To be responsive to the needs of our merchants and to meet that needs NTC offers next day funding. This is a value added service for customers and businesses that need to have their funds available quickly.

With more than 20 years of experience, National Transaction offers a variety of electronic payment services and technology for Retail and Ecommerce industries. From Travel, Medical Industry, Charitable Institution and Franchise.

Our services include:

Loans/Funding Program

Credit and Debit Card Processing

Currency Conversion

Electronic Checks

Electronic Invoicing

Gift and Loyalty Card Programs

Mobile and Online Solutions

Shopping Cart E-commerce Payment Gateway

NTC e-Pay – is an Electronic Invoicing that made simple with NTC e-Pay! Free Setup, nothing to integrate; secure and fast.

Invoice customers Electronically with NTC e-Pay. Our e-Pay Platform can help Merchants bring new customers and encourage repeat business.

Our Virtual Merchant Gateway – accept payments your way! Online, In-Store and On the Go. A payment platform that flexes with your business.

NTC Business Loans – Fast, Affordable, and Simple Application Process.

MediPaid – a medical health insurance claims payment. Delivering paperless, next-day deposits for Health Insurance Payments.

NTC provides services to thousands of customers. NTC maintains a one on one relationships with all its merchants providing them with 24/7 customer service and technical support!

To know more about our product and services give us a call at 888-996-2273

Learn more about the full range of payment capabilities offered by Converge, an omni-commerce platform that lets you accept payments your way. Online, In-Store and On the Go!

Accept a full range of payment methods:

Credit Cards

Debit Cards

Electronic Checks

Gift Cards

Electronic Benefit Transfer (EBT)

Cash

Advanced features also include:

Available enhanced security features, including EMV, encryption and tokenization

Detailed reporting with up to 12 months of data storage

Customizable payment screens

User permission management for up to 5,000 users

National Transaction Corporation accept payments wherever you are with security while having a peace of mind for you and your customers. Furthermore, flexible solutions that empower your business growth in addition to world class support for complex integrations and answers to your toughest questions. Let our payment specialist find the right solution for your electronic payment needs. We offer transparent pricing and services that work with your existing technology to provide a low cost automated billing and collection solution.

Call now at 888-996-2273 and get a FREE Rate Review!

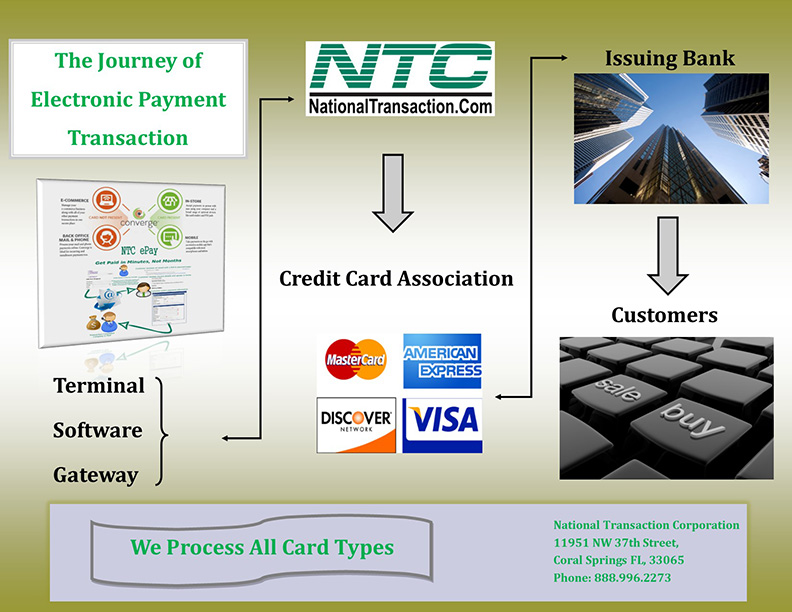

Let’s talk about your money, and how to make more of it. Today money is taking on a new form. It’s digital, it’s electronic and it’s everywhere and anywhere 24/7/365.

