In our second installment, we talked about NTC’s newest solution, NTC ePay. This third and final reason in this series we will go over how NTC keeps your cashflow going.

Due to the history of travel businesses, many travel agencies are given a travel merchant account with monthly credit card processing volume caps. This means merchants are only permitted to handle a specific number of credit card transactions or volume amount per month. Once that limit amount is reached, the merchant can no longer take credit cards for purchases that month. This keeps a business, especially an e-commerce merchant that relies on credit card payments, from operating effectively.

Imagine the impact on as a travel agent when you no longer have to worry about having your cash flow stopped. We work very hard to eliminate holds and reserves on all our travel merchant accountsaccounts.

Now imagine getting approved for large volume.

You will agree that those two factors will have a huge positive impact on your business growth.

Most merchant providers usually hold funds from travel agents, because historical data shows that consumers are much more likely to dispute and chargeback travel agency transactions because of a change in their travel plans.

You may be wondering, why do we not hold your funds?

Well simply said, because we understand your business. NTC has been doing business with travel professionals like you for over 20 years and we understand that holding funds creates a huge hassle for your operation. We understand that cash flow is essential to your continued success.

With NTC travel agents can feel confident that they will maintain cash flow to help their business operate smoothly and efficiently without interruptions.

Why do travel merchants flag large transactions?

Many times travel merchants run tens of thousands of dollars worth of transactions and their processor tells them they’re going to simply hold the funds and pay the merchant at a later date.

We understand how critical it is to have funds available because many agents have shared how with other merchant providers, their cash flow has come to a complete halt at times.

Remember that when you choose a travel payment processor, you must be sure to choose one with experience in working with travel agencies like NTC.

At NTC, we assist you in developing and implementing your fraud prevention procedures, so that you can be proactive in identifying and correcting potential weak spots in your processing cycle.

Over these past three blog articles, we have shared the three main reasons why travel agents like you prefer National Transaction Corporation. Now we want to hear from you as to which of these three reasons is most important for your travel agency business. We’d love to read your comments below.

To be responsive to the needs of our merchants and to meet that needs NTC offers next day funding. This is a value added service for customers and businesses that need to have their funds available quickly.

With more than 20 years of experience, National Transaction offers a variety of electronic payment services and technology for Retail and Ecommerce industries. From Travel, Medical Industry, Charitable Institution and Franchise.

Our services include:

Loans/Funding Program

Credit and Debit Card Processing

Currency Conversion

Electronic Checks

Electronic Invoicing

Gift and Loyalty Card Programs

Mobile and Online Solutions

Shopping Cart E-commerce Payment Gateway

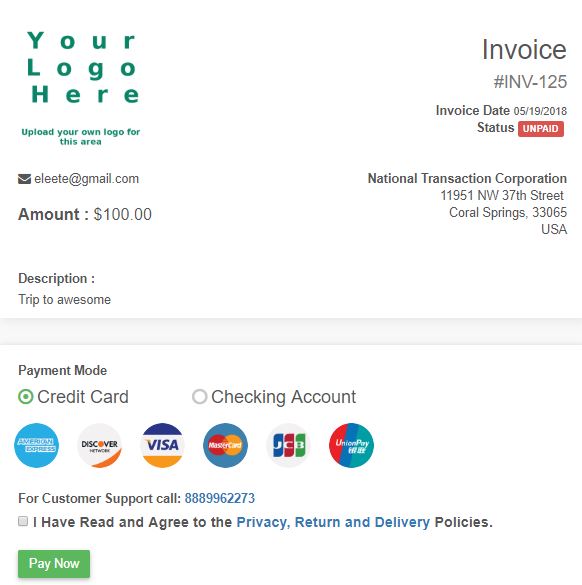

NTC e-Pay – is an Electronic Invoicing that made simple with NTC e-Pay! Free Setup, nothing to integrate; secure and fast.

