To be responsive to the needs of our merchants and to meet that needs NTC offers next day funding. This is a value added service for customers and businesses that need to have their funds available quickly.

With more than 20 years of experience, National Transaction offers a variety of electronic payment services and technology for Retail and Ecommerce industries. From Travel, Medical Industry, Charitable Institution and Franchise.

Our services include:

Loans/Funding Program

Credit and Debit Card Processing

Currency Conversion

Electronic Checks

Electronic Invoicing

Gift and Loyalty Card Programs

Mobile and Online Solutions

Shopping Cart E-commerce Payment Gateway

NTC e-Pay – is an Electronic Invoicing that made simple with NTC e-Pay! Free Setup, nothing to integrate; secure and fast.

Invoice customers Electronically with NTC e-Pay. Our e-Pay Platform can help Merchants bring new customers and encourage repeat business.

Our Virtual Merchant Gateway – accept payments your way! Online, In-Store and On the Go. A payment platform that flexes with your business.

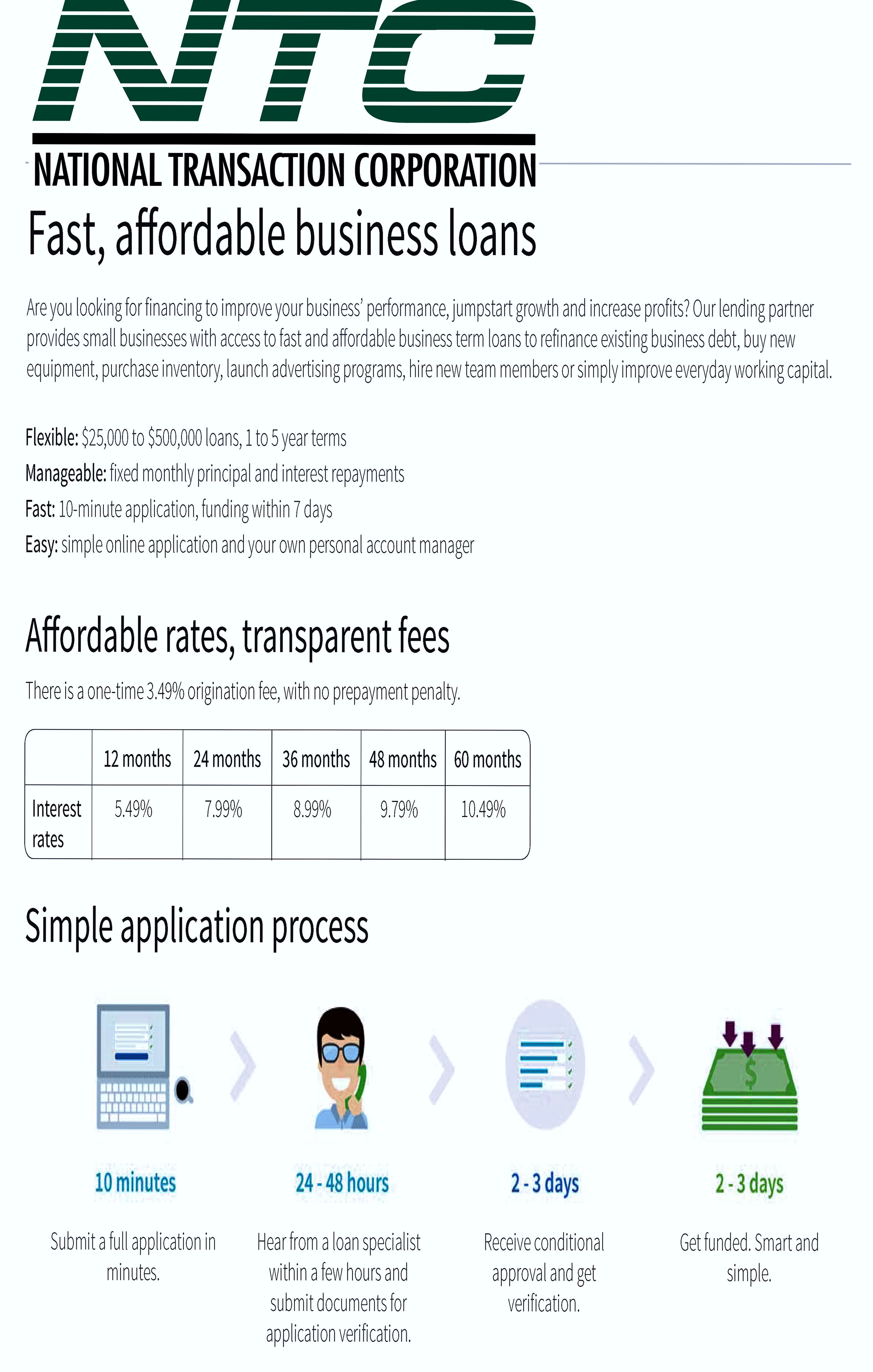

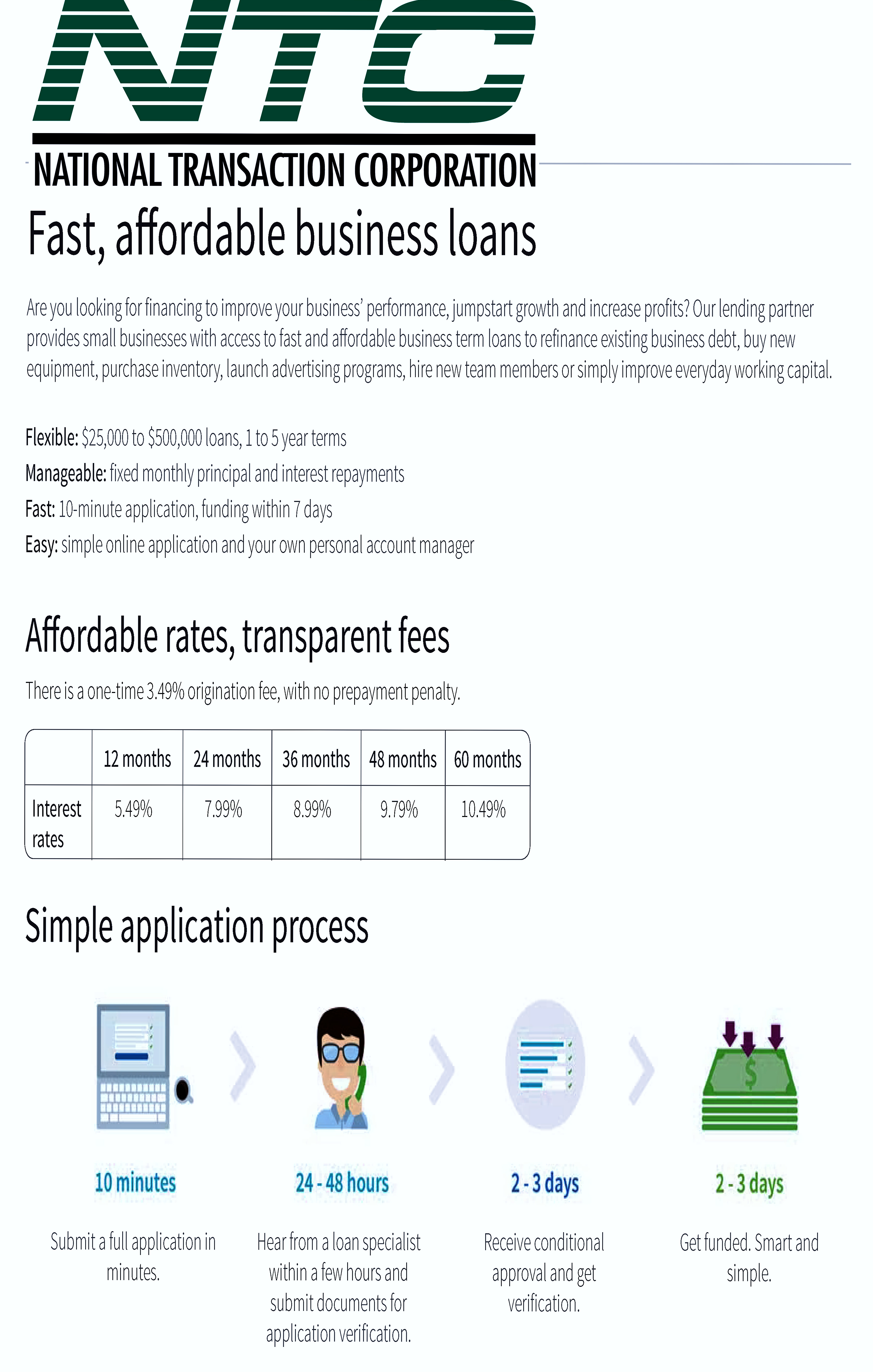

NTC Business Loans – Fast, Affordable, and Simple Application Process.

MediPaid – a medical health insurance claims payment. Delivering paperless, next-day deposits for Health Insurance Payments.

NTC provides services to thousands of customers. NTC maintains a one on one relationships with all its merchants providing them with 24/7 customer service and technical support!

To know more about our product and services give us a call at 888-996-2273

John Stewart January 17, 2022 https://www.digitaltransactions.net/trends-like-open-banking-and-bnpl-will-sustain-e-commerces-hot-streak-a-report-says/