Payment acceptance is key to making more money. You don’t make more money by not accepting a transaction, and making the experience convenient and safe to your customer can bring loyalty.

Let’s break down a transaction.

Cash, but that would mean that the customer has to be in front of you. You could take checks, those are safe to mail, but then you don’t have your money until you drive to the bank and cash or deposit the check.

So how do we easily and securely transfer funds for a transaction? The answer lies in digital or electronic payments. Accepting credit cards, debit cards, ebt cards or even gift & loyalty cards and electronic checks. These provide secure and convenient ways to complete transactions for your customers. If you want to make more money, make it easy for customers to spend it while making it faster for you to receive it. That’s where a merchant account comes in.

A merchant account allows you to deposit funds directly into your bank account in as little as a few hours. Whether the customer swipes their card into your smartphone, calls it in over the phone or keys it into your web site, just having a merchant account can be a huge advantage over competitors.

It allows you to conduct transactions in more ways than cash or checks alone. Transactions are recorded automatically and can easily be reconciled for both customer and merchant. Most importantly it widens the opportunities to conduct sales to the widest customer audience possible.

No matter what you sell or how you sell it, the sale is only complete once the funds are transferred from one party to the other.

It’s important to recognize your missed opportunities. Could accepting electronic payments help increase your revenue stream? We’re here to help you make more money, let us show you the many ways we can do just that. Let’s talk, 888-996-CARD (2273)

To be responsive to the needs of our merchants and to meet that needs, NTC offers next day funding in addition to the value added service for customers and businesses that need to have their funds available quickly.

National Transaction also offers a variety of electronic payment services and technology for businesses; with more than 15 years of experience.

Our services include:

Currency Conversion

Credit and debit card processing

E-commerce and gateways

Electronic checks

Gift and loyalty card programs

Mobile processing

Cash advances and loans/funding program

NTC e-Pay and MediPaid

NTC e-Pay – is an Electronic Invoicing that made simple with NTC e-Pay!

Free Setup, nothing to Integrate, Secure, and Fast. Invoice customers Electronically with NTC e-Pay. In addition, our e-Pay Platform can help Travel Merchants bring new customers while encouraging repeat business.

Our Virtual Merchant Gateway – accept payments your way! Online, In-Store and On the Go. Another payment platform that flexes with your business.

NTC Business Loans – Fast yet Affordable and most of all Simple Application Process.

MediPaid – another medical health insurance claims payment. Delivering paperless and next-day deposits for Health Insurance Payments.

Furthermore, NTC provides services to thousands of customers. NTC maintains a one on one relationships with all its merchants consequently providing 24/7 customer service and technical support!

To know more about our product and services call us now! 888-996-2273

MerchantConnect is a great tool for merchants because it contains all the information that a merchant needs to manage their electronic payment activity. Furthermore, it’s fast, easy and secure!

Merchant can either view or update account information and make changes.

Find copies of statements.

Furthermore find valuable products and services to help merchant with their business.

View recent deposits and other information about account activity including:

Batch Details

Chargeback

Retrieval Status

Deposit History

The merchant can also find news and information to help manage payments at your business. Learn how to:

Best Qualify Transactions

Reduce Risk

Manage Chargebacks

Find reference guides to help operate your payment terminal

The merchant can also utilize the BIN Lookup when you need to inquire about which bank issued a particular card. Simply enter the first six digits on the card and you will receive the information on the issuing bank, including contact information.

If you need a to set-up an account and want to use this tool give us a call at 888-996-2273

To be responsive to the needs of our merchants and to meet that needs NTC offers next day funding. This is a value added service for customers and businesses that need to have their funds available quickly.

With more than 15 years of experience, National Transaction offers a variety of electronic payment services and technology for businesses.

