Category: e-commerce & m-commerce

October 9th, 2015 by Elma Jane

Credit card fraud is much more difficult to prevent in a card-not-present transaction. In a face-to-face setting the merchant can inspect the card to ensure that it is valid and can verify that the cardholder is an authorized user on the account. None of these actions can be performed when the payment is submitted online or accepted by phone. As we moved in adopting EMV Technology, majority of fraud is going to migrate away from counterfeit and stolen cards towards the card-not-present transaction as happened in other countries.

A combination of best practices and fraud prevention tools can provide card-not-present merchants with strong fraud prevention capabilities.

Steps to avoid fraud and protect your business for a card-not-present transaction:

- Email Verification: Send a message to the email address provided by the customer requesting that the customer verify the email address is correct, you can ensure that the email is associated with the other information provided.

- Maintain PCI compliance:All merchants accepting card payments are now required to be compliant with the requirements of the PCI DSS (Payment Card Industry Data Standard) which sets the rules for data security management, policies, procedures, network architecture, software design and other protective measures.

- Security Code Verification. Requesting the three digit security code on the back of a credit card. Visa (CVV2), MasterCard (CVC 2) and Discover (CID) cards, and the 4-digit numbers located on the front of American Express (CID) cards. Card Security Codes help verify that the customer is in a physical possession of a valid card during a card-not-present transaction.

- Use an Address Verification Service (AVS): Enables you to compare the billing address provided by your customer with the billing address on the card issuer’s file before processing a transaction. AVS is good protection against card information obtained through means like phishing and malware because fraudster might not know the billing address.

- Use 3D Secure Service: MasterCard and Verified by Visa enable cardholders to authenticate themselves to their card issuers through the use of personal passwords they create when they register their cards with the programs. The liability of any fraudulent charges through the 3D service is picked up by the issuer, not the merchant.

- Verify the phone number and transaction information.Prior to shipping your products, call the phone number provided by the customer and verify the transaction information. Criminals may be unable to verify such information, because in their haste to max out the credit line before the fraud is discovered, they often order at random and do not keep records.

Posted in Best Practices for Merchants, e-commerce & m-commerce, Mail Order Telephone Order, Payment Card Industry PCI Security, Travel Agency Agents Tagged with: American Express, card-not-present, card-security, cardholder, cnp, credit card, Discover, EMV, MasterCard, merchant, Payment Card Industry, payments, PCI, visa

October 9th, 2015 by Elma Jane

In order to maintain some sort of order within PCI Compliance, VISA and MasterCard have created 4 risk levels that will apply to any particular business, for determining the risk level of a merchant.

| Merchant Level |

Description |

Validation Requirements |

| Level 1 |

Merchants processing over 6 million Visa transactions annually (all channels) or Global merchants identified as Level 1 by any Visa region. |

Annual Report on Compliance (ROC) by Qualified Security Assessor (QSA) or internal auditor if signed by officer of the company.

Quarterly network scan by Approved Scan Vendor (ASV).

Attestation of Compliance Form. |

| Level 2 |

Merchants processing 1 million to 6 million Visa transactions annually (all channels). |

Annual Self-Assessment Questionnaire (SAQ).

Quarterly network scan by ASV.Attestation of Compliance Form. |

| Level 3 |

Merchants processing 20,000 to 1 million Visa e-commerce transactions annually. |

Annual Self-Assessment Questionnaire (SAQ).

Quarterly network scan by ASV.

Attestation of Compliance Form. |

| Level 4 |

Merchants processing less than 20,000 Visa e-commerce transactions annually and all other merchants processing up to 1 million Visa transactions annually. |

Annual SAQ recommended.

Quarterly network scan by ASV if applicable.

Compliance validation requirements set by acquirer. |

Posted in Best Practices for Merchants, Credit Card Security, e-commerce & m-commerce, Payment Card Industry PCI Security Tagged with: MasterCard, merchant, PCI Compliance, visa

October 1st, 2015 by Elma Jane

The day the payments industry has pointed to for several years arrives today, a turning point in the U.S.‘s migration to EMV chip-and-PIN cards.

