Category: Best Practices for Merchants

September 19th, 2014 by Elma Jane

CREDIT CARD NUMBER’S ANATOMY

The numbers on front of a credit card aren’t just random. They give away specific information about the card and where it comes from.

The first 6 digits of the credit card number is the Bank Identification number (BIN). This will tell the name of the credit card issuer.

Example: Travel or entertainment cards, such as American Express cards, begin with a 3 . All Visa credit cards start with a 4, MasterCard with a 5, and 6 is dedicated to Discover.

The first six digits of the card, including the Bank Identification number, represent the issuer identification number. This identifies the bank that issued the card.

Of course, there’s the personal account number. This is made up of the seventh digit on, everything except the last number on the card.

The final digit on the credit card is known as the check digit or checksum. This number is set by something called the Luhn formula, patented by an IBM scientist in 1960. It’s a formula that uses the numerals in your card’s account number to verify that it’s valid. Various combinations of the card’s digits must ultimately add up to a number divisible by 10.

The formula is mostly used to protect against input errors. Let’s say you enter in the wrong numbers on an online shopping site. The formula will compute that the digits don’t add up right, telling you you’ve entered an invalid card number. That last digit of your credit card makes sure the formula works like it’s supposed to.

Now you know that there’s a lot of information on that little card in the wallet.

Posted in Best Practices for Merchants, EMV EuroPay MasterCard Visa, Visa MasterCard American Express Tagged with: (BIN), account number, American Express cards, Bank Identification number, card, card issuer, card number, check digit or checksum, credit, credit card issuer, credit card number, credit-card, Discover, entertainment cards, issuer identification number, MasterCard, online shopping site, personal account number, Visa credit cards

September 19th, 2014 by Elma Jane

MasterCard is claiming a 98% success rate for pilot trials of a biometric verification system combining both voice and facial recognition.

It recently held a closed pilot to understand the consumer experience around voice and facial recognition.

A beta mobile app was tested in an e-commerce environment on over 14,000 transactions. The test group, used both Android and iOS operating systems. The results, yielding a successful verification rate of 98%, mixing a combination of voice and facial recognition. The process usually took less than 10 seconds.

With the first wave of apps utilising Apple’s TouchID fingerprint recognition system coming to market – both US neo-bank Simple and PFM outfit Mint have shipped their first iOS upgrades to incorporate the technology. Biometric verification is beginning to gain currency among businesses and consumers as a useful tool in the fight against fraud.

The launch of Apple Pay will start to bring true scale to the next generation of payments authentication. The challenge is to take lessons from the different applications of biometrics already in place and elevate them into the next generation of authentication, not just for one platform, but for the mass market globally.

MasterCard already has first hand experience of a mass-market implementation of biometric card technology with the recent launch of the Nigerian eIDcard, which combines payment card functionality with a mix of fingerprint, facial and iris recognition.

Posted in Best Practices for Merchants, EMV EuroPay MasterCard Visa, Visa MasterCard American Express Tagged with: Android, Android and iOS operating systems, Apple Pay, Apple's TouchID, beta mobile app, biometric card, biometric card technology, biometric verification, biometric verification system, card, card technology, consumer, currency, e-commerce, facial recognition, fingerprint recognition, fingerprint recognition system, fraud, iOS, iOS operating systems, iris recognition, mass market, MasterCard, mobile app, payments authentication, platform, rate, transactions, verification rate, verification system, voice and facial recognition

September 18th, 2014 by Elma Jane

Americans love gift cards, but many of those pieces of plastic go partially or entirely unused. Some are lost or forgotten. Others simply are ignored once the balance drops to a few dollars or less.

A gift card’s unused value…known in industry parlance as spillage or breakage…long has meant big profits for the gift card industry .

But the Credit Card Accountability, Responsibility and Disclosure Act of 2009, better known simply as the Credit CARD Act, tightened rules on retailers, making it more difficult for stores to cancel unused cards or charge inactivity fees. That prevents retailers from quickly cashing in on breakage.

In addition, savvy consumers are catching on and appear to be finding ways to avoid losing breakage while getting the most out of their gift cards.