Open banking, single-click checkout wallets, and the hot buy now, pay later trend will all help drive e-commerce volume worldwide in the coming five years, predicts Juniper Research in a report released Monday. This momentum is likely to push online sales long after the short-term impetus from the pandemic subsides, Juniper says.

E-commerce volume totaled $4.9 trillion globally in 2021, a figure the United Kingdom-based research firm forecasts will reach $7.5 trillion in 2026, when China will control a 37% share. Wider availability of multiple e-commerce channels, including mobile devices, will propel the overall growth worldwide, Juniper says. But along with the boom in e-commerce will come a corresponding growth in fraud via identity theft, account takeovers, and fraudulent chargebacks, the report warns. China, for example, will account for more than 40% of fraud losses worldwide in 2025, at more than $12 billion, Juniper forecasts.

Open banking is a trend by which fintechs can verify balances in consumers’ accounts and transfer funds to pay for online purchases. As standards bodies work to promulgate standards for this business, e-commerce payment providers “should … partner with specialists in … specific emerging payment areas to keep pace with changing merchant expectations around acceptance types,” the research firm says in its release, referring to digital wallets and crypto as well as open banking.

Open banking has taken on a higher profile in the global payments market with efforts by both of the global card networks to acquire firms that specialize in this area. Visa Inc. has acquired Tink AB, while Mastercard Inc. bought Aiia and Finicity Corp.