Rules set by Visa and MasterCard as of today, the liability for fraud carried out in physical stores with counterfeit cards belongs to the merchant if it has not yet upgraded its POS system to accept EMV-enabled chip cards. Banks will be issuing EMV Chip Cards.

An enormous change, as everyone learns to deal with the new technology that requires consumers to insert their cards and leave them in the store machines throughout a payment transaction, rather than swipe.

In a recent survey, less than a third of merchants overall have invested in EMV-compliant technology, and one study said 80 percent of small and midsize merchants have not upgraded their systems as of today’s liability shift.

Issuers are claiming to be more prepared than merchants, but according to the Smart Card Alliance, around 200 million chip cards have been issued to U.S. cardholders. That, however, is less than 17 percent of the approximately 1.2 billion payment cards in circulation.

What is clear is that today does not represent the end of the journey. The lack of preparedness at the physical point of sale, however, may be beneficial for card-not-present merchants.

Over the past few months, the mainstream media has awoken to the fact that implementing EMV does not mean fraud will disappear. Fraudsters quickly adapted to the difficulty of counterfeiting cards by attacking Card-Not-Present channels, where a chip has no effect.

In other markets, fraud migrated quite rapidly to card-not-present channels. It is necessary on e-commerce merchants to protect themselves with an array of tools, like device authentication, one-time passwords, randomized PIN pad and biometrics. Fraud mitigation tools like data analytics, address and CVV verification, 3D secure and tokenization. These services should be available from their merchant acquirer processor or gateway.

There should be a gradual reduction in card fraud over the next 12-18 months in spite of the delays in this country’s EMV migration. It’s going to take time for the technology to be adopted.

U.S. Merchants’ overall relative lack of preparedness for EMV may give e-commerce and mobile merchants time they didn’t think they would have to explore the options.

Sophisticated authentication technologies such as biometrics will help increase the security of card transactions. Device-based verification could be easily incorporated in an EMV transaction.

Banks have expressed interest more in using the phone as a biometrics. It’s all going to depend on what is the most convenient way to access your funds. The nice thing about biometrics is it’s meant to enable more convenience and stronger security.

Posted in Best Practices for Merchants, e-commerce & m-commerce, EMV EuroPay MasterCard Visa, Mobile Payments, Mobile Point of Sale, Point of Sale Tagged with: banks, biometrics, card fraud, card-not-present, chip cards, chip-and-PIN cards, e-commerce, EMV, gateway, merchant acquirer, merchants, mobile merchants, payments industry, point of sale, POS system, processor, tokenization, Visa and MasterCard

September 22nd, 2015 by Elma Jane

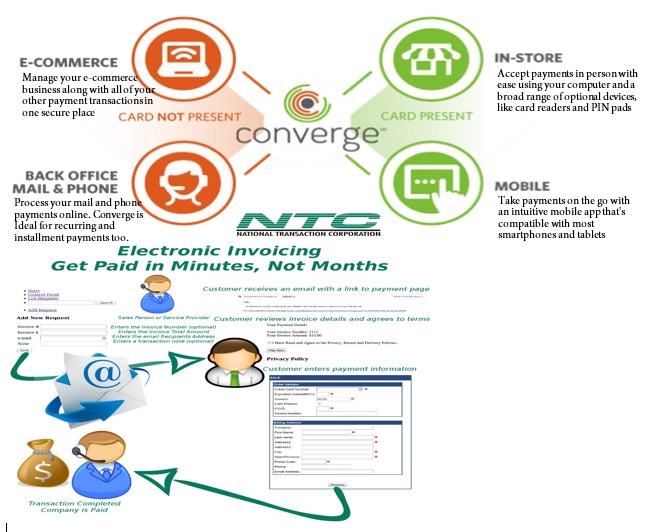

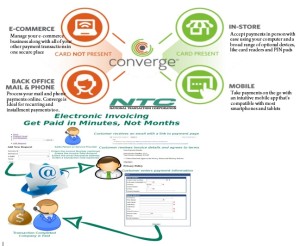

Virtual Merchant/Virtual Merchant Mobile now called Converge, is a popular product offering solutions for retail stores, Non Face to Face businesses along with E-commerce/Internet sites. Converege can be access anywhere with internet. Users can download the application on their smartphone or tablet. Converge also gives users the convenience of sending an invoice to customers electronically with NTC e-Pay!