Invoice customers Electronically with NTC e-Pay. Our e-Pay Platform can help Merchants bring new customers and encourage repeat business.

Our Virtual Merchant Gateway – accept payments your way! Online, In-Store and On the Go. A payment platform that flexes with your business.

NTC Business Loans – Fast, Affordable, and Simple Application Process.

MediPaid – a medical health insurance claims payment. Delivering paperless, next-day deposits for Health Insurance Payments.

NTC provides services to thousands of customers. NTC maintains a one on one relationships with all its merchants providing them with 24/7 customer service and technical support!

To know more about our product and services give us a call at 888-996-2273

Tokenization is a powerful security feature that allows a merchant to support all of their existing business processes that require card data without the risk of holding card data and without any security implications, because tokens are useless to criminals, they can be saved by the merchant as they do not represent any threat.

The liability and costs associated with PCI compliance is substantially reduced and the risk of storing sensitive data is eliminated.

Tokenization applies to credit card and gift card transactions.

Imagine a world where you could accept credit card payments without actually storing any sensitive cardholder data. No more worrying about data breaches, PCI compliance headaches, or the crippling costs of a security breach. That’s the power of tokenization.

Here’s how it works:

Instead of storing sensitive credit card information on your systems, each card number is replaced with a unique, randomly generated “token.” This token is useless to hackers, but it can be used to process payments securely on the merchant account that created the token.

Think of it like a valet ticket:

You hand over your car (the sensitive data) to the valet (the tokenization provider), who gives you a unique ticket (the token). The valet keeps your car safe, and you can use the ticket to retrieve it when needed.

The benefits are immense:

Ironclad Security: Reduce your PCI DSS scope and minimize the risk of costly data breaches. With tokenization, even if your system is compromised, the actual card data remains safe.

Effortless Compliance: Simplify PCI compliance and avoid hefty fines. Tokenization helps you meet the stringent security requirements for handling sensitive cardholder data.

Recurring Billing Made Easy: Securely store tokens for recurring billing or future transactions. This allows you to charge customers later without having to store their sensitive information.

Improved Customer Trust: Demonstrate your commitment to data security and build customer trust. Knowing their information is protected encourages repeat business and loyalty.

Streamlined Checkout: Offer a frictionless checkout experience with saved payment information. Tokenization enables faster and more convenient payments for your customers.

Tokenization is not just a security measure, it’s a strategic advantage:

Reduce costs: Minimize the expenses associated with data breaches and PCI compliance audits.

Boost efficiency: Streamline your payment processes and reduce administrative overhead.

Enhance your reputation: Position your business as a leader in data security and customer trust.

In conclusion:

Tokenization is a game-changer for businesses that accept credit cards. It offers unparalleled security, simplifies compliance, and unlocks new opportunities for growth. Embrace the future of secure payments with tokenization and watch your business thrive.

For Electronic Payments with Tokenization call now 888-996-2273 or click here NationalTransaction.Com

Visa 3-D Secure (3DS) is a security protocol designed to add an extra layer of protection to online credit card transactions.It aims to reduce fraud by verifying the cardholder’s identity before the transaction is authorized.Visa’s implementation of 3DS is called “Visa Secure.”

Here’s how it works:

Transaction Initiation: When a customer makes an online purchase with their Visa card, the merchant’s website communicates with the Visa network to initiate the 3DS process.

Risk Assessment: The issuer (the cardholder’s bank) performs a risk assessment based on various factors, such as the cardholder’s history, the transaction amount, and the merchant’s risk profile.

Authentication: If deemed necessary, the issuer challenges the cardholder to authenticate their identity. This usually involves a step-up authentication method, such as:

One-time password (OTP): Sent to the cardholder’s registered mobile phone or email.

Biometric authentication: Fingerprint scan or facial recognition.

Knowledge-based authentication: Security questions or personal information.

Verification: Once the cardholder successfully authenticates, the issuer confirms their identity to the merchant.