Physical goods will continue to dominate e-commerce spending, the report says, accounting for 82% of payment value by 2026. To tap into the trend, Juniper advises, payments providers should support buy now, pay later plans, which allow consumers to split purchases into four equal installments paid over a six-week period at no interest. BNPL is becoming more controversial, however, as the Consumer Financial Protection Bureau has launched an investigation of the option and as reports emerge that consumers with multiple accounts are more likely to miss a payment.

While still a big trend, e-commerce sales in the U.S. market cooled significantly last year as the pandemic effect lost some of its force. Third-quarter sales in 2021 reached $214.6 billion, up 6.6% year-over-year, according to the Census Bureau, which tracks retail sales. That follows an 8.9% rise in the second quarter and three straight quarters with increases of 32% or more. Fourth-quarter 2021 results are not yet available.

When you are first setting up a retail or an eCommerce endeavor, few decisions will be of as much importance as the payment provider that you choose. Your payment provider will handle each and every card transaction your online company makes, and if it doesn’t function properly, or if it has a lot of hidden fees, such as old legacy systems with long term contracts, you can be setting your business up to fail before you ever get started.

So, we are going to explain to you what you should be looking for when you reach this crucial decision in the setup phase of your business, and we will help you find a payment provider that meets your needs perfectly and sets you up to succeed in the business world.