For Retail store National Transaction offers the latest in EMV and NFC technologies. NTC customers can accept contactless payment with the same NFC technology used by Apple Pay, Google Wallet and SoftCard. NTC offers different solutions that cater to your business needs. For those already using a POS system, NTC integrates with most systems. NTC has you covered.

Posted in Best Practices for Merchants, e-commerce & m-commerce, Electronic Payments, Mobile Payments, Mobile Point of Sale Tagged with: Apple Pay, contactless payment, Converge, e-commerce, EMV, Google Wallet, nfc, POS system, smartphone, tablet, virtual merchant

September 11th, 2015 by Elma Jane

National Transaction Terminals with NFC (near field communication) Capability

To accept Apple Pay transactions at your business, you will need to adopt point-of-sale devices with NFC/contactless readers.

National Transaction offer a range of options to suite your specific needs:

Tablet solutions: Talech with iCMP device and NCR Silver.

Short-range wireless terminals for pay at the table: Bring the point-of-sale to your customers. Ideal for table-service restaurants, curbside pick-up, salons and more.

These terminals are all-in-one solutions with an integrated PIN Pad and printer. The short range terminals use secure, encrypted Bluetooth technology, allowing only the base and terminal to talk to each other, while also monitoring channels to prevent interference from other devices.

The Bluetooth terminals we offer are: VeriFone VX680B and Ingenico iWL220B. (Both Bluetooth Wireless)

Long-range wireless (cellular/mobile) terminals: Have a long-life battery and compact design, which allows you to process transactions anywhere your customers are ideal for deliveries, kiosks and more.

These terminals are all-in-one solutions with an integrated PIN Pad and printer. Phone lines and internet connections are not required to take advantage of our mobile payment solutions.

The GPRS wireless terminals we offer are: VeriFone VX680G and Ingenico iWL250G. (Both GPRS Wireless)

Countertop terminals:

Ingenico iCT250 – has a “magic box” cable management system that prevents cable tangle and clutter. The terminal boasts a color display for improved readability and ease of use.

Verifone VX520 – has a built-in secure software authentication process which prevents unauthorized software applications from being downloaded.

Ingenico iCT220 with iPP320 external PIN pad – has a “magic box” cable management system that prevents cable tangle and clutter, along with a black and white screen for crisp visual clarity. Combine with an iPP320 for a consumer- facing solution to support contactless payments. (Note: the iCT220 device only supports contactless transactions when connected to this external PIN pad).

Whether you need a stand-alone POS terminal, want to take advantage of your existing tablet or PC, or require a wireless or mobile solution, National Transaction Corp., offers numerous user-friendly options. No matter how your customer wants to pay, NTC will help you enable quick and easy transactions from Traditional credit and debit cards, gift cards, smart cards (or EMV), mobile or digital wallets like Apple Pay and eCommerce or MOTO transactions.

Start growing your business quickly by accepting all kinds of credit card payments and debit cards. Choose a state-of-the-art solution so you can accept payment in store or on your mobile device. With transparent pricing, live customer support, no cancellation fees and a secure platform, you’ll be confident you made the right partner for your business with National Transaction Corp.

Learn how easy it can be to accept any contactless or Apple Pay transactions.

Click here for more information about Apple Pay.

For Merchant Account Setup give us a call at 888-996-2273 or visit our website www.nationaltransaction.com

Posted in Best Practices for Merchants, e-commerce & m-commerce, Mail Order Telephone Order, Mobile Point of Sale, Near Field Communication, Point of Sale Tagged with: Apple Pay transactions, contactless readers, Countertop terminals, credit card, debit cards, Digital wallets, ecommerce, Gift Cards, mobile payment, moto, Near Field Communication, nfc, PIN pad, point of sale, POS terminal, smart cards, wireless terminals

June 5th, 2015 by Elma Jane

Traditionally, travel-related merchants have a difficult time obtaining merchant accounts. National Transaction Corporation (NTC) is a full service merchant account provider with extensive experience in the travel arena and related markets, servicing thousands of travel-related merchant accounts by specializing in non-cash electronic transactions. Our services include processing credit card transactions, gift card transactions, and e-commerce transactions, among others. We offer a full line of products including credit card terminals, cellular devices, supplies, and accessories for each model sold. We offer aggressive rates and pricing for mail/telephone order, retail/restaurant, wireless, and online transactions while specializing in the travel and high volume sectors of merchant processing, and we are proud to be the preferred merchant provider for ASTA.

