Jane

Mobile Payments – It is bound to see more actions with tech giants Apple, Google and Samsung in mobile payment trends. We will also see new technologies like smartwatches, bracelets and rings that will give us the ability to provide payment options.

NFC – Near Field Communication, another familiar face among the payment trends. NFC, however, goes way beyond making payments using smartphones. These speed up POS payment processing quickly and easily without requiring a PIN or signature. While there are other POS payment methods, such as QR codes, NFC will come out on top. Merchants should ensure they have an overview of the current Point-of-Sale options and should, if needed, upgrade to the latest technology.

Security: Tokenization and biometric authentication will have a strong influence on the payment industry.

Tokenization – when applied to data security, is an extremely interesting method of securing credit card data. As the credit card numbers are substituted by tokens that has no value, then no harm can be done if tokens are stolen, which makes tokenization a secure process.

There are several new inventions when it comes to payment processing authentication such as password, PIN, and fingerprint methods. But they are weak so two-factor authentication is increasingly used to improve security.

Biometrics Authentication – like finger print scan, facial recognition, voice recognition, and pulse recognition are set to become increasingly significant. This will increase both security and convenience.

International E-Commerce – It’s important that merchants offer shoppers their preferred local payment method. Merchants who are looking for e-commerce success will need to create an international strategy. Merchants should also consider checking with their payment service providers. Providers know their way around to alternative payment methods.

Cash on the Retreat – Cashless Society? Some countries in Europe are certainly cutting down on the usage of cash. In Sweden, it is now almost impossible to use cash to pay for bus tickets. Acceptable payment methods include customer cards, credit cards, and payments via smartphone apps. Traditional cash-based bakeries no longer exist and instead, now display signs requesting that customers use cashless payment methods for even the smallest amounts. The situation in Denmark is similar; the government is currently debating whether or not to release smaller retailers from the obligation of having to accept cash as a payment method. Cash is on the retreat, and alternative payment methods are advancing. However, cash is still on the list.

Real-Time Payments (Instant Payments) – The European Central Bank (ECB) will bring instant payments strongly in the near future. Instant or real-time payments are a trend which will be with us for a long time to come.

Regulatory Changes – The first Payment Services Directive (PSD) from 2007 is still currently implemented domestically. After a tough two-year negotiation period, the EU has now, finally, agreed on a second payment services directive (PSD2). The European Banking Authority (EBA) is set to develop more detailed guidelines and regulatory standards for various industries. Payment industries should begin preparing themselves now for implementation, doing this will allow them to be ready for the appropriate steps necessary in 2016/2017.

Posted in Best Practices for Merchants, e-commerce & m-commerce, Near Field Communication, Point of Sale, Travel Agency Agents Tagged with: Apple, biometric, credit card, data security, e-commerce, google, merchants, Mobile Payments, Near Field Communication, nfc, payment industry, payment methods, payment options, payment processing, payment service providers, payment services, payment trends, payments, PIN, point of sale, POS, qr codes, real-time payments, Samsung, tokenization

December 16th, 2015 by Elma Jane

Google’s contactless payment solution, Android Pay, will now be available through the mobile checkouts of several Android apps in the U.S.

With this addition, it avoids having to pull out your card everytime you make a purchase, meaning card data never makes it to the merchants. A good news for anyone who is concerned about privacy.

Android Pay is compatible with all Near Field Communication (NFC) or Host Card Emulation (HCE) enabled devices using any OS released since KitKat.

With Coca-Cola signing up as the first merchant in the Google program, a new loyalty program was recently released for the mobile wallet, by tapping your phone on an NFC-enabled Coke vending machine, you’ll get a Coke and get points added into your Android Pay Account for future purchases.

http://www.pymnts.com/news/payment-methods/2015/android-pay-now-in-app-payment-option/

Posted in Best Practices for Merchants, Credit Card Security, Mobile Payments, Smartphone Tagged with: Android Pay, card, card data, contactless payment, HCE, host card emulation, loyalty program, merchants, mobile wallet, Near Field Communication, nfc, payment

December 15th, 2015 by Elma Jane

Visa Inc. has launched the Visa Token Service in Asia Pacific, in association with United Overseas Bank (UOB). Store tokens on mobile devices, cloud-based mobile applications, and e-commerce merchants carry less risk of security hack. This security technology will replace sensitive account information to make payments without exposing bank details.

Tokenized cards are linked to customer’s wallet application or mobile and validated by VisaNet. Biometric authentication and device identification features are available through this service. Visa debit or credit cardholders with NFC-enabled Android smarthphones cardholders will be able to make contacless payments.

Posted in Best Practices for Merchants, e-commerce & m-commerce Tagged with: bank, biometric, cardholders, cards, contacless payments, credit, debit, e-commerce, e-commerce merchants, merchants, nfc, payments, token, Tokenized cards, visa

December 14th, 2015 by Elma Jane

Reality of data theft means that a breach can sometimes have two or three aftershock effects years down the line.

Eighty five percent of American consumers admitted that if significant personal consequences present themselves after their information is compromised as part of a breach, they would have no problem seeking a new place to spend their money.

In particular, 67 percent said that they would cut ties with the victimized brand if money was actually removed from their checking accounts, 62 percent said so if their credit cards were charged for fraudulent purchases, 57 percent said the same if their personal information was released and 54 percent would look elsewhere if their credit scores were affected.

It’s been two years since major retail attacks made data breach a household word, vice president of enterprise data security firm said.

As it becomes easier for customers to switch their preferred brands, data breaches events can be too devastating for some merchants.

http://www.pymnts.com/news/2015/been-breached-say-bye-bye-to-customer-loyalty/

Posted in Best Practices for Merchants Tagged with: Breach, credit, data breach, data security, merchants