Transaction Completion: The merchant can then proceed to process the transaction with increased confidence that the cardholder is legitimate.

Integration and Implementation:

Merchants need to integrate 3DS into their online payment systems.This typically involves working with their payment gateway provider or acquiring bank to implement the necessary APIs and protocols.Visa provides detailed documentation and support for merchants to integrate Visa Secure.

Benefits and Features of 3DS:

Reduced Fraud: By verifying the cardholder’s identity, 3DS significantly reduces the risk of unauthorized transactions and chargebacks.

Improved Security: Adds an extra layer of security to online payments, protecting both merchants and customers from fraud.

Shift in Liability: In many cases, if a fraudulent transaction occurs after successful 3DS authentication, the liability shifts from the merchant to the issuer.This can save merchants significant costs associated with chargebacks and fraud disputes.

Increased Customer Confidence: Demonstrates a commitment to security and builds trust with customers, encouraging them to complete their purchases.

Enhanced User Experience: The latest version of 3DS (EMV 3DS 2.0) offers a smoother and more user-friendly authentication experience, minimizing friction during checkout.

Support for Mobile and Digital Wallets: 3DS is compatible with various payment channels, including mobile devices and digital wallets, providing a consistent and secure experience across all platforms.

In conclusion: Visa 3-D Secure is a powerful tool for merchants to enhance the security of their online transactions, reduce fraud, and improve customer confidence.

By implementing Visa Secure, merchants can protect themselves from financial losses and provide a safer and more trustworthy shopping experience for their customers.

For e-Commerce Electronic Payments set up with 3D Secure

Travel Agents prefer NTC ePay because they get paid faster with their very own “Buy Now” button or simply by requesting payments by email!

In our last installment, we shared how the security of NTC Payment Processing works for you. In this second part of our three-part series, we discuss the ways that the technology behind NTCePay helps your travel agency.

NTCePay offers travel agents the most innovative technology because it is fast, mobile friendly and easy to use.

Whether you use Quickbooks, Peachtree or any other accounting application, you can enter the invoice number into the ePay application for reconciliation, and you can customize your pricing to any amount you choose. Your agency can create invoice and payment links that can be posted to your website or any social media website for payment.

Things flow better when everything seems to work together, making your day a lot easier? Technology is something that can get your daily workflow to go smoothly, and NTC ePay works for you. If you need a customized solution to go with your workflow, NTC can make most anything a reality for your business workflow.

National Transaction Corporation is one of the few travel payment processing companies that can directly integrate with both TRAMS and SABRE. You can perform your bookings like you always have but have the payment flow the way you need it to. We also integrate with many booking engines and shopping carts allowing you many options that are not available by host agencies.

NTC ePay is simple, secure and sets up in just minutes. It’s a web application, so you can use it on any device you already own: your desktop, laptop, tablet or phone. It lets you add inventory items or use the quick send feature for simplified invoicing.

Our ePay product was designed from the ground up with your security in mind. Even though we encrypt data back and forth to the payment gateway, we also use the gateway to handle the cardholder’s input. NTC’s cutting-edge technology doesn’t store credit card data, nor does it transmit that data. What that means to you is that the liability is 100% on the bank and not your business, as is typically the case. The application is written and hosted on our own servers, so you can set up and be in the e-commerce business within minutes.

By the way, there are also many customizations available to you with NTC ePay which can be set up very easily by your users. Inquire with your specific process and we will meet your specific needs in the travel payment scope.

Now, when you run a social media campaign you can leverage our NTCePay technology to help you increase sales. Use our ePay links to post vacation travel packages or special sales and have customers pay in two clicks.

Next week we will share the third reason in this series why National Transaction Corporation is the preferred choice for travel agents like you.

Remember, when you need a safe and technologically advanced gateway to manage all your travel agency payments, look no further than NTC.

Feel free to call us now at 888-996-2273, if you are ready to start using NTC ePay today.