According to the most recent figures, about 1 percent of the total value of gift cards was predicted to go unused in 2013. That’s down from a record high of 10 percent in 2007. Some of the reduction in breakage is a result of growing cardholder realization that even though there’s only $2.12 on gift card, they got to find a way to use it.

However, even with the decline in breakage, around $1 billion worth of gift cards will be lost to fees and expiration dates or misplaced, shoved in a drawer or otherwise neglected this year. That’s a huge amount of money that consumers will not be able to use toward a new shirt, stuffed animal or bicycle.

Retailers love when people use gift cards because studies show that most customers spend more in the store than the card is worth. Breakage makes gift cards even more profitable: An estimated $127 billion in gift cards will be sold in 2014, even a small percentage of unused cards boost a company’s bottom line.

Those profits make it feasible for retailers to make some consumer-friendly moves, such as selling gift cards at a discount. However, most of the money goes toward other endeavors.

Wal-Mart may have a billion dollars (in unused gift cards) sitting there. Wal-Mart could go out and build 30 new superstores without borrowing a penny. They know those gift cards will come in eventually, but for now, they have the use of that money.

Ways to make sure you’re not ‘breakage’

The longer you let a card sit untapped, the less likely you are to use it. Here are eight ways to make sure your gift cards are not lost to breakage:

Give again. Instead of letting that last two bucks on a card go to waste, use it to make a donation. Stockpile cards and combine them into higher-value gift cards that are donated to the needy.

A Gift Card Giver founder, got the idea when he asked a group of acquaintances how many had unused gift cards sitting in their wallets. They literally started pulling out gift cards from their wallets, everyone had one.

The Gift Card Giver founder offered to redistribute the unused cards to the needy and a new nonprofit was born.

Give low-end cards as gifts. To make sure your gift card doesn’t languish in someone else’s wallet, consider purchasing cards at Walgreens and Wendy’s instead of Nordstrom and Saks. Practical gift cards, such as those for fast-food chains and discount retailers are used faster than cards to fine dining establishments and pricey department stores.

Corral your cards. Make sure you can quickly locate your cards by storing them all in the same place.

If you have too many cards to tuck into your wallet, stowing them in a durable plastic envelope. Or upgrade to a Card Cubby (about $24), which includes alphabetized tabs and is tiny enough to keep in a purse.

Plan your shopping ahead of time. Set up your e-mail program to send you a monthly reminder to use your gift cards. Think in terms of the week or month ahead, when will you be near the store? What items do you need there? Is there a gift you need for someone else? You are more likely to use the card if you know what you want ahead of time and can get in and out quickly.

Rethink general-purpose gift cards. Gift cards from credit card companies can be used anywhere you can use a credit card. But these cards also come with drawbacks.

Use-anywhere cards, known as open-loop cards are more likely to come with startup fees and monthly inactivity fees that chip away at your balance. Many of these gift cards also include a valid through or good through date stamped on the front. Your card’s underlying value will not expire after that date, but you will have to call customer service for a replacement card, and that raises the risk that you will simply toss the card and your remaining balance.

Read the fine print. The CARD Act prohibits gift card inactivity fees for the first year, and requires that gift cards cannot expire within five years of when activated. State lawsmay extend additional gift card protections. That gives you a big, but not permanent cushion of time to use the cards.

Trade or sell your cards. If you get a card you know you will not use, a Hot Topic gift card, for instance, when you are more of an L.L.Bean type, use one of the many card-swapping and card-selling sites to get what you really want.

That is because with a Wendy’s and a Walgreens on practically every corner, such lower-end cards simply are more convenient to use. They also offer more value for your card. If you give a Wal-Mart gift card to your mailman, there are plenty of things to use it on.