Our services include:

Currency Conversion, credit, and debit card processing, e-commerce and gateways, electronic checks, gift and loyalty card programs, mobile processing, cash advances and loans/funding program. We also have NTC e-Pay and MediPaid.

NTC e-Pay – is an Electronic Invoicing that made simple with NTC e-Pay! Free Setup, Nothing To Integrate, Secure, and Fast. Invoice customers Electronically with NTC e-Pay. Our e-Pay Platform can help Travel Merchants bring new customers and encourage repeat business.

Our Virtual Merchant Gateway – accept payments your way! Online, In-Store and On the Go. A payment platform that flexes with your business.

NTC Business Loans – Fast, Affordable, and Simple Application Process.

MediPaid – a medical health insurance claims payment. Delivering paperless, next-day deposits for Health Insurance Payments.

NTC provides services to thousands of customers. NTC maintains a one on one relationships with all its merchants providing them with 24/7 customer service and technical support!

To know more about our product and services give us a call at 888-9962273

A payment processor is a company often a third party appointed by a merchant to handle credit card transactions for merchant acquiring banks. They are usually broken down into two types: Back and Front-End.

Back-End Processors accept settlements from Front-End Processors and, via The Federal Reserve Bank, move the money from the issuing bank to the merchant bank.

Front-End Processors have connections to various card associations and supply authorization and settlement services to the merchant banks’ merchants. In an operation that will usually take a few seconds, the payment processor will both check the details received by forwarding them to the respective card’s issuing bank or card association for verification, and also carry out a series of anti-fraud measures against the transaction.

Additional parameters, including the card’s country of issue and its previous payment history, are also used to gauge the probability of the transaction being approved.

Once the payment processor has received confirmation that the credit card details have been verified, the information will be relayed back via the payment gateway to the merchant, who will then complete the payment transaction. If verification is denied by the card association, the payment processor will relay the information to the merchant, who will then decline the transaction.

Modern Payment Processing

Due to the many regulatory requirements levied on businesses, the modern payment processor is usually partnered with merchants through a concept known as software-as-a-service (SaaS). SaaS payment processors offer a single, regulatory-compliant electronic portal that enables a merchant to scan checks “often called remote deposit capture or RDC”, process single and recurring credit card payments (without the merchant storing the card data at the merchant site), process single and recurring ACH and cash transactions, process remittances and Web payments. These cloud-based features occur regardless of origination through the payment processor’s integrated receivables management platform. This results in cost reductions, accelerated time-to-market, and improved transaction processing quality.

Payment Processing Network Architecture

Typical network architecture for modern online payment systems is a chain of service providers, each providing unique value to the payment transaction, and each adding cost to the transaction. Merchant>Point-of-sale SaaS> Aggregator >Credit Card Network> Bank. The merchant can be a brick-and-mortar outlet or an online outlet. The Point-of-sale (POS) SaaS provider is usually a smaller company that provides customer support to the merchant and is the receiver of the merchant’s transactions. The POS provider represents the Aggregator to merchants. The POS provider transaction volumes are small compared to the Aggregator transaction volumes. The POS provider does not handle enough traffic to warrant a direct connection to the major credit card networks. The merchant also does not handle enough traffic to warrant a direct connection to the Aggregator. In this way, scope and responsibilities are divided among the various business partners to easily manage the technical issues that arise.

Transaction Processing Quality

Electronic payments are highly susceptible to fraud and abuse. Liability to merchants for misuse of credit card data creates a huge expense on merchants, if the business were to attempt mitigation on their own. One way to lower this cost and liability exposure is to segment the transaction of the sale from the payment of the amount due. Some merchants have a requirement to collect money from a customer every month. SaaS Payment Processors relieve the responsibility of the management of recurring payments from the merchant and maintain safe and secure the payment information, passing back to the merchant a payment token. Merchants use this token to actually process a charge which makes the merchant system fully PCI-compliant. Some payment processors also specialize in high-risk processing for industries that are subject to frequent chargebacks, such as adult video distribution.

