Category: Credit Card Reader Terminal

August 2nd, 2016 by Elma Jane

Credit card machine or point of sale terminals are used for processing debit and credit card transactions and are often integrated into a Point of Sale System. Let’s take a look at the POS terminal evolution.

Manual Imprinters – although the process was time consuming and did not offer the speed or instant transfer capabilities, manual imprinters have been around since the start of a wide acceptance of credit cards. Manual imprinters are still widely used and are considered a great backup processing method.

Electronic Authorizations – Merchants had the choice of calling in for an authorization or imprinting their transactions. The first electronic credit card authorizations were done over the phone, but many businesses opted voice authorization only on larger transactions because of the long waiting time for authorizing a transaction over the phone,

Point of Sale Terminals: Point of sale terminals emerged in 1979, which was a turning point in the credit card processing industry. Visa introduced a bulky electronic data capturing terminal. This was the first of credit card machine or terminal as we know them today, it has greatly reduced the time required to process a credit card. MasterCharge became MasterCard in the same year and credit cards were replaced to include a magnetic information stripe which now has become EMV/chip and PIN.

The Future: There’s a lot of room for advancement when it comes to Credit card processing technology. Increasing processing speed, reliability and security are driving forces behind processing technology advancement. Today’s credit card terminals are faster and more reliable with convenient new capabilities including contactless and Mobile NFC acceptance. The processing industry will definitely be adapting new technologies in the near future and has a lot to look forward to.

Posted in Best Practices for Merchants, Credit Card Reader Terminal, EMV EuroPay MasterCard Visa, Near Field Communication Tagged with: credit card, credit card machine, debit, electronic credit card, Electronic Data, EMV/chip, merchants, mobile, nfc, PIN, point of sale, POS, processing industry, terminals, transactions, visa

July 26th, 2016 by Elma Jane

Mobile payment space is growing yet, many small businesses and retailers are choosing to overlook the idea of mobile payment acceptance.

Here are stats that prove the importance of mobile payments:

About 45% of consumers use mobile payments out of convenience.

1 billion users will use in-store mobile payments by 2019.

An increase from $3.2 billion in 2014 to $487 billion by 2020 in US in-store mobile payments is predicted.

Millenials use contactless payments on a regular basis.

Over the next five years, mobile payments will reach about $3 trillion in volume.

There are 16 million Starbucks mobile app active users that make 8 million mobile payments per week.

Transactions globally are on mobile devices.

It is a great investment for a merchant to upgrade your point-of-sale (POS) to have near field communication (NFC) capabilities. If you’re not currently accepting mobile payments, you should start now, your customers who are already using mobile payments will thank you and your business will be ahead of the game as more businesses onboard mobile payment acceptance.

Posted in Best Practices for Merchants, Credit Card Reader Terminal, Credit Card Security, Mobile Payments, Near Field Communication, Point of Sale Tagged with: contactless payments, customers, merchant, mobile payment, Near Field Communication, nfc, point of sale, POS, transactions

May 18th, 2016 by Elma Jane

Terminals are ready, but the software isn’t – many merchants have EMV capable equipment, but has not been activated yet because it still needs to be certified.

The certification process includes security and compatibility tests.

For a small merchant, all you need to worry about is your equipment or software is EMV certified.

For software, developers, terminal manufacturers needs to get certification before they can deploy their products to merchants.

So many merchants who want to accept EMV, are now just waiting for their POS system to get necessary upgrades, which they can’t do until they’re certified.

Slower Checkout Time – common complaint by consumers. Dipping takes several seconds longer than swiping the card. There’s also a chance of forgetting your card because you have to leave your card inserted while waiting for the transaction to get approved.

The fastest Path to EMV – Depending on the nature of your business, the risk of landing yourself for credit card fraud is slim. The easiest way is to contact your merchant account provider and they will tell you what equipment and software you need and how much it will cost.