Exposure of personal information is a new challenge in todays environment, the initial exposure being a nightmare to unravel. A Javelin Strategy and Research study shows that a single data security breach can cost Billions of dollars in consumer fraud losses. Data security breaches rose 48% from 2011 in 2012 to 1,611 data breaches. Identity theft is on the rise too.

Walmart CEO Mike Duke Expecting $10 Billion in e-commerce payments 2013.

Commenting at a shareholder meeting WalMart CEO Mike Duke expected WalMarts online e-commerce site to bring in $10 Billion in transactions this year.

India Sees Spike in e-commerce and Mobile Payment Investments.

India is seeing deeper saturation of broadband rollouts connecting personal computers and laptops online at a faster pace. Big names such as Intel are keen on India’s development for market opportunities. Amazon and ebay just staked claims to India’s e-commerce playing field with deals to deliver their e-commerce services. Read more of this article »

When you are first setting up a retail or an eCommerce endeavor, few decisions will be of as much importance as the payment provider that you choose. Your payment provider will handle each and every card transaction your online company makes, and if it doesn’t function properly, or if it has a lot of hidden fees, such as old legacy systems with long term contracts, you can be setting your business up to fail before you ever get started.

So, we are going to explain to you what you should be looking for when you reach this crucial decision in the setup phase of your business, and we will help you find a payment provider that meets your needs perfectly and sets you up to succeed in the business world.

As a general rule of thumb, there are three main factors that you really need to consider when you go to choose who you will be working with: The people involved in the transaction, the fees associated with each transaction, and how the transaction is handled behind the scenes. There are some smaller tidbits that can make a specific provider a better or worse choice, but those three factors will allow you to narrow your search down to a select few of top competitors that will truly help your company succeed.

The Parties Involved

Besides your bank and the customer’s bank, there are three different factors that go into every single one of your transactions, and a payment provider works with all three of them. There’s you, your customer, and the technology acting as a bridge between the two of you. We’ll go into more detail about all that, now.

The Customer

With this part of the transaction, we are really talking about the “issuing bank”. That’s your customer’s bank, and they handle lending the customer the money to make a purchase on your site, and they issue the card that the customer uses to make that purchase. This is your customer’s main form of interaction with the transaction process, and it’s one of the most important factors since it’s what starts the transaction in the first place. However, you have no control over this factor, and you can simply ensure that the technology, which we’ll talk about soon, makes their part of the transaction as smooth as possible.

The Merchant

This is you and your part in the transaction. You function as the merchant that the customer is engaging with, and in order to do that, you need a merchant bank to partner with and work as your company’s bank. A merchant bank functions differently than the bank you use in your day to day life. Instead of issuing you funds in advance for credit purchases and managing your checking and savings accounts, a merchant bank takes in your customers’ payments for you, and then puts those payments into a special merchant account that is a lot like a business’s checking account. Without a merchant bank, you won’t be able to succeed in the long-term with eCommerce.

The Technology Solution

Your technology, and the company handling it, is what makes a transaction possible in the first place, and there are two parts to this imperative factor: The payment processor and the payment gateway.

Processor

The payment processor is what actually handles the transaction. It moves the money between the different parties and delivers it to the banks and accounts involved. If your processor is subpar, your customer’s transaction experience will be, too. You need an up-to-date payment processor that functions smoothly and without any hassle placed on you or your customer to ensure that each customer enjoys a seamless transaction.

Gateway

The payment gateway is essentially what sends the transaction information to the payment processor. It links to your site’s shopping cart feature, and when a customer buys something, it connects to the payment processor and begins the transaction. In order to ensure that your transactions are smooth and effortless, this technological asset needs to be competent and able to easily satisfy your customers without being apparent.

How the Transaction Process Happens

The transaction process is fairly complicated, but it all takes place in a matter of seconds. In fact, it’s usually seemingly instantaneous.