NTC is dedicated to providing the highest caliber of service and solutions in the merchant processing industry. We actually answer the phone when you need assistance! NTC has a team of dedicated employees providing personalized service to each account holder and are available directly through their toll free number, never hidden behind a menu system. Our excellent service truly separates us from everyone else in the industry. The principals of NTC have extensive experience in the processing arena for over 25 years, with experience in all facets of operation, including credit cards, credit initiation, credit investigation, loss prevention, deployment, and customer and terminal support. We employ internal sales associates as well as independent sales agents who offer many opportunities through their referral reward services and Independent Sales Organization (ISO) programs.

NTC’s online gateway allows for processing transactions, reviewing account history, and interacting with various shopping cart and accounting applications such as QuickBooks, Peachtree, and many other titles. Reservation software such as Trams are compatible and integrate well with all National Transaction merchant accounts. Whether you are a travel agency or an independent agent, we offer many solutions that cater to the travel industry and will increase your revenue with quicker deposits into your bank account.

Travel environments are unique in that your transactions are usually keyed; there is almost always a delayed delivery period, and large ticket transactions are not uncommon since one card holder may be paying for multiple tickets. They also tend to be seasonal, with peak season months generating an unusual spike in their “average” monthly volume, and charge-back’s pose a potential threat by travelers who are unable to complete their trip. Combine even a few of these factors together and you have cause for a reserve, or even account termination. National Transaction Corp specializes in understanding what makes your transactions unique, as a travel agent, and how they affect your merchant account.

The importance of customer service is something that is over looked when merchants compare the overall cost of monthly fees with their merchant account. That is, until the moment they need assistance with their account. Whether searching for missing deposits, having problems processing transactions, issuing refunds, processing voids, or questioning their billing statement, a merchant should always remember you get what you pay for. If you wonder why they can offer you no monthly fee, they are offering you no LIVE customer support. Customer support for them will come via means of email. You will wait hours for answers, and even days for a simple confirmation or general email, let alone a resolution.

National Transaction Corporation has over 17 years of dedication and experience in providing quality solutions in the credit card processing arena. From internet e-commerce applications to food stamp processing, from small start up businesses to fortune 500 companies, NTC has a complete product selection to customize a solution to grow with your business. We at NTC pride ourselves on being a full service, member service provider. It is our mission to provide the same dedication and service in maintaining your business as you experience in us earning your business. NTC will provide service after the sale. It is that service that sets us apart! For more information, contact NTC for world class service and solutions.

Contact National Transaction Corporation today at 888-996-2273 to see how we can help you with your travel merchant account, or visit us online at www.nationaltransaction.com for more information.

by Elizabeth Cody (Travel Research Online)

Posted in Best Practices for Merchants, Credit card Processing, e-commerce & m-commerce, Gift & Loyalty Card Processing, Merchant Account Services News Articles, Merchant Cash Advance, Travel Agency Agents Tagged with: ASTA, bank account, billing statement, credit card terminals, credit card transactions, credit cards, customer service, deposits, e-commerce, e-commerce transactions, electronic transactions, gift card transactions, Independent Sales Organization, ISO, merchant account provider, merchant accounts, merchants, service provider, travel, travel agency, travel agent, travel industry

September 30th, 2014 by Elma Jane

Email remains king in the types of digital marketing businesses. Fifty four percent of businesses view email as the most effective form of Internet marketing. However, a number of other types of digital marketing tactics aren’t far behind. More than 40 percent of the businesses surveyed believe optimized websites and blogs, search engine optimization (SEO) and social media are among the most successful online marketing tactics. Mobile marketing and e-commerce marketing are viewed as the least effective forms.

Contributing to email marketing’s success is the ease in which it is conducted. Eleven percent of the businesses surveyed thought email was one of the most difficult types of digital marketing to execute. Social media tops the list, with nearly 50 percent of businesses saying it was the hardest to accomplish.Content marketing and SEO were among the other toughest tactics to execute. Overall, the vast majority of businesses using some form of digital marketing report seeing positive results from it.