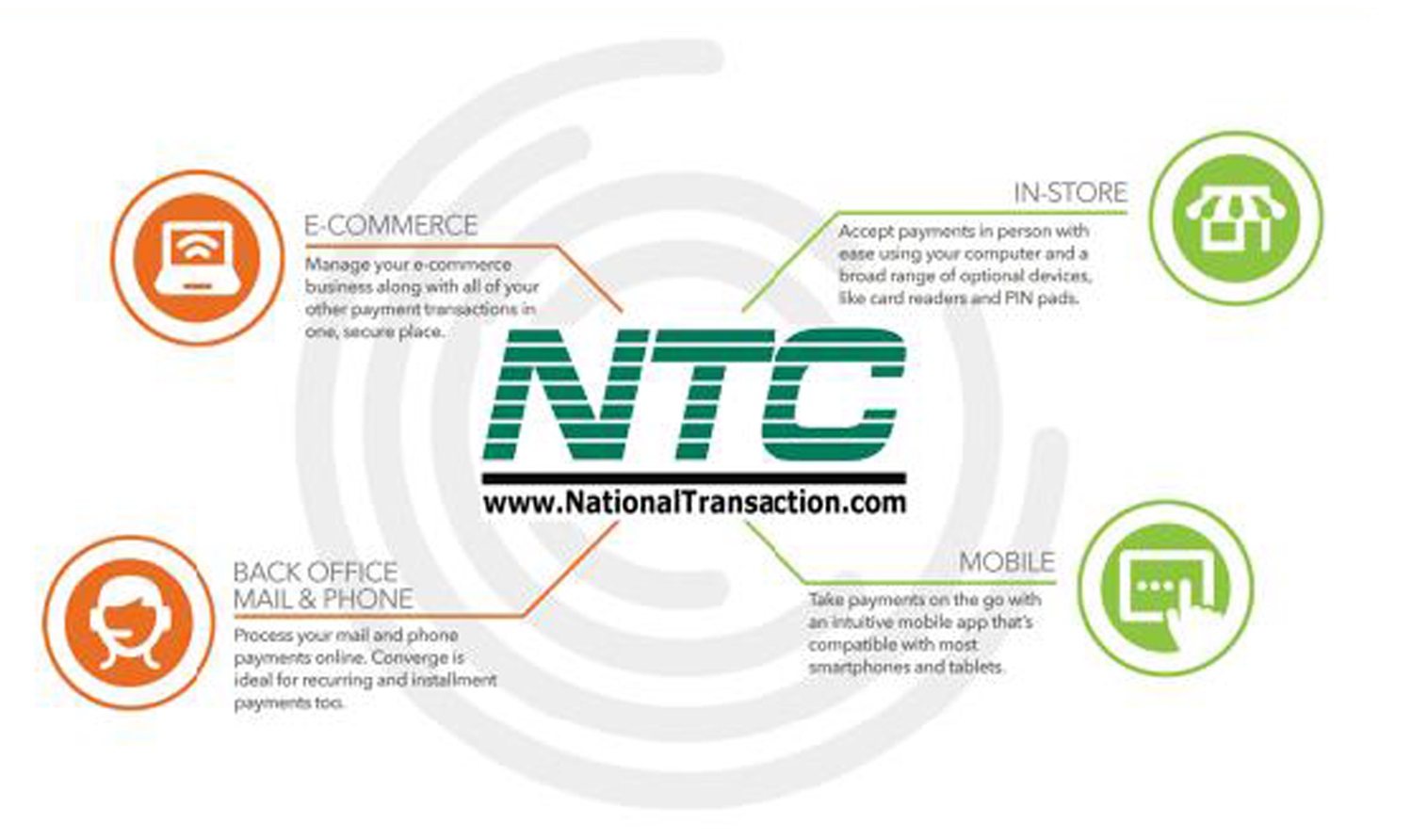

For our retail customers, we have the iCT250, the smart and compact desktop device designed for maximum efficiency. iCT250 offers a smart and effective payment experience on minimum counter space. Accept all electronic payment methods including EMV chip & PIN, magstripe and NFC/contactless.

For card-not-present, we have our payment gateway platform that accepts payments your way Online, In-Store and On the Go.

- E-commerce – manage your e-com business along with all of your other payment transactions in one, secure place.

- In-Store – accept payments in person with ease using your computer and a broad range of an optional device, like card readers and PIN pads.

- Back Office Mail & Phone – Process you mail and phone payments online. Converge is ideal for recurring and installment payments too.

- Mobile – Take payments on the go with an intuitive mobile app that’s compatible with most smartphones and tablets.