Once a purchase is made, the payment gateway encrypts the transaction data to protect your customer and your business, and then it asks the customer’s bank if it will advance the funds for the customer’s purchase. If yes, the payment will be sent to your merchant account, and if not, the transaction will be denied and ended until a resolution can be found.

Once that step is completed, the funds typically end up being accessible by you the second your merchant bank acquires them and places them in your account, but you may be forced to keep a certain amount in the account to make sure you can cover any returns that pop up.

This part is not instantaneous. It can take a couple days to complete this part of the process.

Transaction Fees

This is easily the factor that you’ll want to pay attention to the most, because a lot of merchant service providers are downright misleading when they quote your rates, and you need to get a firm understanding of how a company sets up its fees to know what to actually expect from your bill.

Most often, companies will quote something like 1.8% rates to interest you and appeal to your more frugal side, but then they’ll apply all sorts of hidden fees that raise that rate as high as 11% without notifying you properly. As you can imagine, that can make your bill a bit more than what you thought it would be.

There are three rate models that are most often used:

Flat-Rate

You’re given a specific amount to pay, and whether that covers your total fees or not, that’s what you pay. You could be overpaying tremendously if you accept a quite a few low cost cards vs. the higher cost cards. The processor is banking on your acceptance of these lower cards to ensure all costs are covered.

Interchange Plus Pricing

This takes the interchange fee you pay and adds a small fixed rate on top of it. It’s not as consistent as a flat-rate fee because of the sheer amount of interchange fees out there and the number of different credit cards with all of the various reward and incentive programs.

Tiered Pricing

This is when the provider creates a few tiers of fees and charges you based on the tier your fees are in rather than each individual fee. The only bad thing about this is that the provider decides which fees go into which tier.

Other Important Things to Consider

Does your processor provide Data Security/PCI protection? What about financial breach protection, in the event you are breached?

Any business or other entity that stores, processes or transmits cardholder data must ensure that their processes meet the Payment Card Industry / Data Security Standard (PCI/DSS). Failure to do so can result in heavy fines being levied.

Understanding PCI/DSS

The PCI/DSS is a global standard defining acceptable practice for any entity involved in the storage, transmission or processing of cardholder data.

In recognition of the sensitive, confidential and valuable nature of this data the standard imposes strict regulations which must be met in full. The full requirements are detailed but are covered by 12 broad requirements. These are grouped into 6 broad control objectives as follows:

1. Build and Maintain a Secure Network and Systems – Install and maintain a firewall configuration to protect data – Do not use vendor-supplied defaults for system passwords and other security parameters

2. Protect Cardholder Data – Protect stored data (use encryption) – Encrypt transmission of cardholder data and sensitive information across public networks

3. Maintain a Vulnerability Management Program – Use and regularly update anti-virus software – Develop and maintain secure systems and applications

4. Implement Strong Access Control Measures -Restrict access to data by business need-to-know -Assign a unique ID to each person with computer access -Restrict physical access to cardholder data

5. Regularly Monitor and Test Networks -Track and monitor all access to network resources and cardholder data -Regularly test security systems and processes

6. Maintain an Information Security Policy -Maintain a policy that addresses Information Security

Any entity handling card transactions must meet the standard and be able to demonstrate (certify) that it does so. The level of certification is flexible and depends on how transactions are processed and in what volume.

A Summary of Benefits

Achieving full compliance with PCI/DSS standards is more than an obligation. It delivers genuine benefits to businesses:

– Lessen the risk of fraudulent transactions

– Prevent security breaches

-Lessen the impact should a breach occur

– Reduce your business’ exposure to risk and liability

– Provide peace of mind for your customers

– Avoid the negative PR associated with data loss

Why are These Requirements in Place?

Card transactions have grown enormously in recent years as cards become the number 1 preferred form of payment. Since no physical money is handled or exchanged as part of these transactions they are dependent on the transfer of data.