As a general rule of thumb, there are three main factors that you really need to consider when you go to choose who you will be working with: The people involved in the transaction, the fees associated with each transaction, and how the transaction is handled behind the scenes. There are some smaller tidbits that can make a specific provider a better or worse choice, but those three factors will allow you to narrow your search down to a select few of top competitors that will truly help your company succeed.

The Parties Involved

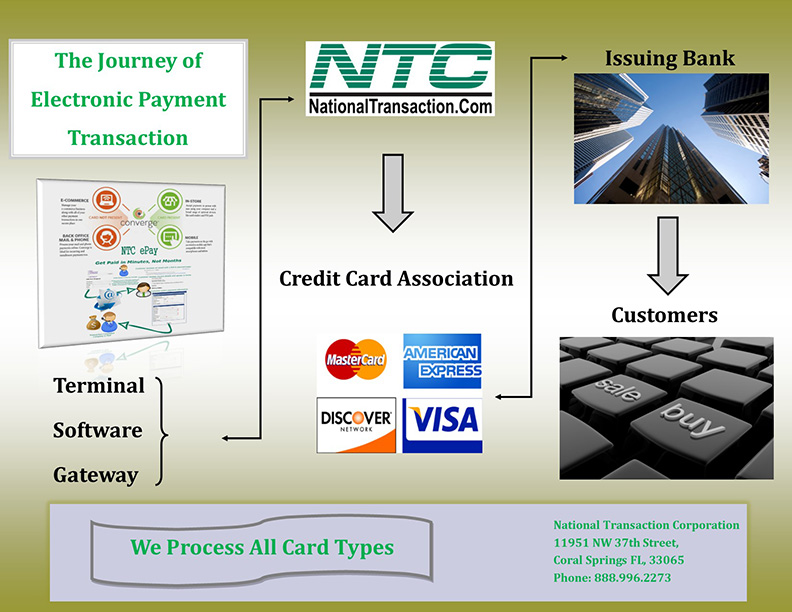

Besides your bank and the customer’s bank, there are three different factors that go into every single one of your transactions, and a payment provider works with all three of them. There’s you, your customer, and the technology acting as a bridge between the two of you. We’ll go into more detail about all that, now.

The Customer

With this part of the transaction, we are really talking about the “issuing bank”. That’s your customer’s bank, and they handle lending the customer the money to make a purchase on your site, and they issue the card that the customer uses to make that purchase. This is your customer’s main form of interaction with the transaction process, and it’s one of the most important factors since it’s what starts the transaction in the first place. However, you have no control over this factor, and you can simply ensure that the technology, which we’ll talk about soon, makes their part of the transaction as smooth as possible.

The Merchant

This is you and your part in the transaction. You function as the merchant that the customer is engaging with, and in order to do that, you need a merchant bank to partner with and work as your company’s bank. A merchant bank functions differently than the bank you use in your day to day life. Instead of issuing you funds in advance for credit purchases and managing your checking and savings accounts, a merchant bank takes in your customers’ payments for you, and then puts those payments into a special merchant account that is a lot like a business’s checking account. Without a merchant bank, you won’t be able to succeed in the long-term with eCommerce.

The Technology Solution

Your technology, and the company handling it, is what makes a transaction possible in the first place, and there are two parts to this imperative factor: The payment processor and the payment gateway.

Processor

The payment processor is what actually handles the transaction. It moves the money between the different parties and delivers it to the banks and accounts involved. If your processor is subpar, your customer’s transaction experience will be, too. You need an up-to-date payment processor that functions smoothly and without any hassle placed on you or your customer to ensure that each customer enjoys a seamless transaction.

Gateway

The payment gateway is essentially what sends the transaction information to the payment processor. It links to your site’s shopping cart feature, and when a customer buys something, it connects to the payment processor and begins the transaction. In order to ensure that your transactions are smooth and effortless, this technological asset needs to be competent and able to easily satisfy your customers without being apparent.