For more details give us a call at 888-996-2273 or check out our website for our products and services.

Posted in Best Practices for Merchants, Credit Card Reader Terminal, e-commerce & m-commerce, EMV EuroPay MasterCard Visa, Internet Payment Gateway, Mail Order Telephone Order, Merchant Account Services News Articles, Mobile Payments, Near Field Communication, Point of Sale, Smartphone, Travel Agency Agents Tagged with: card, card readers, Chip & PIN, consumers, contactless, credit card, customers, e-commerce, electronic payment, EMV, fraud, in-store, magstripe, merchant account, merchants, mobile, nfc, online, payment, payment gateway, PIN pads, POS, provider, Security, terminals, transaction

April 14th, 2016 by Elma Jane

Accepting credit card payments is a must if you’re planning to start a business. It’s good to know what is out there and how it applies to your situation. So you need to learn about credit card processing machines, depending on your business.

Here are some of the different types of credit card processing machines:

Dial-Up Terminal – the grandfather of credit card processing machines. Dial-up terminals use a phone line to connect with a credit card processing company. The advantage is that they are normally inexpensive than some higher-end options. The disadvantage is slower processor speed.

IP Terminal – connect the merchant over a high-speed internet connection. The advantage of IP terminal over dial-up terminal is speed. IP machines can process transactions as fast as 3 seconds as opposed the 10 to 25 seconds that a dedicated dial-up machine might take. IP terminals now cost about the same as dial-up units and that a single DSL link can accommodate more than one credit card terminal.

Wireless Terminals – the priciest yet most convenient type is a wireless machine that runs on a wireless network, much like your mobile phone.

Virtual Terminal – virtual terminals are computers running credit card processing software connected to a credit card reader. Virtual terminals are a great addition to an office because they don’t require a standalone credit card processing terminal.

There are many options available for your business, whether you’re e-Commerce, MOTO, In-Store or Mobile there’s a credit card processing machine and platform out there that will fit your business.

Give us a call to know more at 888-996-2273 or visit us at www.nationaltransaction.com

Posted in Best Practices for Merchants, Credit Card Reader Terminal, e-commerce & m-commerce Tagged with: card reader, credit card, credit card processing, e-commerce, merchant, mobile, moto, payments, terminal, virtual terminal

February 24th, 2016 by Elma Jane

Merchants can bring in new customers and encourage repeat business by using their point-of-sale terminal as a marketing tool. A point-of-sale terminal allows you to process payment and accept debit and credit cards, and generate more business by using the right tools.

Customize Receipts – a customized receipt becomes an advertisement. The customer knows where that receipt is from should they want to contact you.

Gift Cards Program – Gift card recipient are likely to spend over the face value of the card. Customers will appreciate simplified gift shopping.

Loyalty Program – Loyalty program makes customers think of your business first and encourages them to come back often to earn a reward.

Referral Rewards – Print an offer to reward referrals, so they can send people to you.

A merchant account is not just an expense by finding the right tool you can generate more income for your business!

visit www.nationaltransaction.com today, or call 888-996-2273 Extension 1

Posted in Best Practices for Merchants, Credit Card Reader Terminal, Point of Sale Tagged with: credit cards, customers, debit, gift Card, loyalty program, merchant account, merchants, payment, point of sale, terminal

October 19th, 2015 by Elma Jane

If you’re a merchant accepting credit cards, you’re probably aware that things are changing. As of October 1st, 2015, merchants are now liable for any fraudulent activity that occurs as a result of non-EMV-compliant. For those Merchants who haven’t yet updated their POS terminal, you need to talk with your processor to get a new equipment.

Things Merchant should know to be EMV ready:

What is EMV Chip Cards? Chip Cards are standard bank cards that are embedded with a micro-computer chip. Some may require a PIN instead of a signature to complete the transaction process. The new cards will still have magnetic stripes, at least for the time being, so you technically can continue to process payments with the same old equipment you’ve been using for years. But by refusing to upgrade your hardware, you are taking on responsibility for any fraud that might have otherwise been prevented with the new technology.

How does EMV Chip Cards Work? Instead of swiping your card, you are going to do what is called card dipping, which means inserting your card into a terminal slot and waiting for it to process.