That data therefore becomes sensitive and valuable and must be protected. Failure to protect this data can lead to fraud and theft. These crimes often impact both the card holder and the merchant directly. They can also damage or even destroy the reputation of businesses or organizations involved in hacks or data breaches.

More widely card fraud has the long-term detrimental effect of eroding consumer confidence and trust – both in the individual companies affected and in the card payment industry more widely.

Millions of consumers and organizations worldwide are choosing to pay by card. And millions of businesses, professionals, traders and organizations are accepting and handling these payments. Instead of allowing an ad-hoc approach where each business sets its own level of security the PCI / DSS was imposed. This ensures a uniformly high level of data security throughout the worldwide card payment industry.

Keep your Data Secure – Don’t get caught without PCI Data Breach Protection

With more retailers than ever before embracing e-commerce, the fraud journey is becoming a focus for many. It is clear, though, why retailers have paid more attention to the customer journey. After all, in addition to shaping a customer’s overall experience, a customer’s journey determines whether or not they will make a repeat purchase. Too often, however, when focusing solely on the customer journey, the fraudster’s journey remains overlooked. To bring the fraud journey into focus, we need to understand what it really is and where retailers should be placing their efforts.

Like the customer journey, the fraud journey is the path fraudsters take when interacting with a brand. In the case of the fraud journey, we consider the actions a fraudster takes to commit fraud. Understanding the fraud journey and focusing on the fraudster’s actions will enable online retailers to dramatically reduce fraud conversion rates and ultimately prevent fraud.

It’s not by chance that the customer’s journey and the fraudster’s journey are often mentioned together. In their attempt to satisfy customers while also detecting and preventing fraud, many retailers are faced with an impossible juggling act: Do I prevent fraud or give my customers the experience they want? True, balancing between the two, enabling the paths to co-exist, is challenging, yet it can be achieved. Taking the time to understand the intricacies of the fraud journey can help reduce false positives and cut down on chargebacks.

The True Cost of Chargebacks

Chargebacks. The very word sends shivers down the spine of even the most experienced online retail fraud fighters—with good reason. Chargebacks end up costing retailers in additional fees as well as in customer dissatisfaction and it’s nearly impossible to truly evaluate the cost of chargebacks.

It’s estimated that for every $100 in chargebacks, retailers end up paying $240! But the problem with chargebacks goes far beyond any fees or penalties incurred. The issue with chargebacks is that if a customer gets to the point where they have to request a chargeback, the damage has already been done.

Why Does the Fraud Journey Matter?

Let’s consider the forecast that e-commerce is expected to make up 22 percent of all global retail sales by 2023. Or that it’s predicted that U.S. e-commerce sales will jump 18 percent due to Covid-19. E-commerce sales are at an all-time high, and there are no signs this trend is going to slow down anytime soon. This emphasizes even more the need to focus on the fraud journey. The fraud journey has an impact when building an effective chargeback management strategy and it is directly linked to customer retention and acquisition.

The fraud journey gives one an in-depth understanding of users who could be fraudsters, based on suspicious behavior. Retailers looking to up their fraud prevention and chargeback management game, need to have a clear understanding of the fraud journey. This understanding will make it easy for them to differentiate actions a legitimate user would take, from fraudulent actions. For example, a change of the shipping address upon login indicates a possible fraudulent action. Carefully considering the behavior of a legitimate customer at every stage of the customer journey can help isolate suspicious activities with more accuracy, and thus cut down on false positives.

Fraud Prevention: The Ultimate Juggling Act

Understanding chargebacks and how to prevent them, starts with understanding how retailers approach fraud prevention. In cases where retailers focus on detection and prevention at the payment stage, or even only one part of the payment stage, fraudsters are able to successfully move through their journey undetected until it is too late.

If a fraudster’s activity is detected as suspicious and flagged only at the payment stage, gives an opportunistic fraudster plenty of opportunities to monetize the service by other means before their presence is detected. This could include everything from promo abuse and referral abuse to new account fraud.