How the Transaction Process Happens

The transaction process is fairly complicated, but it all takes place in a matter of seconds. In fact, it’s usually seemingly instantaneous.

Once a purchase is made, the payment gateway encrypts the transaction data to protect your customer and your business, and then it asks the customer’s bank if it will advance the funds for the customer’s purchase. If yes, the payment will be sent to your merchant account, and if not, the transaction will be denied and ended until a resolution can be found.

Once that step is completed, the funds typically end up being accessible by you the second your merchant bank acquires them and places them in your account, but you may be forced to keep a certain amount in the account to make sure you can cover any returns that pop up.

This part is not instantaneous. It can take a couple days to complete this part of the process.

Transaction Fees

This is easily the factor that you’ll want to pay attention to the most, because a lot of merchant service providers are downright misleading when they quote your rates, and you need to get a firm understanding of how a company sets up its fees to know what to actually expect from your bill.

Most often, companies will quote something like 1.8% rates to interest you and appeal to your more frugal side, but then they’ll apply all sorts of hidden fees that raise that rate as high as 11% without notifying you properly. As you can imagine, that can make your bill a bit more than what you thought it would be.

There are three rate models that are most often used:

Flat-Rate

You’re given a specific amount to pay, and whether that covers your total fees or not, that’s what you pay. You could be overpaying tremendously if you accept a quite a few low cost cards vs. the higher cost cards. The processor is banking on your acceptance of these lower cards to ensure all costs are covered.

Interchange Plus Pricing

This takes the interchange fee you pay and adds a small fixed rate on top of it. It’s not as consistent as a flat-rate fee because of the sheer amount of interchange fees out there and the number of different credit cards with all of the various reward and incentive programs.

Tiered Pricing

This is when the provider creates a few tiers of fees and charges you based on the tier your fees are in rather than each individual fee. The only bad thing about this is that the provider decides which fees go into which tier.

Other Important Things to Consider

Does your processor provide Data Security/PCI protection? What about financial breach protection, in the event you are breached?

Any business or other entity that stores, processes or transmits cardholder data must ensure that their processes meet the Payment Card Industry / Data Security Standard (PCI/DSS). Failure to do so can result in heavy fines being levied.

Understanding PCI/DSS

The PCI/DSS is a global standard defining acceptable practice for any entity involved in the storage, transmission or processing of cardholder data.

In recognition of the sensitive, confidential and valuable nature of this data the standard imposes strict regulations which must be met in full. The full requirements are detailed but are covered by 12 broad requirements. These are grouped into 6 broad control objectives as follows:

1. Build and Maintain a Secure Network and Systems – Install and maintain a firewall configuration to protect data – Do not use vendor-supplied defaults for system passwords and other security parameters

2. Protect Cardholder Data – Protect stored data (use encryption) – Encrypt transmission of cardholder data and sensitive information across public networks

3. Maintain a Vulnerability Management Program – Use and regularly update anti-virus software – Develop and maintain secure systems and applications

4. Implement Strong Access Control Measures -Restrict access to data by business need-to-know -Assign a unique ID to each person with computer access -Restrict physical access to cardholder data

5. Regularly Monitor and Test Networks -Track and monitor all access to network resources and cardholder data -Regularly test security systems and processes

6. Maintain an Information Security Policy -Maintain a policy that addresses Information Security

Any entity handling card transactions must meet the standard and be able to demonstrate (certify) that it does so. The level of certification is flexible and depends on how transactions are processed and in what volume.

A Summary of Benefits

Achieving full compliance with PCI/DSS standards is more than an obligation. It delivers genuine benefits to businesses:

– Lessen the risk of fraudulent transactions

– Prevent security breaches

-Lessen the impact should a breach occur

– Reduce your business’ exposure to risk and liability

– Provide peace of mind for your customers

– Avoid the negative PR associated with data loss

Why are These Requirements in Place?

Card transactions have grown enormously in recent years as cards become the number 1 preferred form of payment. Since no physical money is handled or exchanged as part of these transactions they are dependent on the transfer of data.