Posted in Best Practices for Merchants, Gift & Loyalty Card Processing Tagged with: card-selling, card-swapping, cardholder, cards, consumers, Credit CARD Act, credit card companies, credit-card, customer service, customers, drawbacks, e-mail program, fees, gift card industry, Gift Cards, inactivity fees, lower-end cards, open-loop cards, retailers, startup fees, Wal-Mart gift card

September 18th, 2014 by Elma Jane

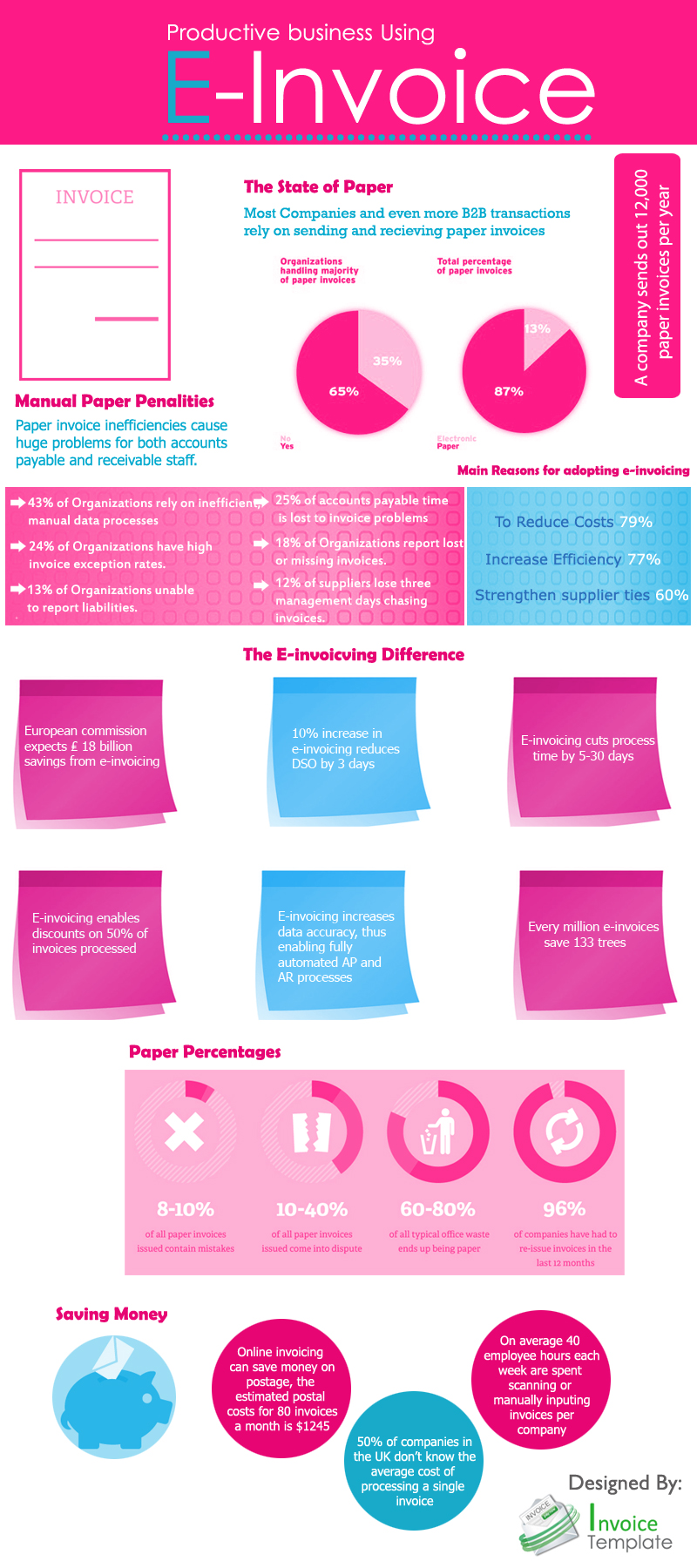

Electronic invoicing is the exchange of the invoice document between a supplier and a buyer in an integrated electronic format. Traditionally, invoicing, like any heavily paper-based process, is manually intensive and is prone to human error resulting in increased costs and processing lifecycles for companies.

The issue of compliance seems to have separated E-Invoicing from B2B. Surprisingly many Finance leaders are unaware that their company is already sending/receiving EDI electronic invoices.

E-Invoicing is a common B2B practice and National Transaction is ready to launch its E-Invoicing system.