When a Chip Card or EMV Card is dipped, data flows between the card chip and the issuing financial institution to verify the card’s legitimacy and create the unique transaction data.

This process isn’t as quick as a magnetic-stripe swipe. It will take a little longer for that transmission of data.

What Must a Merchant Do? For merchants and financial institutions, the switch to EMV chip cards means adding new in-store technology and internal processing systems, and complying with new liability rules. Merchants who have not yet purchased new POS Terminal may be held liable for fraud as of October 1st, 2015. Implementing EMV technology isn’t an option, it’s a necessity. If you are one of those in the retail business or retailers using mobile payment devices who missed the Oct. 1st deadline, you are already at risk. Upgrading should be a top priority.

Posted in Best Practices for Merchants, Credit Card Reader Terminal, Credit Card Security, EMV EuroPay MasterCard Visa, Point of Sale Tagged with: bank cards, chip cards, credit cards, data, EMV, financial institutions, magnetic stripes, merchant, mobile payment, PIN, POS terminal, processor, retail business, terminal slot

October 16th, 2015 by Elma Jane

With the EMV liability shift that takes effect in October 2015, how much you’ll be affected depends on how you process credit card payments.

For Card Present Transactions

If you use POS hardware or terminal that you need to swipe the credit card, then you’ll be facing the same EMV environment as retailers. October 1st is the start of the liability shift for fraudulent charges made with the card present transactions. The party who hasn’t made an investment in EMV security features will be liable.

For the card issuer, they need to invest in EMV security features, that’s why they came out with the chip cards, where all credit and debit cards have this security chips that are harder to counterfeit than magnetic strips.

For the merchant, they need to invest in EMV capable terminals or POS hardware that can take advantage of the card’s security chip.

If both parties have made the investment, then liability will be resolved in a similar manner to how it was before the shift. However, if only one party has adopted EMV technology, the party that didn’t make the investment will be held liable.

For Card Not Present Transaction (CNP)

If you process credit cards online, over the phone, or through an online payment gateway integrated, the new EMV standards won’t directly change the way you do business. You’ll still be processing EMV cards based on the customer’s credit card number.

Chances are Card-Not-Present transactions will experience an increase in fraud. Because of the EMV-technology in the Card Present Transaction, fraudster will likely turn their attention to the next target which is CNP,

but payment gateways and banks concerned about the vulnerabilities, will begin to adopt new standards to minimize their exposure.

If you’re processing CNP transactions stay up-to-date on the newest security developments, online security standards find more effective ways to navigate the new credit card security frontier.

Posted in Best Practices for Merchants, Credit Card Reader Terminal, Credit Card Security, EMV EuroPay MasterCard Visa, Mail Order Telephone Order, Point of Sale Tagged with: banks, Card Not Present Transaction, card-present transactions, chip cards, cnp, credit card, debit cards, EMV, merchant, payment gateway, payments, POS, terminal

October 8th, 2015 by Elma Jane

Rules have changed in regards to swiping credit cards October 1st, 2015 with the EMV Liability Shift; which may not cause much concern for most consumers, but for merchants.

EMV compliance isn’t a legal requirement. However, if you’re a merchant that accepts credit cards in-person, then you need to find out whether you’re meeting the EMV Standard. The new rule for the liability shift applies October 1st, regardless of the size or type of business.

What Is EMV Standard?

EMV stands for EuroPay, MasterCard, and Visa, the three companies that originally created the standard.

The EMV Shift is to provide enhanced security and prevent fraudulent activity with credit cards. Updated equipment is also necessary for processing the new computerized cards, and unfortunately, the responsibility of securing up-to-date hardware falls on the merchant.

Since card evolves more instead of cash in our society, fraud and data breaches is on the increase, and now a common occurrence. Adapting new technology is therefore necessary. A hassle for many merchants, but there are actually benefits from all parties involved in a credit card transaction.

Data shows that fraud decreases dramatically when EMV Standards are implemented In Europe. The region has experienced an 80% reduction in credit card fraud, while the USA has seen a 47% increase by NOT implementing EMV standards.