A solution for mobile commerce will be needed eventually, whether you’re an ecommerce merchant or you run a brick-and-mortar shop.

There are mobile payment platforms for digital wallets, smartphone apps with card-reader attachments, and services that provide alternative billing options. Here is a list of mobile payment solutions.

Boku enables your customers to charge their purchases directly to their mobile bill using just their mobile number. No credit card information, bank accounts or registration required. The Boku payment option can be added to a website, mobile site, or app. Price: Contact Boku for pricing.

Intuit GoPayment is a mobile credit card processing app from Intuit. It accepts all credit cards and can record cash or check payments. Intuit GoPayment transactions sync with QuickBooks and Intuit point-of-sale products. Intuit GoPayment works with iOS and Android devices and provides a free reader. Price: $12.95 per month and 1.75 percent per swipe, or 2.75 percent per swipe and 3.75 per keyed transaction.

iPayment MobilePay is a mobile payment solution from Flagship Merchant Services and ROAMpay. The service accepts all major cards and can record cash transactions. To help build your customer database, the app completes customer address fields for published landlines. The app can handle taxes, tips, and can record transactions offline. You can use the service month-to-month. The app and the reader are free. Price: $7.95 per month; Each transaction costs $0.19 plus a swipe fee maximum of 1.58 percent, or a key fee between 1.36 and 2.56 percent.

ISIS mobile commerce platform enables brick-and-mortar stores to collect payments (via an NFC terminal) from the mobile devices of their customers. Provide your customers with a simplified checkout process through the contactless transmission of payments, offers, and loyalty integrated in one simple tap. Price: Isis does not charge for payment transactions in the Isis Mobile Wallet. Payment transaction fees will not be increased by working with Isis.

LevelUp is mobile payment system that uses QR codes on smartphones to process transactions. Use LevelUp with a scanner through your POS system, or use a standalone scanner with a mobile device. You can also enter the transaction through the LevelUp Merchant App, using your smartphone’s camera to read the customer’s QR Code and entering the amount to complete the transaction. LevelUp also provides tools to utilize customer data. Price: LevelUp charges a 2 percent per transaction fee. Scanner is $50; tablet is $200.

MCX is a mobile application in development by a group of large retail merchants. Details on the solution are vague, but MCX is intended to offer a customizable platform that will be available through virtually any smartphone. MCX’s owner-members include a list of merchants in the big-box, convenience, drug, fuel, grocery, quick- and full-service dining, specialty-retail, and travel categories. Price: To be determined.

mPowa is a mobile payment app to process credit and debit card transactions, and record cash and check sales. mPowa will soon launch its PowaPIN chip and PIN reader for the EMV (“Europay, MasterCard, and Visa”) card standard. (Developed in Europe, EMV utilizes a chip embedded in a credit card, rather than a magnetic strip.) The EMV standard is likely to gain footing to combat credit card fraud. mPowa is a good solution for merchants with a global presence. Price: 2.95 percent per transactions, or .25 percent or $0.40 per transaction when used as a current processor’s point-of-sale system.

PayAnywhere is a solution to accept payments from your smartphone or tablet with a reader. It features an automatic tax calculation based on your current location, discounts and tips, inventories with product images and data, and more. Bilingual for English and Spanish users. PayAnywhere provides a free credit card reader and free app, available for iOS and Android. Price: 2.69 percent per swipe, 3.49 percent plus $0.19 per keyed transaction.

PayPal Here gives you a variety of options for accepting payments, including credit cards, PayPal, check, record cash payments, or invoice. With PayPal Here, you can itemize sales totals, calculate tax, offer discounts, accept tips, and manage payment email notifications. Available for iOS and Android. The app and reader are free. Price: 2.75 percent per swipe and 3.5 percent plus $0.15 per manually-entered transaction.

