Category: Smartphone

March 3rd, 2016 by Elma Jane

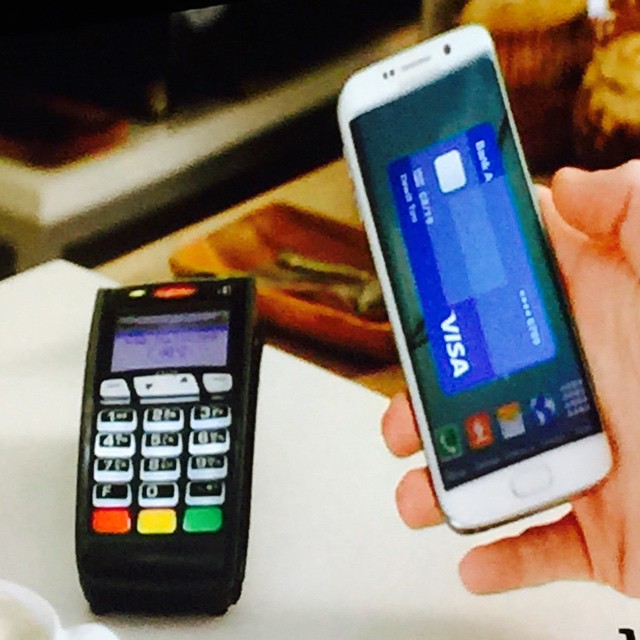

Apple and Samsung, Plus HCE, Lending Momentum to Contactless

EMV migration in the U.S. is helping to establish NFC since nearly all EMV terminals come with built-in NFC capability. Consumers worldwide will make mobile payments with their handsets using near-field communication this year, nearly 70% will be Apple Pay and Samsung Pay users.

Some banks were offering mobile wallets based on HCE. Banks have responded to HCE because its cloud configuration stores and manages payments information, bypassing the secure element in the phone. This allows banks to introduce tap-and-pay mobile-payments services quickly because it eliminates the need to negotiate terms with mobile carriers and device manufacturers to gain access to the secure element. Cloud-based credentials can be tokenized to protect from hackers. Tokenization and HCE combination is extremely attractive to banks.

Apple, Samsung and a cloud-based technology host card emulation are playing a big role in spreading contactless payments.

Posted in Best Practices for Merchants, EMV EuroPay MasterCard Visa, Mobile Payments, Mobile Point of Sale, Near Field Communication, Smartphone Tagged with: banks, consumers, contactless, contactless payments, EMV, HCE, host card emulation, mobile, Mobile Payments, mobile wallets, Near Field Communication, nfc, payments, terminals, tokenization

February 23rd, 2016 by Elma Jane

Cardless ATM’s Could Help Push Mobile Wallet Adoption

The mobile wallet will be the payment method in five to 10 years.

Cardless ATM transactions is a great way to introduce smartphones as payments devices. It could help with the adoption of mobile payments and wallets. Mobile Smart Phones will become the piece of plastic and cards will be a thing of the past…

A multinational banking corporation intends to use (NFC) near-field communication for its service. It will let customers leverage NFC technology on their smartphones to authenticate at the bank’s ATM without a debit card.

An NFC cardless ATM transactions could be compatible with Apple Pay which uses NFC technology.

Benefits:

Speedier ATM cash withdrawal takes about 15 seconds without the debit card compared with 60 to 90 seconds with a debit card, whether it’s a chip or magnetic-stripe transaction.

Safer ATM transaction. No physical connection between the phone and ATM, skimming device to intercept the transaction is gone.

The barcode represents the time of day and what terminal the transaction is taking place at. Everything is tokenized.

Cardless ATM transactions are interesting and an appropriate evolution.

Posted in Best Practices for Merchants, Near Field Communication, Smartphone Tagged with: banking, cards, debit card, Mobile Payments, mobile wallet, Near Field Communication, nfc, payments, transactions

January 28th, 2016 by Elma Jane

The shift to EMV is helping to address vulnerabilities in the United States payments ecosystem. It has been shown that EMV can deliver benefits as a part of industry efforts to combat fraud.

EMV migration is a critical focus for enhancing payments security, which is why the current efforts around chip card deployment are greatly beneficial for consumers and merchants alike. EMV technology helps to reduce counterfeit card fraud, as it generates dynamic data with each payment to authenticate the card, after which the cardholder is prompted to sign or enter a PIN to confirm their identity.

The EMV rollout represents a dynamic time for card payments that promises great advances, among them is enhanced security for cardholders. It also presents an opportunity to consider other innovations such as mobile wallets and mobile POS to further engage your customers and drive customer loyalty. When merchants continue to invest in EMV and NFC (near field communications, used for tap-and-pay transactions), the purchases made at their EMV-enabled terminals are made more secure than magnetic stripe.

New mobile payment options such as mobile wallets support EMV and therefore offer this added layer of security. Ultimately, by enabling contactless payments, merchants can also enable more flexibility in addition to increasing security for their customers.

Additionally, industry players are backing major mobile wallets, such as Android Pay, Apple Pay, and Samsung Pay.