True definition of an electronic invoice is that it should contain data from the supplier in a format that can be entered integrated into the buyer’s Account Payable (AP) system without requiring any data input from the buyer’s AP administrator.

There are number of formats to be employed, it is useful to Apply below guidelines:

An E-Invoice:

1) Structured invoice data issued in Electronic Data Interchange (EDI) or XML formats.

2) Structured invoice data issued using standard Internet-based web forms.

Not a true E-Invoice:

1) Paper invoices sent via fax machines.

2) Scanned paper invoices.

3) Unstructured invoice data issued in PDF or Word formats.

Although significant cost and time savings can be achieved by removing paper and manual processing from your invoicing, the real benefits of E-Invoicing come with the level of security that comes with E-invoicing. Integration between your trading partners and your invoicing software and other business systems are optional. National Transaction can offer a customized Electronic Invoice Structure .

Posted in Best Practices for Merchants Tagged with: (AP), Account Payable, AP administrator, b2b, buyer, compliance, data, E-Invoice, E-Invoicing, E-Invoicing system, EDI, EDI electronic invoices, electronic data interchange, electronic format, electronic invoices, Electronic invoicing, Finance leaders, Internet-based web, invoice document, invoicing, National Transaction, Paper invoices, Security, supplier, web

September 17th, 2014 by Elma Jane

Commuters using the London tube network can now tap their contactless bank cards on the ticket barriers to pay for their journeys, further displacing cash on the capital’s transit system.

Fares are cheaper than cash, with users being charged adult pay as you go fares and benefiting from daily and Monday to Sunday fare capping. Customers without bank cards will continue to benefit from cheaper fares through Transport for London’s Oyster card.

This is not the end of Oyster and it’s not the end of cash, but it is a significant dent in the market for cash.

The move follows the abolition of cash on London’s buses and covers all tube, overground, DLR, tram and National Rail services that accept Oyster.

The shift to contactless has future-proofed the capital’s transit system for up-and-coming innovations in payments. You can already use your mobile phones to make your payments and tap and go through the tube turnstiles, and in the future it will open up many other connected devices as well, whether that’s smart wristbands or smart watches.

An incredible response to the launch of contactless payments on London Buses with nearly 19 million Visa contactless journeys made since it launched in 2012. Today’s launch will be another major boost to contactless usage leading to the three-fold increase expected in the next year. To coincide with the rollout, Londoners are invited to sign up for 10,000 free bPay contactless payments bands. Its wearable device will let commuters pay for their journeys with a wave of their wrists and help avoid card clash.

Posted in Best Practices for Merchants Tagged with: bank, card clash, cards, contactless bank cards, contactless payments, customers, devices, mobile, mobile phones, network, payments, phones, smart watches, smart wristbands, Visa contactless journeys, wearable device

September 17th, 2014 by Elma Jane

Host Card Emulation (HCE) offers virtual payment card issuers the promise of removing dependencies on secure element issuers such as mobile network operators (MNOs). HCE allows issuers to run the payment application in the operating system (OS) environment of the smart phone, so the issuing bank does not depend on a secure element issuer. This means lower barriers to entry and potentially a boost to the NFC ecosystem in general. The issuer will have to deal with the absence of a hardware secure element, since the OS environment itself cannot offer equivalent security. The issuer must mitigate risk using software based techniques, to reduce the risk of an attack. Considering that the risk is based on probability of an attack times the impact of an attack, mitigation measures will generally be geared towards minimizing either one of those.

To reduce the probability of an attack, various software based methods are available. The most obvious one in this category is to move part of the hardware secure element’s functionality from the device to the cloud (thus creating a cloud based secure element). This effectively means that valuable assets are not stored in the easily accessible device, but in the cloud. Secondly, user and hardware verification methods can be implemented. The mobile application itself can be secured with software based technologies.