That data therefore becomes sensitive and valuable and must be protected. Failure to protect this data can lead to fraud and theft. These crimes often impact both the card holder and the merchant directly. They can also damage or even destroy the reputation of businesses or organizations involved in hacks or data breaches.

More widely card fraud has the long-term detrimental effect of eroding consumer confidence and trust – both in the individual companies affected and in the card payment industry more widely.

Millions of consumers and organizations worldwide are choosing to pay by card. And millions of businesses, professionals, traders and organizations are accepting and handling these payments. Instead of allowing an ad-hoc approach where each business sets its own level of security the PCI / DSS was imposed. This ensures a uniformly high level of data security throughout the worldwide card payment industry.

Keep your Data Secure – Don’t get caught without PCI Data Breach Protection

With more retailers than ever before embracing e-commerce, the fraud journey is becoming a focus for many. It is clear, though, why retailers have paid more attention to the customer journey. After all, in addition to shaping a customer’s overall experience, a customer’s journey determines whether or not they will make a repeat purchase. Too often, however, when focusing solely on the customer journey, the fraudster’s journey remains overlooked. To bring the fraud journey into focus, we need to understand what it really is and where retailers should be placing their efforts.

Like the customer journey, the fraud journey is the path fraudsters take when interacting with a brand. In the case of the fraud journey, we consider the actions a fraudster takes to commit fraud. Understanding the fraud journey and focusing on the fraudster’s actions will enable online retailers to dramatically reduce fraud conversion rates and ultimately prevent fraud.

It’s not by chance that the customer’s journey and the fraudster’s journey are often mentioned together. In their attempt to satisfy customers while also detecting and preventing fraud, many retailers are faced with an impossible juggling act: Do I prevent fraud or give my customers the experience they want? True, balancing between the two, enabling the paths to co-exist, is challenging, yet it can be achieved. Taking the time to understand the intricacies of the fraud journey can help reduce false positives and cut down on chargebacks.

The True Cost of Chargebacks

Chargebacks. The very word sends shivers down the spine of even the most experienced online retail fraud fighters—with good reason. Chargebacks end up costing retailers in additional fees as well as in customer dissatisfaction and it’s nearly impossible to truly evaluate the cost of chargebacks.

It’s estimated that for every $100 in chargebacks, retailers end up paying $240! But the problem with chargebacks goes far beyond any fees or penalties incurred. The issue with chargebacks is that if a customer gets to the point where they have to request a chargeback, the damage has already been done.

Why Does the Fraud Journey Matter?

Let’s consider the forecast that e-commerce is expected to make up 22 percent of all global retail sales by 2023. Or that it’s predicted that U.S. e-commerce sales will jump 18 percent due to Covid-19. E-commerce sales are at an all-time high, and there are no signs this trend is going to slow down anytime soon. This emphasizes even more the need to focus on the fraud journey. The fraud journey has an impact when building an effective chargeback management strategy and it is directly linked to customer retention and acquisition.

The fraud journey gives one an in-depth understanding of users who could be fraudsters, based on suspicious behavior. Retailers looking to up their fraud prevention and chargeback management game, need to have a clear understanding of the fraud journey. This understanding will make it easy for them to differentiate actions a legitimate user would take, from fraudulent actions. For example, a change of the shipping address upon login indicates a possible fraudulent action. Carefully considering the behavior of a legitimate customer at every stage of the customer journey can help isolate suspicious activities with more accuracy, and thus cut down on false positives.

Fraud Prevention: The Ultimate Juggling Act

Understanding chargebacks and how to prevent them, starts with understanding how retailers approach fraud prevention. In cases where retailers focus on detection and prevention at the payment stage, or even only one part of the payment stage, fraudsters are able to successfully move through their journey undetected until it is too late.

If a fraudster’s activity is detected as suspicious and flagged only at the payment stage, gives an opportunistic fraudster plenty of opportunities to monetize the service by other means before their presence is detected. This could include everything from promo abuse and referral abuse to new account fraud.