The new liability rules took effect on October 1st in the US, and any party that has not yet implemented EMV-compliant machines might now be liable for fraud committed with counterfeit chip cards. Note that this liability shift only applies to in-person transactions. Phone order and web order transactions will be dealt with as they always were.

For Merchants, it means you’ll eventually need to get new equipment for processing credit cards payments in-person (unless you’ve already done so not too long ago, as nearly all POS terminals sold in the USA nowadays are EMV compliant). For most business owners, it’s a good idea to implement the new system sooner rather than later.

Step to take as a Merchant Until you get your EMV equipment

- Ask for an official ID from customers whose credit card you process.

- Conduct some research to see which EMV system would be best for your business.

- Start shopping around for new payment processing options that are EMV compliant.

If you already have a machine that can process chip cards, you’re fully EMV-compliant.

If you don’t accept any in-person payments, then you’re all set.

If you do accept in-person payments and you do not have a chip card machine, chances are you’ll be fine for a little while. But those of you with a high risk of encountering a fake card (if you are a high-volume business with a large average ticket, for instance) should probably upgrade soon.

Fraudsters are going to be taking advantage of businesses that haven’t upgraded so it’s a great time to switch!

Check out NTC’s EMV/NFC Capable Terminal!

Posted in Best Practices for Merchants, Credit Card Reader Terminal, Credit Card Security, EMV EuroPay MasterCard Visa, Point of Sale Tagged with: chip cards, credit card transaction, credit cards, credit cards payments, EMV, EMV equipment, EuroPay, high risk, MasterCard, merchants, nfc, payment processing, POS terminals, visa

October 6th, 2015 by Elma Jane

If you accept credit cards and don’t know what EMV is here is what you need to know.

EMV stands for Europay, MasterCard and Visa. A credit card that had a chip embedded in it is an EMV. EMV Cards have been standard in Europe for more than 10 years because they’re more secure than magnetic stripe cards. Magnetic stripe cards doesn’t change, it has static data, which makes them easy to clone. The chip embedded card makes it more difficult and costly to counterfeit because the data that is transmitted changes each time the card is read. This means less fraud.

Liability Shift rules set by Visa and MasterCard as of October 1st. The liability for fraud carried out in physical stores with counterfeit cards belongs to the merchant if it has not yet upgraded its POS system to accept EMV-enabled chip cards.

- Calculate your risk – Consider the cost of replacing your point-of-sale (POS) terminal vs. potential risk. Whether you replace it now or at a later time, eventually all businesses will have to replace their POS terminals.

- Educate your staff – Educated employees translate to better-educated customers. Merchants can help customers better understand this change and what it means for them.

- Upgrade your POS system – Consider using an EMV compliant credit-card reader on a wireless device for an ultra-secure mobile solution. This is also a chance to upgrade other options, such as near field communication NFC technology, which lets consumers use their mobile devices to make payments at the point of sale.

National Transaction Terminals with EMV and NFC (near field communication) Capability To accept Apple Pay, Android Pay and other NFC Transactions at your business. You will need to adopt point-of-sale devices with NFC/contactless readers.

National Transaction offer a range of options to suite your specific needs.

If you’re using Virtual Merchant Mobile now called Converge please contact our office at 888-996-2273 to know your options.

Posted in Best Practices for Merchants, Credit Card Reader Terminal, Credit Card Security, EMV EuroPay MasterCard Visa Tagged with: Android Pay, Apple Pay, chip cards, contactless readers, Converge, credit cards, EMV, EuroPay, magnetic stripe, MasterCard, merchants, Near Field Communication, nfc, payments, POS, terminal, Virtual Merchant Mobile, visa

September 25th, 2015 by Elma Jane

National Transaction Terminals with NFC (near field communication) Capability to accept Apple Pay, Android Pay and other NFC payment transactions at your business. You will need to adopt point-of-sale devices with NFC/Contactless readers.

National Transaction offer a range of options to suite your specific needs.

Give us a call now! 1-888-996-2273 or go to www.nationaltransaction.com

Posted in Best Practices for Merchants, Credit card Processing, Credit Card Reader Terminal, Credit Card Security, Mobile Point of Sale, Near Field Communication, Point of Sale, Smartphone Tagged with: Android Pay, Apple Pay, contactless readers, Near Field Communication, nfc, payment, point of sale