Should an attack occur, several approaches exist for mitigating the Impact of such an attack. On an application level, it is straightforward to impose transaction constraints (allowing low value and/or a limited number of transactions per timeframe, geographical limitations). But the most characteristic risk mitigation method associated with HCE is to devaluate the assets that are contained by the mobile app, that is to tokenize such assets. Tokenization is based on replacing valuable assets with something that has no value to an attacker, and for which the relation to the valuable asset is established only in the cloud. Since the token itself has no value to the attacker it may be stored in the mobile app. The principle of tokenization is leveraged in the cloud based payments specifications which are (or will soon be) issued by the different card schemes such as Visa and MasterCard.

HCE gives the issuer complete autonomy in defining and implementing the payment application and required risk mitigations (of course within the boundaries set by the schemes). However, the hardware based security approach allowed for a strict separation between the issuance of the mobile payment application on one hand and the transactions performed with that application on the other hand. For the technology and operations related to the issuance, a bank had the option of outsourcing it to a third party (a Trusted Service Manager). From the payment transaction processing perspective, there would be negligible impact and it would practically be business as usual for the bank.

This is quite different for HCE-based approaches. As a consequence of tokenization, the issuance and transaction domains become entangled. The platform involved in generating the tokens, which constitute payment credentials and are therefore related to the issuance domain, is also involved in the transaction authorization.

HCE is offering autonomy to the banks because it brings independence of secure element issuers. But this comes at a cost, namely the full insourcing of all related technologies and systems. Outsourcing becomes less of an option, largely due to the entanglement of the issuance and transaction validation processes, as a result of tokenization.

Posted in Best Practices for Merchants, Credit Card Security, EMV EuroPay MasterCard Visa, Near Field Communication, Visa MasterCard American Express Tagged with: (MNOs), (OS), assets, bank, card, card issuers, cloud, cloud based payments, cloud based secure element, cloud-based, hardware secure element, Host Card Emulation (HCE), issuing bank, MasterCard, mobile, mobile app, mobile application, mobile network operators, mobile payment, mobile payment application, nfc, operating system, payment application, payment transaction, payments, platform, risk, secure element, smart phone, software, software based technologies, token, tokenization, transaction, virtual payment, visa

September 16th, 2014 by Elma Jane

Card-not-present merchants are battling increasingly frequent friendly fraud. That type of fraud..The I don’t recognize or I didn’t do it dispute. This occurs when a cardholder makes a purchase, receives the goods or services and initiates a chargeback on the order claiming he or she did not authorize the transaction.

This problem can potentially cripple merchants because of the legitimate nature of the transactions, making it difficult to prove the cardholder is being dishonest. The issuer typically sides with the cardholder, leaving merchants with the cost of goods or services rendered as well as chargeback fees and the time and resources wasted on fighting the chargeback.

Visa recently changed the rules and expanded the scope of what is considered compelling evidence for disputing and representing chargeback for this reason code. The changes included allowing additional types of evidence, added chargeback reason codes and a requirement that issuers attempt to contact the cardholder when a merchant provides compelling evidence.

The changes give acquirers and merchants additional opportunities to resolve disputes. They also mean that cardholders have a better chance to resolve a dispute with the information provided by the merchant. Finally, they provide issuers with clarity on when a dispute should go to pre-arbitration as opposed to arbitration.

Visa has also made other changes to ease the burden on merchants, including allowing merchants to provide compelling evidence to support the position that the charge was not fraudulent, and requiring issuers to a pre-arbitration notice before proceeding to arbitration, which reduces the risk to the merchant when representing fraud reason codes.

The new “Compelling Evidence” rule change does not remedy chargebacks but brings important changes for both issuers and merchants. Merchants can provide information in an attempt to prove the cardholder received goods or services, or participated in or benefited from the transaction. Issuers must initiate pre-arbitration before filing for arbitration. That gives merchants an opportunity to accept liability before incurring arbitration costs, and Visa will be using information from compelling evidence disputes to revise policies and improve the chargeback process

Visa made those changes to reduce the required documentation and streamline the dispute resolution process. While the changes benefit merchants, acquirers and issuers, merchants in particular will benefit with the retrieval request elimination, a simplified dispute resolution process, and reduced time, resources and costs related to the back-office and fraud management. The flexibility in the new rules and the elimination of chargebacks from cards that were electronically read and followed correct acceptance procedures will simplify the process and reduce costs.