Posted in Best Practices for Merchants, Credit Card Security, EMV EuroPay MasterCard Visa, Smartphone Tagged with: card, cardholder, chip card, consumers, contactless payments, customers, data, EMV, fraud, magnetic stripe, merchants, mobile, mobile payment, mobile wallets, near field communications, nfc, payments, PIN, POS, Security, terminals, transactions

January 18th, 2016 by Elma Jane

EMV + NFC = BIG PLUS FOR YOUR BUSINESS

The business is already making upgrades, so If you’re a merchant, business owner who’s still on the fence about upgrading your payment processing equipment to accept EMV cards why not take that upgrade a step further and add NFC while adding EMV systems?

Not only will the upgrade help prevent potential financial responsibility for fraudulent transactions, but you can also realize the added benefit of being able to process NFC transactions at the same time.

Customers want the ability to pay with a mobile device, and NFC will allow for such transactions to go on.

Having NFC tools in place will help provide a valuable note of future-proofing to systems in place, being ready for it will be to the business’ benefit.

EMV and NFC technology is just good business sense for three important reasons Added Security, Economic Sense and Staying Current.

For more information about terminal upgrade and features that suits best for your business give us a call at 888-996-2273.

Posted in Best Practices for Merchants, EMV EuroPay MasterCard Visa, Mobile Payments, Near Field Communication, Point of Sale, Smartphone Tagged with: cards, customers, EMV, merchant, mobile, nfc, Security, transactions

December 16th, 2015 by Elma Jane

Google’s contactless payment solution, Android Pay, will now be available through the mobile checkouts of several Android apps in the U.S.

With this addition, it avoids having to pull out your card everytime you make a purchase, meaning card data never makes it to the merchants. A good news for anyone who is concerned about privacy.

Android Pay is compatible with all Near Field Communication (NFC) or Host Card Emulation (HCE) enabled devices using any OS released since KitKat.

With Coca-Cola signing up as the first merchant in the Google program, a new loyalty program was recently released for the mobile wallet, by tapping your phone on an NFC-enabled Coke vending machine, you’ll get a Coke and get points added into your Android Pay Account for future purchases.

http://www.pymnts.com/news/payment-methods/2015/android-pay-now-in-app-payment-option/

Posted in Best Practices for Merchants, Credit Card Security, Mobile Payments, Smartphone Tagged with: Android Pay, card, card data, contactless payment, HCE, host card emulation, loyalty program, merchants, mobile wallet, Near Field Communication, nfc, payment

December 14th, 2015 by Elma Jane

Samsung Pay now supports 50 popular merchant gift cards as well as a gift card store that enables users to buy gift cards from supported merchants, within the Samsung Pay app. According to press release, more gift card options will be added to Samsung Pay in the coming months. Samsung Pay is bringing consumers an easier way to use gift cards. With Samsung Pay, you can easily carry your gift cards with you everywhere you go and not to have to worry about a card going unspent.

http://paymentweek.com/2015-12-14-samsung-pay-adds-support-for-popular-gift-cards-9116/

Posted in Best Practices for Merchants, Smartphone Tagged with: cards, Gift Cards, merchant

December 7th, 2015 by Elma Jane

Most payments will probably be made with apps in phones or smartwatches in less than a decade from now, using NFC, biometrics or other mechanisms that don’t involve swiping or using plastic cards.

If your mobile device has an integrated NFC chip, you can use a mobile wallet app like Apple Pay and Android Pay to pay for items that support NFC transactions at a retail store. Simply wave your device near an NFC compatible terminal to pay, no card swiping required.

Both Apple Pay and Android Pay have fingerprint scanners on phones, you can enable payments with just a fingerprint scan.

In some countries, it’s easy for consumers to get credit cards with imbedded NFC chips. This means that you may be able to wave your card at the terminal instead of swiping, no phone required. In America, though, because NFC hasn’t caught on until recently, analysts expect that NFC via smartphone and smartwatch services such as Apple Pay and Android Pay will dominate contactless transactions in the next few years.

Just as credit cards replaced cash, credit cards will be replaced by digital payments which will continue to rely on the credit infrastructure but will obscure the plastic card itself.

As consumers, we love to see better products. When it comes to payments, we need Standards and Reliability.

Posted in Best Practices for Merchants, Mobile Payments, Mobile Point of Sale, Near Field Communication, Smartphone Tagged with: biometrics, cards, contactless transactions, credit cards, digital payments, mobile wallet, nfc, NFC chip, payments, smartphone, terminal

November 17th, 2015 by Elma Jane

Within the payment processing industry, Merchant accounts are categorized according to how they process their transactions.

There are two primary merchant account categories:

Swiped (Card Present) and Keyed (Card-Not-Present).

Swiped or Card-Present Transactions: Are those in which both the card and the cardholder are present at the time the payment is processed, they physically swipe their customers credit card through a terminal or point-of-sale system.

The sub-categories within this group include:

Retail Merchants – Normally conduct their business in an actual storefront or office space. They primarily use counter-top terminals or Point-of-Sale systems. Restaurant Merchants – Requires a special set-up that allows for tips to be added to the final sale amount by settling the transaction with an adjusted price that will include the tip amount.