That’s exactly why a more advanced fraud prevention and detection approach is required. For example, using technologies such as behavioral biometrics will enable retailers to stop a fraudster long before the payment stage, before any real damage is done, and will help cut down on chargebacks.

Is it really that simple? Retailers are rightfully concerned with the need to ensure that detection of fraud early in the fraud journey, early enough to prevent damage including chargebacks, will introduce as little friction as possible into the customer’s journey. At times it seems retailers can’t win. If they flag an activity as suspicious based on strict rules, they might find themselves with a rise in false positives and possibly disappointed legitimate customers. Other times retailers rely on fraud detection and prevention at the payment stage, ignoring any fraudulent activity, which happens before that, throughout the customer journey. Either way, with fraudulent activities getting more sophisticated, retailers are dealing with a growing number of chargebacks due to fraud.

In-depth understanding of the fraud journey, identifying and monitoring its various touchpoints, will help retailers to reduce fraud and still maintain the balance between customer satisfaction and security.

Proactive Chargeback Management

The common passive-reactive approach to chargeback management is proving to be insufficient as fraudsters are increasingly using tools such as bots and emulators to scale their attacks. Behavioral biometrics-based fraud detection introduces a proactive approach to counter advanced fraud. As opposed to focusing on login or checkout only, and reacting too late, behavioral biometrics focuses on user behavior throughout the entire customer journey, making it easy to identify suspicious and potentially fraudulent behavior at its earliest stage, enabling to stop the fraudster in his tracks, before damage is done.

Adopting advanced technologies like behavioral biometrics will provide retailers with visibility and insight into the entire fraud journey, leading to better, data-driven decision making, pre-transaction prevention and cut down chargebacks.

SecuredTouch is the expert in adaptive fraud detection solutions for online retailers and financial institutions. Using machine learning, the technology continuously analyzes hundreds of behavioral data points to differentiate between human and non-human behaviors, human to device interactions and behavioral anomalies to provide early detection of fraud. The solution identifies sophisticated fraud throughout the customer journey while simultaneously improving the user experience. Businesses benefit from reduced drain on internal resources and increased transaction rates, ultimately leading to an improved bottom line. Today, our award-winning solutions are used by some of the world’s largest retailers and financial institutions.

By Ran Wasserman, CTO, SecuredTouch – Sponsored Content

Merchant accounts are not depository accounts like checking and savings accounts; they are considered a line of credit. Therefore, when a customer pays with a credit card; a bank is extending credit to that customer and also making the payment on his/her behalf. As for processors or payment providers; they pay merchants before the banks collect from customers and are therefore extending credit to the merchant, that’s why Merchant account is considered as a LOAN.

To be responsive to the needs of our merchants and to meet that needs, NTC offers next day funding in addition to the value added service for customers and businesses that need to have their funds available quickly.

National Transaction also offers a variety of electronic payment services and technology for businesses; with more than 15 years of experience.

Our services include:

Currency Conversion

Credit and debit card processing

E-commerce and gateways

Electronic checks

Gift and loyalty card programs

Mobile processing

Cash advances and loans/funding program

NTC e-Pay and MediPaid

NTC e-Pay – is an Electronic Invoicing that made simple with NTC e-Pay!

Free Setup, nothing to Integrate, Secure, and Fast. Invoice customers Electronically with NTC e-Pay. In addition, our e-Pay Platform can help Travel Merchants bring new customers while encouraging repeat business.

Our Virtual Merchant Gateway – accept payments your way! Online, In-Store and On the Go. Another payment platform that flexes with your business.

NTC Business Loans – Fast yet Affordable and most of all Simple Application Process.

MediPaid – another medical health insurance claims payment. Delivering paperless and next-day deposits for Health Insurance Payments.

Furthermore, NTC provides services to thousands of customers. NTC maintains a one on one relationships with all its merchants consequently providing 24/7 customer service and technical support!

To know more about our product and services call us now! 888-996-2273

National Transaction offer valuable features and benefits. If you want to improve your business’s productivity, you should look for this features that you need from your merchant account provider.