Sometimes, an efficient process for total chargeback management requires expertise or in-depth intelligence that may not be available in-house. The rules surrounding chargeback dispute resolution are numerous and ever-changing, and many merchants simply do not have the staffing to keep up in a cost-effective and efficient way. Chargebacks are a way of life for CNP merchants; however, by working with a respected third-party vendor, they can maximize their options without breaking the bank.

Reason Code 83 (Fraud Card-Not-Present) occurs when an issuer receives a complaint from the cardholder related to a CNP transaction. The cardholder claims he or she did not authorize the transaction or that the order was charged to a fictitious account number without approval.

The newest changes to Reason Code 83, a chargeback management protocol, offer merchants a streamlined approach to fighting chargebacks and will ultimately reduce back-office handling and fraud management costs. Independent sales organizations and sales agents who understand chargeback reason codes and their effect on chargeback rates can teach merchants how to prevent chargebacks before they become an issue and successfully represent those that they can’t prevent.

Posted in Best Practices for Merchants, EMV EuroPay MasterCard Visa, Visa MasterCard American Express Tagged with: account, account number, acquirers, agents, Back Office, card, card holder, card-not-present, Card-not-present merchants, cardholder, cards, chargeback, chargeback fees, chargeback rates, cnp, CNP merchants, CNP transaction, fees, fraud, fraud management, Independent sales, independent sales organizations, issuer, management protocol, Merchant's, organizations, protocol, purchase, Rates, resolution, resolution process, resources, risk, sales agents, services, transaction, visa

September 16th, 2014 by Elma Jane

When plastic cards become digital tokens, they become virtual. So how do you say that the Card is Present or Not Present. The legendary regulatory difference that the cards industry has relied on to differentiate between interchange fees for Card Present and Card Not Present transactions.

Apple secured Card Present preferential rates for transactions acquired by iTunes on the basis that the card’s legitimacy is verified with the issuer at the time of registration and the token minimizes probability of fraud. If an API call to the issuing bank is sufficient to say that the Card is Present, who is to say that the same logic can’t apply to online merchants who also verify the authenticity of Cards on File when they tokenize them? How can one arbitrarily say that the transaction processed with token from an online merchant is Card Not Present, but the one processed with Apple Pay is Card Present even though both might have made the same API call to the bank to verify the card’s validity?

In the Apple case, a physical picture of the card is taken and used to verify that the person registering the card has it. It is not that hard for an online merchant to verify that the Card on File converted as a token does belong to the person performing an online transaction.

As we move towards chip and pin the card present merchants will spend substantial money upgrading their hardware and POS systems. That expense will be offset by that savings in losses due to fraud. MOTO and e-commerce transactions ( card NOT present ) will always have a higher cost because the nature of processing is NON face to face transactions. Of course the fraud and losses are higher when the card is manually entered or given to someone over the phone……Face to face will always have the lowest cost per transaction because it is usually the final step in the sale. Restaurants are low risk because you had the transaction AFTER you eat. If there is a dispute it happens before the merchant even sees the credit card.

In the long run, as cards become digital and virtual through tokens, we are all going to wonder if card is present or not present. May be some will say. Card is a ghost.

Posted in Best Practices for Merchants, Credit card Processing, EMV EuroPay MasterCard Visa, Visa MasterCard American Express Tagged with: (POS) systems, API call, Apple secured Card Present, bank, Card Not Present transactions, card present, card present merchants, cards, cards industry, chip, credit-card, digital and virtual, digital tokens, e-commerce transactions, fees, fraud, hardware, industry, interchange, interchange fees, issuer, issuing bank, low risk, Merchant's, moto, NON face to face transactions, online, online merchants, online transaction, PIN, Processing, Rates, token, transactions

September 15th, 2014 by Elma Jane

Visa has taken advantage of the hoopla surrounding Apple’s application of digital account tokens to replace card numbers for online and mobile purchasing by initiating the roll out of its Token Service to US clients.