Square is a simple approach to mobile credit card processing. Square provides a free point of sale app and a free credit card reader for iPhones and iPads. Square offers a selection of tools to track sales, taxes, top-purchasing customers, and more. Square’s pricing is on the higher end, but with no monthly fee Square may be a good fit if you have infrequent mobile transactions. Price: 2.75 percent per swipe and 3.5 percent plus $0.15 per manually-entered transaction.

As we move to smartphones and tablets as payment methods security and privacy concerns are a real issue. With recent NSA leaks shedding light on our data and the access others have to it, we have to consider security, privacy and health implications. This year alone e-commerce transactions on smartphones and tablets during the holiday season are set to grow by 15%. Although tablets, not smartphones will drive the bulk of that growth, smartphones are set to overtake mobile-commerce payments over the next 5 years. Tablet payments in the U.S. alone are expecting to reach $26 billion in transactions. Currently tablets are more convenient for m-commerce due to their size, but as far as the future of electronic payment processing, smartphones are where it’s at.

The smart merchant sees this coming and realizes frictionless transactions increase sales. The more comfortable and less complicated a transaction is for a customer, the better. Smartphones, tablets, PCs, laptops and more can already process electronic transactions from credit and debit cards, gift cards, electronic checks and more. Money movement is easier than ever and more convenient than cash. Cash is king however in situations where internet connectivity and power are an issue. In India for example, a poor electric grid makes power outages a common occurrence. During natural disasters, when resources are badly needed, power outages or severed internet communications mean no electronic transactions can be processed. So physical currency remains a must, in the future we may see payment technology evolve to where digital money like crypto currency (BitCoin) may be stored on the device itself similar to having cash. As these electronic payment systems evolve, merchants need to position themselves to accept what their market prefers to transact with.

The smart citizen also sees this coming and has concerns that things like a National ID program being established may compromise their privacy.

As an extreme example of electronic transactions, a nightclub in Spain used subdermally implanted RFID chips in a woman that allowed patrons to pay for food and beverages without a credit card.

Electronic Check also known as Echeck – is an electronic version of a Paper Check. Electronic Checks allow merchants to convert paper check payments made by customers to electronic payments that are processed through the (ACH) Automated Clearing House Network. It’s a fast, efficient, and secure way to process check payments.

Because of the many benefits and increased security methods that electronic checks offer, this method of payment is quickly growing in popularity. In 2007, electronic check conversion increased by 30%, with more than 3.1 billion paper checks converted to echecks through in-store transactions. Familiarizing yourself with how electronic checks work, the benefits and security features they offer, and how you can get started with electronic check conversion will save you time and money and help you provide greater protection for your business and your customers.

How it works:

Electronic check conversion is a simple method of processing payments, and the changes to how you do business are minimal. One of this method’s greatest advantages is that you can electronically submit checks instead of having to physically take them to the bank, saving you time and increasing employee efficiency.

When you receive a paper check payment from your customer, you will run the check through an electronic scanner system supplied by yourmerchant service provider likeNational Transaction Corporation (NTC). This virtual terminal captures the customer’s banking information and payment amount written on the check. The information is transferred electronically via the Federal Reserve Bank’s ACH Network, which takes the funds from your customer’s account and deposits them to yours.

Once the echeck has been processed and approved, the virtual terminal will instantly print a receipt for the customer to sign and keep. Employees should mark the paper check as “void” and return it to the customer. Your merchant transactions will be available online for viewing with customized detailed reporting, which may vary in features depending on the merchant service provider you choose.

Using electronic check conversion to process your customers’ payments holds many benefits over paper checks:

Benefits:

1. Received Funds Sooner. Businesses that use electronic check conversion have funds deposited almost twice as fast as those using the traditional check processing method, with billing companies often receiving payments within one day.