Advanced Security Options – did you know that 6 out of 10 small businesses close within six months of a card data breach? Point-of-Sale devices should have appropriate security measures, particularly EMV, encryption and tokenization. With National Transaction we have Safe-T for Small and Medium Businesses and Safe-T for Large Businesses. Top-tier security is important on all your business’s data especially customer information, consider adding additional authentication procedures. Merchant account providers bundle various security features to make the process of becoming secure.

Fast Payment Processing – having up-to-date technology is the first step because some customers might become annoyed by slow service and leave. The sooner you have the money processed by your merchant account provider, the bigger and stronger your business can become. NTC is adept at administering payments quickly and efficiently. We can provide regular funding or next day funding.

Feature Flexibility – Look for a merchant provider that appropriately addresses your payment concerns. Obtaining the features you need from your merchant services provider is very important.

Mobile Payment Processing – NTC offer Virtual Merchant/Converge Mobile that gives you the ability to accept payments using your smartphone or tablet anywhere you go. The app works with most Apple and Android mobile devices. You can accept key-entered transactions or swipe cards using an encryption reader. You can now take chip card payments using Ingenico iCMP PIN Pad. Merchants who aren’t mobile payment capable do demonstrate unwillingness to progress with payment technology and might lose customers eventually.

Reliable Customer Support – NTC is available 24/7 answering the phone by humans and not automated systems. You got support with your hardware, answer questions and guide you to better understand the process. Customer support is perhaps the most important feature of any business partnership you make. You don’t want to choose the wrong provider.

Up-to-Date Tech – futuristic features, like mobile payment abilities, EMV/NFC, contactless payments are worth investing. Modern consumers are generally more familiar with up-to-date payment systems. Seeing a merchant service provider offer a swipe-only terminal should be a red flag, because the recent regulations require merchants to have EMV to provide better data security.

Application Fee – is a fee charged to cover the costs of processing and assessing your loan application.

Bank Wire Fee – When borrowing a loan, lenders commonly wire the money to your bank account via ACH, because the banks need to talk to each other and ensure the money is going to the right place and that no fraud is going on.

Check Processing Fee – ACH transfers are commonly used to collect periodic repayments from the debtor’s bank account. Some lenders offer the option of paying by check, but you’ll have to pay a fee for the extra cost involved.

Closing Cost – not to be confused with closing fees, encapsulate all the fees charged for processing a loan, including origination/closing fees, processing fees, referral fees, and/or packaging fees.

Draw Fee – similar to an origination fee, but is applicable instead for lines of credit.

Guarantee Fee – is charged on all SBA loans above $150K. Guarantee fee is charged to protect against credit-related losses in the mortgage portfolio.

Late Payment Fee – Missing a payment deadline can result in a late fee. A late payment may have an affect on your personal or business credit score.

Origination Fee – an up-front fee charged for processing a new loan application. Prepayment

Penalty – Is a borrower, a bank or mortgage lender agreement that regulates what the borrower is allowed to pay off and when.

Servicing and Maintenance Cost – fees charged to cover the costs associated with collecting payments, maintaining records, following up on delinquencies and any other costs associated with maintaining a term loan or line of credit.

Business loans are available in different types, from merchant cash advances to lines of credit. The most effective way to get the best deal on a business loan is to be educated and know that Fees are Negotiable.

A number of financial institutions are beginning to implement biometric authentication. They started to replace traditional knowledge-based passwords with biometric authentication.

A British multinational banking is introducing biometric tests for its customers in U.K., letting account holders access online banking using their fingerprint or voice. If you’re using phone-banking services you can register your voiceprint with the company instead of using a regular password. A special voice biometrics technology will analyze a customer’s voice when they call the bank.

Customers using Apple’s Touch ID will be able to access their accounts on their mobile phones using their fingerprint.

Customers in the U.S., Canada, Mexico, Hong Kong, and France will have the technology by the end of the year. Other markets will follow in 2017 and 2018. The British multinational banking and financial services company have nearly 50 million retail banking customers around the world.