Businesses have a wide range of motives for using Internet marketing. Wanting to increase customer engagement, sales revenue, leads for their sales teams and brand awareness were the most important reasons. Reducing marketing and customer service costs are surprisingly least important. Majority of the businesses believe their digital marketing efforts are only getting better. In order to achieve all of their goals, there are a number of challenges businesses are facing:

The most challenging obstacle to success is clearly the lack of an effective digital marketing strategy.

Followed by an inadequate budget to fund programs.

Other challenges business must overcome to achieve better digital marketing results include a lack of training and expertise.

Inability to prove a return on investment and increasing competition.

Posted in Best Practices for Merchants, e-commerce & m-commerce Tagged with: Content marketing, customer service, digital marketing, digital marketing businesses, e-commerce marketing, email, Internet marketing, Mobile marketing, search engine optimization, SEO, social media, websites

September 29th, 2014 by Elma Jane

If your retail business products sells only in-store, then you’re falling behind. Consumers in the digital age expect options when they shop, and if you’re not offering those choices, your customers may pass you by for a more tech-savvy competitor. Consumers go into stores, evaluate products and buy online, or research online and go into the store for purchase. The two worlds have merged, if you’re not covering both spectrums, you’re missing out.

Recent research by UPS showing 40 percent of today’s shoppers use a combination of online and in-store interactions to complete their purchases. The days of physical stores being separated from online shopping are over. They’re no longer channels that are happening on their own. The UPS survey found that a large chunk of online shoppers cross channels during their shopping path. Be present on both channels and take advantage of that.

It’s not always possible or economic for an online-only retailer to open up a physical storefront, but existing brick-and-mortar stores or wholesalers can easily introduce an e-commerce component to their sales to expand their customer reach. Online sales help reach consumers that may not otherwise be able to purchase your products. Even if your company’s main focus is creating a personalized in-store experience, there are still ways to capture the online shopper market. In addition to giving consumers a way to research your products before coming in-store to purchase your offerings, you can offer people a way to conveniently buy items they already know they want.

For all the advantages a multi-channel sales strategy can give a retailer, there are still some challenges to this approach. Managing inventory versus cash flow and ensuring even demand on both channels have been company’s two greatest challenges in balancing in-store and online sales. Creating demand is how companies set themselves apart from competition. The secret sauce. The challenge is making sure that retail operations have a turnover ratio that works for the shipping schedules from the main warehouse. This isn’t a problem for e-commerce businesses, because product can be packaged and shipped as fast as it gets produced. But an omnichannel company has to take retail and e-commerce into account when stocking a warehouse.

There are a few different strategies retailers can use to help keep their sales operations well-balanced. Offering different items online versus in-store, to avoid inventory competition (i.e., selling seasonal or discontinued items online and current items in-store). Requiring a minimum order for online purchases or grouping products together rather than selling them individually to make e-commerce more worth your while.

The best way to balance a multi-channel sales strategy is to take a unified view of consumers online and offline by connecting their on- and offline behaviors via technology. Some of the retailers questions have is how to connect a person offline with what they buy online, how to recognize who they are in the store and know what they look at on your website, because people are switching back and forth. Link behaviors online with a unique ID through email or a mobile app, since 66% of customers use smartphones in-store.

Even if your business can’t actually sell and ship products via e-commerce,it’s still important to be in tune and up-to-date with the way customers want to interact with you on the Web. People are on the go, researching on phones and tablets. If you’re not savvy to what’s happening out there and don’t have the best-in-class SEO, you’ll miss out. You still need to engage in the digital world, even if it’s not always obvious.

Posted in Best Practices for Merchants, e-commerce & m-commerce Tagged with: brick and mortar, business products, consumers, customers, digital world, e-commerce, email, mobile app, multi-channel sales, online and in-store, online shoppers, online shopping, phones, products, retail business, SEO, shoppers, Smartphones, tablets, web

September 15th, 2014 by Elma Jane

Visa has taken advantage of the hoopla surrounding Apple’s application of digital account tokens to replace card numbers for online and mobile purchasing by initiating the roll out of its Token Service to US clients.