2. Reduced Fraud and Fewer Errors. Echecks are processed using an automated system, which cuts down the number of people who must handle the check, reducing the potential for error and fraud. Merchant service providers (NTC) also maintain, monitor, and check files against negative account databases that store information about individuals or companies that have past records of fraud to help decrease fraudulent activity.

3. Reduced Processing Costs. In general, the cost to process an echeck is substantially less than that of paper check processing or credit card transactions. Echecks require less manpower to process and eliminate incidental costs such as deposit and transaction fees that accompany paper checks. With Echecks, you can save up to 60% in processing fees.

4. Sales Increase. If your business didn’t accept paper checks in the past, you can expand the payment options available to your customers and increase sales by offering echecks. If you are converting from accepting paper checks to echecks, you can still expand your customer base by being able to accept international and

out-of-state checks without the worry of fraud. Echecks require account validation and customer authentication processes that identify bad checks within seconds.

5. Safe, Simple and Smart. Electronic check conversion is easy to set up and relies on the ACH Network for processing, the same reliable and trusted funds transfer system that handles Direct Deposit and Direct Payment. Plus, echecks are a smart choice for the environment, helping to reduce more than 67.4 million gallons of fuel used and 3.6 million tons of greenhouse gas emissions created by transporting paper checks.

Increase security with electronic checks – Electronic check conversion leverages the latest information protection features such as encryption and message authentication. Because of this, many retail merchants, merchant service providers, and financial institutions consider it to be one of the most secure payment methods in the electronic payment processing industry.

Authentication – Merchants must verify that the person providing the checking account information has the authority to use that checking account. There are a number of authentication services and products available to merchants, including:

Digital Signatures or Digital Certificates are a way of Encrypting information that gives the receiver a more reliable indication that the information was sent by the claimed sender. They are used by programs on the Internet to confirm the identity of a customer to concerned third parties, serving a similar purpose as a handwritten signature. Digital Signatures cannot be easily tampered with or imitated and are easily transportable, thereby making them a reliable method for verifying identity when implemented correctly. Digital Signatures are often used to implement Electronic Signatures, a broader term that refers to any Electronic Data that carries the intent of a signature.

Duplicate Detection and prevention is another way to reduce fraudulent activities. Financial institutions have software and operational controls in place to prevent duplication of the scanned electronic representations of customer checks.

Encryption The ACH Network automatically encrypts messages using 128-bit encryption and a secure sockets layer (SSL).

Public Key Cryptography is an Encryption/Decryption Security Method that uses one key to Encrypt a sent message and another to Decrypt it. With Electronic Check Conversion, the Private Key is a secret mathematical calculation used to create the digital signature on the Echeck, and the Public Key is the corresponding key given to anyone who needs to verify that the sender signed the echeck and that the electronic transfer has not been tampered with. Public Key Cryptography is another way to ensure authenticity of the Electronic Transfer of Funds.

What is the (ACH) Automated Clearing House Network?

The Automated Clearing House (ACH) Network is a funds distribution system that moves funds electronically from one entity to another. This highly reliable and efficient nationwide electronic network is governed by the rules established by the National Automated Clearing House Association (NACHA) and the Federal Reserve (Fed). The ACH payment system also handles debit card transactions; direct deposits of payroll, Social Security, and other government benefits; direct debit payments; and business-to-business payments.

How to get started with Echeck:

Useful advice to help make the implementation of electronic check conversion at your business run smoothly:

Choose a processing company that is well established in the market. While a competitive pricing package may also be of importance, having a processor that is reliable with a good reputation is essential.

Look for a processorthat enables you to easily align your current business processes with your new electronic processing system. Ensure that you can easily export customer data and smoothly integrate the electronic payment processing system with your business management software.

Notify your customers that your business will begin using electronic check conversion to process payments. Federal rules require you to post a notification about this change in practice as well as to give your customers a takeaway copy of the notification. You must also provide customers a telephone number to request more information about electronic check conversion.