Visa Tokens will be made available to issuing financial institutions globally, starting with US banks next month, and followed by a phased roll-out overseas beginning in 2015. The technology has been designed to support payments with mobile devices using all major mobile platforms.

More than 750 staff from across the Visa organisation globally were involved in the effort, working closely with initial launch partners – financial institutions, merchants and processors to ensure the ecosystem was ready. Today, Visa is making these services available and believe it will help transform connected devices and wearables into secure payment vehicles.

Visa Token Service replaces sensitive payment account information found on plastic cards with a digital account number or token. Because tokens do not carry a consumer’s payment account details, such as the 16-digit account number, they can be safely stored by online merchants or on mobile devices to for e-commerce and mobile payments.

The release of the service has been given added urgency by a spate of successful hacks on merchant card data stores, such as the recent plundering of card account data at Home Depot and Target.

MasterCard has its own equivalent Digital Enablement Service, which will be released outside of the US in 2015.

Posted in Best Practices for Merchants, Credit Card Security, e-commerce & m-commerce, Mobile Payments, Visa MasterCard American Express Tagged with: account details, card, card account data, card data, data, digital account, digital account number, e-commerce, financial institutions, MasterCard, merchant card data, Merchant's, mobile, Mobile Devices, Mobile Payments, mobile platforms, online merchants, payments, processors, Token Service, tokens, visa, Visa organisation, Visa Token Service, wearables

September 12th, 2014 by Elma Jane

Over the last couple of years, Big Data has become a huge buzzword in the business world. Whether this data comes from social networks, purchase histories, Web browsing patterns or surveys.

The vast amount of consumer information that brands can gather and analyze has allowed them to improve and personalize their customers’ experiences. But for all the attention Big Data has received, many companies tend to forget about one application of it…Employee Engagement.

When done in the right way, tracking, analyzing and sharing employee performance metrics can be very beneficial for both you and your staff. One of the things that is very powerful is being able to analyze real-time information, boil it down into performance data and empower employees with reports from that data. If you can provide employees with data to do their job better in a succinct, actionable way, it’s very motivating.

The more Big Data can be incorporated into an intimate individual experience, the better. This demonstrates to the employee that the experience is not just off the shelf and that it is relevant to the person. This personal relevance is shown to deliver higher engagement.

Applying Big Data analytics to employees’ performance helps identify and acknowledge not only the top performers, but the struggling or unhappy workers as well.

If you want to introduce analytics technology to your employee engagement strategies, below are a few tips to help you.

Find a program that integrates with your current systems. For any new software that you implement within your company, it’s important to make the transition as seamless and simple for your employees as possible.

The software has to work where the employees work already. You can’t make them switch tasks and go to another platform to aggregate the data stream. The software should genuinely assist the end user. Your choice of software should be a grassroots decision, and you should have buy-in from your employees before you ask them to use the new system.

Consider how employees will view themselves and others. Once you introduce performance and engagement analytics into your company, you’ll have to consider how that program fits into employee relationships and workplace culture as a whole.

A company needs to take into consideration the actions of the employee’s co-workers and how to make these data points of interest to the employee. This helps to foster a respected and trusting engagement experience and data needs to be used to build trust. No matter what solution you choose, an analytics program moves you away from the traditional manual reporting process of performance measurement; helping make your staff more efficient, motivated and engaged.

Business software is in the beginning stages of being useful for performance measurement. Businesses have not pushed for innovation as hard as consumers have, but now that’s starting to change. Think about business processes in a different way and gather data in a way that matters.

Select and focus on the most important metrics.Analytics programs can pull and process data for a large number of metrics. Even when applying Big Data to customer service, many businesses struggle to keep up with the volume of information pouring in. Narrowing down your focus to only the most important key performance indicators (KPIs). Don’t introduce too many metrics, it becomes too difficult and confusing. If you can boil it down to some very simple statistics, like a score that incorporates the elements you want, everyone can focus on consolidated KPIs.

Posted in Best Practices for Merchants Tagged with: big data, Business software, consumer, customer, customer service, data, key performance indicators, program, service, social networks, software, web, Web browsing patterns