That’s exactly why a more advanced fraud prevention and detection approach is required. For example, using technologies such as behavioral biometrics will enable retailers to stop a fraudster long before the payment stage, before any real damage is done, and will help cut down on chargebacks.

Is it really that simple? Retailers are rightfully concerned with the need to ensure that detection of fraud early in the fraud journey, early enough to prevent damage including chargebacks, will introduce as little friction as possible into the customer’s journey. At times it seems retailers can’t win. If they flag an activity as suspicious based on strict rules, they might find themselves with a rise in false positives and possibly disappointed legitimate customers. Other times retailers rely on fraud detection and prevention at the payment stage, ignoring any fraudulent activity, which happens before that, throughout the customer journey. Either way, with fraudulent activities getting more sophisticated, retailers are dealing with a growing number of chargebacks due to fraud.

In-depth understanding of the fraud journey, identifying and monitoring its various touchpoints, will help retailers to reduce fraud and still maintain the balance between customer satisfaction and security.

Proactive Chargeback Management

The common passive-reactive approach to chargeback management is proving to be insufficient as fraudsters are increasingly using tools such as bots and emulators to scale their attacks. Behavioral biometrics-based fraud detection introduces a proactive approach to counter advanced fraud. As opposed to focusing on login or checkout only, and reacting too late, behavioral biometrics focuses on user behavior throughout the entire customer journey, making it easy to identify suspicious and potentially fraudulent behavior at its earliest stage, enabling to stop the fraudster in his tracks, before damage is done.

Adopting advanced technologies like behavioral biometrics will provide retailers with visibility and insight into the entire fraud journey, leading to better, data-driven decision making, pre-transaction prevention and cut down chargebacks.

SecuredTouch is the expert in adaptive fraud detection solutions for online retailers and financial institutions. Using machine learning, the technology continuously analyzes hundreds of behavioral data points to differentiate between human and non-human behaviors, human to device interactions and behavioral anomalies to provide early detection of fraud. The solution identifies sophisticated fraud throughout the customer journey while simultaneously improving the user experience. Businesses benefit from reduced drain on internal resources and increased transaction rates, ultimately leading to an improved bottom line. Today, our award-winning solutions are used by some of the world’s largest retailers and financial institutions.

By Ran Wasserman, CTO, SecuredTouch – Sponsored Content

The chargeback process was introduced more than four decades ago as a consumer-protection mechanism. It was meant to inspire consumer confidence in payment cards, which were still a novel concept at the time. Fast-forward to today, though, and these forced payment reversals have evolved into a significant problem for online merchants.

Chargeback abuse—commonly known as friendly fraud—is a major source of loss. In fact, chargeback issuances resulting from friendly fraud were expected to reach $50 billion annually in 2020, according to Mercator Advisory Group.

Even then, this figure is a low estimate. It doesn’t account for current trends in a post-Covid environment, where we’ve seen a dramatic increase in friendly fraud. These attacks were already up by the end of March, and there’s no sign that they’re going to slow down.

Covid-19 might look like the source of the problem on a superficial level. If we dig deeper, though, we see four underlying factors behind the preexisting upward trend in chargeback filings:

More fraudsters view the CNP environment as the “channel of least resistance;”

Inconsistency in technologies and regulations across different markets;

The rise of mobile banking;

The response by card networks like Visa and Mastercard.

These four factors carry diverse ramifications for the market. For instance, roughly $118 billion in e-commerce transactions are declined each year, according to Javelin Strategy & Research. Most of these rejected purchases are false positives, meaning the merchant unnecessarily rejected the purchase in hopes of avoiding a chargeback.

Clearly, there’s a growing disconnect between merchants, financial institutions, and card networks regarding how best to address this situation. We can see this reflected in the fact that the rate of chargeback issuances in North America is expected to significantly outpace those in the European market. This is attributed to factors like strong customer authentication protocols required by the Revised Payment Services Directive (PSD2), and more widespread use of 3-D Secure technology.

