Credit card transaction types are categorized based on the level of risk and processing cost associated with them. Here’s a breakdown of the common types:

1. Qualified

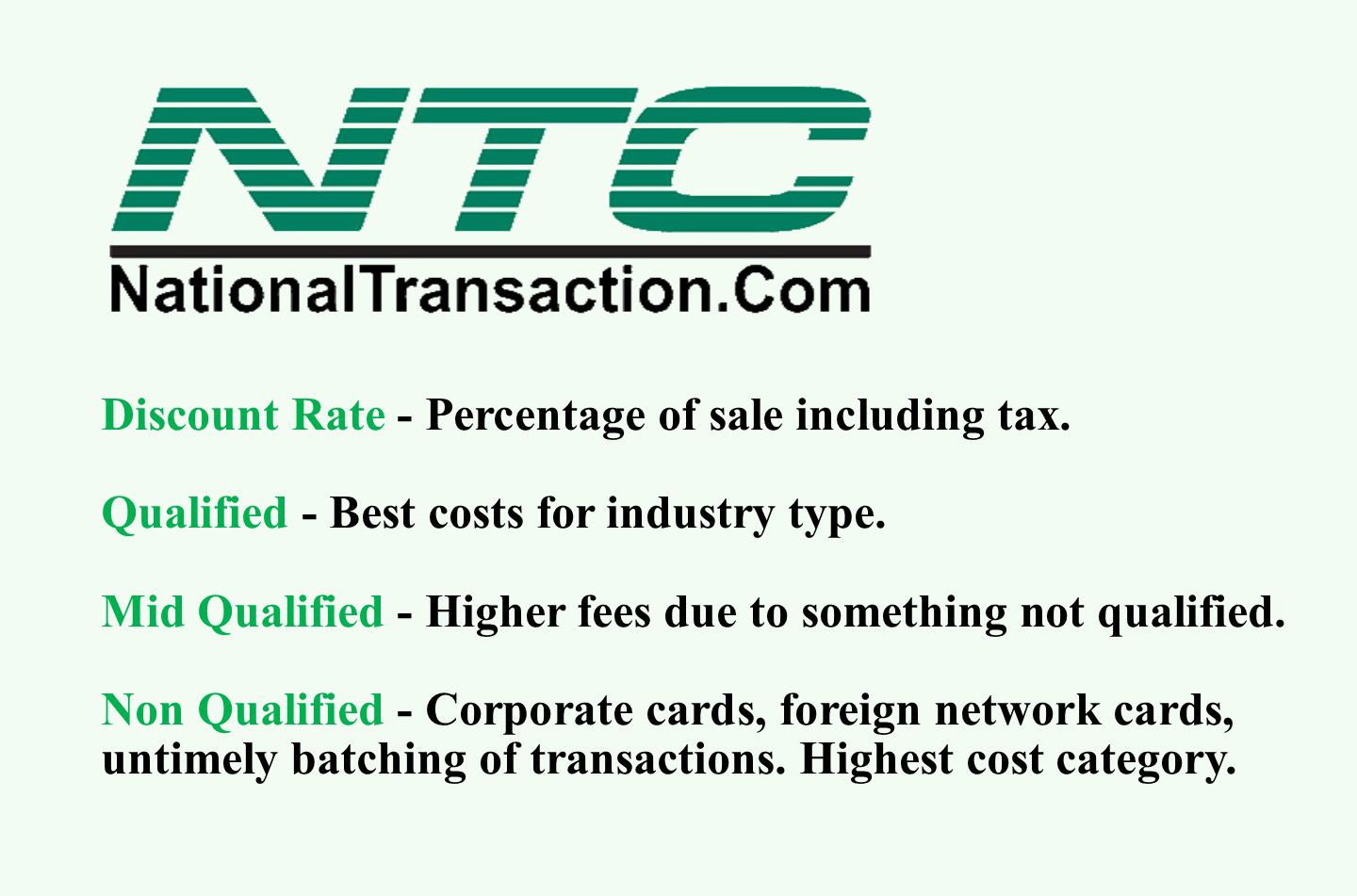

Definition: These are considered the “safest” and least expensive transactions for processors to handle.They typically involve traditional credit or debit cards processed in person with a physical card swipe or chip insertion.

Characteristics:

Card is present during the transaction

Cardholder’s signature is captured (if required)

AVS (Address Verification Service) matches the billing address on file

CVV (Card Verification Value) is provided and matches

Transaction meets all security protocols and risk assessment criteria set by the card issuer and processor.

Examples:Swiping a standard Visa or Mastercard credit card at a retail store.

2. Mid-Qualified

Definition: These transactions fall in between qualified and non-qualified in terms of risk and processing cost. They often involve card-not-present transactions or cards with higher reward structures.

Characteristics:

Manually keyed-in transactions (online, over the phone, or mail order)

Rewards cards with higher cashback or points benefits

Business or corporate cards

Transactions where AVS or CVV information is not provided or doesn’t match

Examples: Entering your credit card details online to purchase something, using a rewards card with travel benefits.

3. Non-Qualified

Definition: These transactions are considered the riskiest and most expensive to process.They often involve international cards, manually keyed transactions without proper security measures, or cards with very high reward programs.

Characteristics:

International credit cards

Manually keyed transactions without AVS or CVV verification

High-risk businesses like online gambling or adult entertainment

Keyed transactions for business or corporate cards

Examples: Using a foreign-issued credit card, manually processing a transaction without verifying the cardholder’s address.

Why does this matter?

Processing Fees: Merchants are charged different fees for each transaction type.Qualified transactions have the lowest fees, while non-qualified transactions have the highest.

Tiered Pricing: Many payment processors use tiered pricing models, categorizing transactions into these types and charging accordingly. This can sometimes be confusing or lead to unexpected costs for merchants.

Interchange Fees: The card networks (Visa, Mastercard, etc.) also charge interchange fees for each transaction, which vary based on factors similar to those used for transaction type categorization.

Understanding these transaction types is crucial for merchants to:

Negotiate better processing rates: By understanding the factors that influence transaction categorization, merchants can negotiate better fees with their processors.

Optimize payment processing: Merchants can take steps to minimize the number of mid-qualified and non-qualified transactions, such as encouraging in-person payments or using address verification systems.

Control costs: By being aware of the different transaction types and their associated costs, merchants can better manage their payment processing expenses.

Remember: The specific criteria for each transaction type can vary depending on the payment processor, card network, and individual merchant account. It’s always best to clarify with your payment processor to understand their specific categorization rules and fee structures.

To establish a merchant account for your business call now 888-996-2273 or click here NationalTransaction.Com