Visa Tokens will be made available to issuing financial institutions globally, starting with US banks next month, and followed by a phased roll-out overseas beginning in 2015. The technology has been designed to support payments with mobile devices using all major mobile platforms.

More than 750 staff from across the Visa organisation globally were involved in the effort, working closely with initial launch partners – financial institutions, merchants and processors to ensure the ecosystem was ready. Today, Visa is making these services available and believe it will help transform connected devices and wearables into secure payment vehicles.

Visa Token Service replaces sensitive payment account information found on plastic cards with a digital account number or token. Because tokens do not carry a consumer’s payment account details, such as the 16-digit account number, they can be safely stored by online merchants or on mobile devices to for e-commerce and mobile payments.

The release of the service has been given added urgency by a spate of successful hacks on merchant card data stores, such as the recent plundering of card account data at Home Depot and Target.

MasterCard has its own equivalent Digital Enablement Service, which will be released outside of the US in 2015.

Posted in Best Practices for Merchants, Credit Card Security, e-commerce & m-commerce, Mobile Payments, Visa MasterCard American Express Tagged with: account details, card, card account data, card data, data, digital account, digital account number, e-commerce, financial institutions, MasterCard, merchant card data, Merchant's, mobile, Mobile Devices, Mobile Payments, mobile platforms, online merchants, payments, processors, Token Service, tokens, visa, Visa organisation, Visa Token Service, wearables

September 9th, 2014 by Elma Jane

The use of customer data can help you make smarter decisions that can improve your store, enhance the shopper experience, and increase conversions. When used incorrectly, however, data can waste resources and alienate your visitors.

Ways that ecommerce merchants commonly misuse data.

Collecting Unnecessary Data

Big Data analytics and reporting tools can put a lot of information in your hands, but that doesn’t mean you should collect and track every single metric. Don’t waste space and bandwidth collecting information that is not essential in your business. Unnecessary data can create noise that slows down the analytics process. Gathering and analyzing information you don’t need can distract you from the metrics that matter. Collecting too much data can create security headaches. The best defense against breaches is to not have data to steal. If you don’t need it, don’t collect it.

Determine your store’s key performance indicators before collecting any information. A good way of doing this is to examine each metric and ask yourself whether it’s just nice to know or is something that you can actually act on. While it may be nice to know that a particular customer has a high Klout Score, that metric probably won’t do anything for your bottom line. It’s better to not bother with it. Key metrics vary from one business to the next. For most ecommerce sites, the important metrics usually include conversion rate, traffic sources, and on-site browsing activities.

Creeping-out Shoppers

Most retailers do this inadvertently when they’re trying to customize the shopper experience. A certain amount of personalization can provide value and convenience to users, but you also have to draw the line between cool personalization and creepy. Sending emails with tailored product recommendations is a good way to increase conversions. But you have to be careful with how you execute it, so that you don’t appear too intrusive. The same goes for remarketing banner ads.

Ignoring Qualitative Information

Numbers can produce many insights, but focusing solely on that data can create an incomplete view of your company. Best data strategies make use of both quantitative and qualitative information. Go beyond the numbers to get the pulse of your customers by collecting feedback through social interactions, customer service logs, surveys with open-ended questions and more. Qualitative information can complement and validate the hard numbers.

Using Data to Justify a Decision or Hypothesis

When it comes to data collection, many merchants fall into the confirmation bias trap, wherein they interpret the information to confirm their existing beliefs or to justify their decisions. Using data this way causes you to ignore information or results that aren’t in line with your beliefs and could result in you missing opportunities. Say a company has so much faith in its new marketing strategy that when website traffic improves, the staff deems the campaign a success without looking at the conversion or retention rates. If the staff had ignored initial biases and looked at the big picture instead, they could have identified flaws and found ways to correct them. The key to addressing this is to have an open mind when interpreting information. This can be difficult, especially when you’re too close to your business. Consider a third-party specialist who can remain objective, to help make the right decisions.

Posted in Best Practices for Merchants, e-commerce & m-commerce Tagged with: breaches, business, conversion rate, customer, customer data, customer service, data, ecommerce, ecommerce merchants, Merchant's, rate, retention rates, Security, sources, tools, traffic