Wireless / Mobile Merchants – They use wireless terminals or mobile phones to run these transactions in Real-Time. Have the ability to accept credit cards transactions wherever they are located out on the road.

Hotel / Lodging Merchant – Will authorize a customer’s credit card for a certain sale amount.

Card-Present Transactions also include grocery stores, department stores, movie theaters, etc. Card acceptance settings where cardholders use unattended point-of-sale (POS) terminals, such as gas stations, are also defined as card-present transactions.

Keyed-In or Card-Not-Present Transactions: Whenever the transaction is completed and the cardholder (or his or her credit card) is not physically present to hand to the seller.

The sub-categories within this group include:

Mail Order / Telephone Order (MOTO) – The customers card information is gathered via over the phone, fax, email or internet and then manually key-entered into a terminal or payment gateway software. Once the transaction is approved and completed, the product is then shipped to the customer for delivery.

eCommerce / Internet – Conduct ALL of their business over the internet through a web site. So all credit card transactions are processed online via a payment gateway in real-time. The payment gateway is integrated into the web sites shopping cart. The cardholders card is charged instantly.

Travel Merchants is one example of Keyed or Card-Not-Present Transactions.

Start processing credit card payments today whether Swiped or Keyed.

Give us a call now at 888-996-2273 so more details!

Posted in Best Practices for Merchants, e-commerce & m-commerce, Mail Order Telephone Order, Mobile Payments, Mobile Point of Sale, Point of Sale, Smartphone, Travel Agency Agents Tagged with: Card Not Present transactions, card present, card-not-present, card-present transactions, cardholder, credit card, credit card payments, credit card transaction, ecommerce, keyed, Lodging Merchant, mail order, merchant accounts, merchants, mobile merchants, moto, payment gateway, payment processing, point of sale, POS terminals, Restaurant Merchants, Retail Merchants, shopping cart, swiped, telephone order, terminal, transactions, travel merchants

November 5th, 2015 by Elma Jane

EMV-compliant POS systems are now being equipped with NFC technology to accept contactless payments. What does this mean for the future of payments?

EMV lays the foundation for increased card-present and contactless payments security, with EMV, magnetic stripe cards are soon to be a bygone technology. Plastic EMV cards will not have a long lifespan as payments move into a more digital space, security and NFC upgrades merchants and consumers now will carry over into the digital and mobile payments space.

Consumers are constantly looking for more convenient ways to transact, which is made possible by the simultaneous adoption of EMV and NFC. While EMV supports plastic chip cards, payments are going digital and POS systems equipped with NFC technology save consumers from digging through their wallets, making it easier for consumers to transact via mobile devices. Mobile payments should be simple, scalable and affordable in today’s payment landscape and consumers should have the option to securely store and use multiple cards within their digital wallets or applications they most often use.

EMV standards increase security for card-present payments, which are relevant to many consumers today, but the convenience of mobile and contactless payments is the future. In an era of EMV, NFC plays as critical a role in propelling both technologies forward. Retailers and card issuers alike must recognize the opportunity to take advantage of both.

Posted in Best Practices for Merchants, Credit Card Security, EMV EuroPay MasterCard Visa, Smartphone Tagged with: (POS) systems, card present, chip cards, contactless payments, Digital wallets, EMV, magnetic stripe cards, merchants, Mobile Payments, nfc technology, payments

October 13th, 2015 by Elma Jane

What can near field communication do for individual and how can it make lives easier. Many uses of NFC technology offer benefits in a number of everyday tasks ranging from paying for groceries to receiving adequate health care treatments.

Check this out if the benefits are worth it:

Contactless Payments – well-known use of NFC technology is for contactless payment. Customers can use their smartphone over a card reader to make a purchase without swiping or counting out cash. This saves time and also reduces the chances of losing a credit card that comes with carrying multiple cards around.

Health Care – With NFC technology, hospitals can better track patient information and doctors’ notes in real-time. This helps prevent the wrong medications from going to the wrong patient and creates a streamlined system focused on the best in patient care.

Information Sharing – NFC tags most common way NFC is currently used on Android and Windows phones. Using your Phone or Tablet, you can tap a strategically-placed NFC tag, which prompts your phone to take action on something, like automatically prompts your phone to enable Wi-Fi, disable sounds and decrease brightness. Exchange information between two Android phones.

Pairing with Devices – Smart household appliances are adopting NFC. LG’s smart washing machines let you pair your phone with the machine so that you can remotely monitor the washing cycle.

Social Networking Social networking is booming, and NFC tags are looking to get in on the action. NFC allows users to interact with each other and update their location and other info without any unnecessary log-ins or tapping through menu screens.

Transportation – Swiping a smartphone not only allows the passenger access to the subway but also keeps track of the number of trips he has left. Passengers can come and go much faster and easily pay for extra trips.

Posted in Best Practices for Merchants, Near Field Communication, Smartphone Tagged with: Android, card reader, contactless payment, credit card, health care, Near Field Communication, nfc technology, smartphone