The pressure is on for industry players to find more comprehensive solutions for chargebacks. These solutions must be data-driven and adaptable, though. Otherwise, the growing disconnect between cardholders, merchants, financial institutions, and card networks will exacerbate existing problems in the market, leading to further losses.

The good news is that, in the meantime, there are strategies merchants can employ to address these concerns. For instance, even though friendly fraud operates by concealing itself behind false chargeback reason codes, it’s still helpful to have a clear understanding of what each reason code means in context.

Merchants can’t avoid friendly fraud in the same way they can detect criminal attacks or eliminate merchant errors. However, they can minimize friendly fraud risk by adopting key best practices, including:

Notifying customers to remind them about recurring payments;

Keeping organized and well-documented transaction records;

Using delivery confirmation when shipping physical goods;

Providing easy access to round-the-clock, live customer service;

Providing a quick response to any refund or cancellation requests.

Also, if a merchant identifies a chargeback as friendly fraud, it’s important to engage that dispute through the representment process. This is a complex, time-consuming process, which is why many merchants opt to outsource their chargeback management. It’s still possible to conduct the process with in-house management. However, it will require strong evidence to support the merchant’s case, such as:

A legible sales receipt

A tracking number

Any emails or transcripts of communications you’ve had with the customer

Delivery confirmation information

A record of in-store pickup

Photographic evidence (when available)

This evidence needs to be contextualized with a chargeback rebuttal letter, explaining why the original transaction was valid. Also, merchants are on a tight schedule. In most cases, they have only a few days to provide a response to their acquirer.

Chargeback management can be a difficult and confusing process. But, with the problem of chargeback abuse only set to grow over time, it’s something merchants can’t afford to take for granted.

—Monica Eaton Cardone is the chief operating office and cofounder of Chargebacks911, Clearwater, Fla.

There are few moments like now where American consumers are collectively open to the idea of new payment methods – especially contactless ones such as mobile wallets. This is good news for businesses since mobile wallets offer a safer payment alternative to credit cards and drastically reduce customer wait times at checkout.

Mobile wallets (such as Apple Pay and PayPal) use authentication, monitoring and data encryption to secure and transmit personal information, and the level of security associated with them has payment card issuers backing their use. This is certainly helping drive consumer adoption, as does convenience.

In fact, global mobile wallet transaction value is estimated to reach nearly $14 trillion by 20201 – and that is a pre-COVID-19 estimate. New estimates are higher and point to further rapid adoption given the current need for touch-free payment options. According to a recently published Visa Back to Business report,* 70 percent of consumers surveyed in June 2020 have used a new shopping or payment method for the first time this year.

A rapid shift has begun and the numbers tell the storySo what is holding back business adoption of mobile wallets? Until recently, it just wasn’t a priority for many small- and medium-size businesses to enable it or educate their employees on its use. The lack of preferential demand didn’t make it a pressing topic. But that is changing. Consider this:

According to Forbes,2 by 2026, digital natives will be 59 percent of the consumers in the U.S. market.

Of this, 45 percent will be specifically Millennials and Gen Z, representing the largest purchasing power.

As Gen Z move into becoming the largest generation cohort, their purchasing power will be $143 billion.

But it’s not just what lies ahead that SMBs should be focused on now.

According to Visa’s Back to Business report, shoppers are now putting COVID-19 safety measures at the top of their shopping lists and they will reward stores that do the same. In fact, if all other factors were equal (price, selection, location), nearly 63 percent of consumers surveyed would switch to a new store that installed contactless payment options, such as mobile wallets.3

What does this mean for you? Now is the time to connect with customers to make sure they are fully contactless capable and have the technology in place to accept many of the most popular mobile wallets.

1Payments Industry Intelligence, “The rise of digital and mobile wallet: Global usage statistics from 2018,” November 25, 2018. 2Forbes, January 2020 3Visa Back to Business report 2020