November 18th, 2016 by Elma Jane

Tokenization and Encryption are completely different technologies when it comes to securing sensitive data, such as credit cards.

Encryption tools and techniques is to mask original data, then allow it to be decrypted. It uses an algorithm to scramble credit card information that makes the data unreadable to anyone.

Encryption is most often “end-to-end.”

Example: When someone enters card data into a web browser to buy an item and decrypted when the purchaser’s authorized credit card information reaches its intended destination, which is the merchant’s e-commerce database.

Encrypted card data is unreadable while it’s “at rest” in a database or “in motion” during a purchase transaction; and inaccessible until a key decrypts it. The chances of a hacker stealing the data is minimal. But, if card data passes through multiple internal systems en route to an acquiring bank or payment gateway, the encrypt/decrypt/re-encrypt process could open a wide security hole, thus creating vulnerabilities to hackers.

Tokenization have found to be cheaper, easier to use and more secure than end-to-end encryption.

Tokenization completely removes credit card data from internal networks and replaces it with a generated, unique “token”. Tokens have no meaning and are worthless to criminals if a company’s system is breached.

Merchants use only the token to retrieve, access, or maintain their customers’ credit card information.

Example: Actual credit card number was 3234 4567 8789 78910, it might become FHIW145BVE65478 when a token is generated. The token is randomly generated and there is no algorithm to regain the original card number. hackers can’t reverse-engineer the actual credit card number, even if they were to grab the tokens off the servers.

Using tokens doesn’t change a merchant’s payment processing experience. Only they’re much safer for a merchant than actual credit cards.

Posted in Best Practices for Merchants, Credit Card Security Tagged with: card, credit cards, customers, data, encryption, gateway, merchants, payment, Security, token, tokenization, transaction

November 17th, 2016 by Elma Jane

Payment Card Industry

What is PCI DSS (Payment Card Industry Data Security Standards)? A set of requirements, founded by Amex, Discover, JCB, MasterCard and Visa; to facilitate industry-wide adoption of consistent data security measures on a global basis. Best practices for enhancing payment account data security.

Why does my business need to be PCI Compliant? You help protect your business

by reducing the risk of a costly breach of your customers’ payment card data. Payment card brands (Amex, Discover, JCB, MasterCard and Visa) mandate that all businesses processing payment cards must be compliant.

Once my business validates PCI-DSS compliance, does that prevent a security breach from happening? No. It helps prevent security breaches and loss of cardholder data but do not provide a guarantee to your business. Also, similar to the regularly required updates to anti-virus and firewall software; data security is also continually subject to new threats.

What happens to my business if I am not PCI Compliant? If you do not comply with the security requirements contained within PCI-DSS as mandated by the payment card networks; you put your organization at risk of a payment card compromise.

In the event that your business is compromised, you may also be subject to additional fines, fees, and assessments by the card brands. You may also lose your credit card acceptance privileges.

What am I required to do to validate PCI compliance? The minimum requirement for PCI Level 4 business is to complete a PCI-DSS Self-Assessment Questionnaire (SAQ) on an annual basis and achieve a passing status.

Posted in Best Practices for Merchants, Payment Card Industry PCI Security Tagged with: card, credit card, customers, data, payment, PCI, Security

October 13th, 2016 by Elma Jane

Code 10 merchants first line of defense!

How to use “Code 10”

- Call the voice authorization phone number provided by your Merchant Provider. This number can be found on the sticker on your terminal or call your Merchant Service provider and ask to be transferred to the Voice Authorization department.

- Choose the prompt for “Code 10”. Never call a phone number for the card issuing bank provided by a customer; or let the customer call the card issuing bank for you to obtain an authorization code. Do not accept an authorization code given to you by a customer. Authorization code obtained from your Authorization Center can be verified; but not the one from other sources.

- Provide the cardholder name, billing address and shipping address, if the order is a mail order, phone or Internet sale. The representative will attempt to verify the information you provide with the bank that issued the card to the customer.

- The representative will attempt to verify the cardholder information during your call; the data will be forwarded to an investigator for further research and will attempt to contact you within 24 – 72 hours with the current status or results of the investigation.

- Request another form of payment other than a credit card if an authorization request is declined. Do not split a declined transaction into smaller increments to obtain an authorization.

- Obtain an authorization code for the full amount of the sale. Always obtain the authorization code before shipping the merchandise.

Whether you are in a face-to-face environment, or via mail, phone or Internet that sell goods and services you can employ a “Code 10” authorization to verify additional information on a suspicious transaction.

You may be prompted by your processing terminal to call for voice authorization of the charges (CALL AUTH), or you may simply not feel right about the transaction. In either case, you can use “Code 10” to gain additional information before you release your merchandise.

Posted in Best Practices for Merchants, Credit Card Security Tagged with: bank, card, cardholder, customer, internet, merchant provider, merchants, service provider, terminal, transaction

October 11th, 2016 by Elma Jane

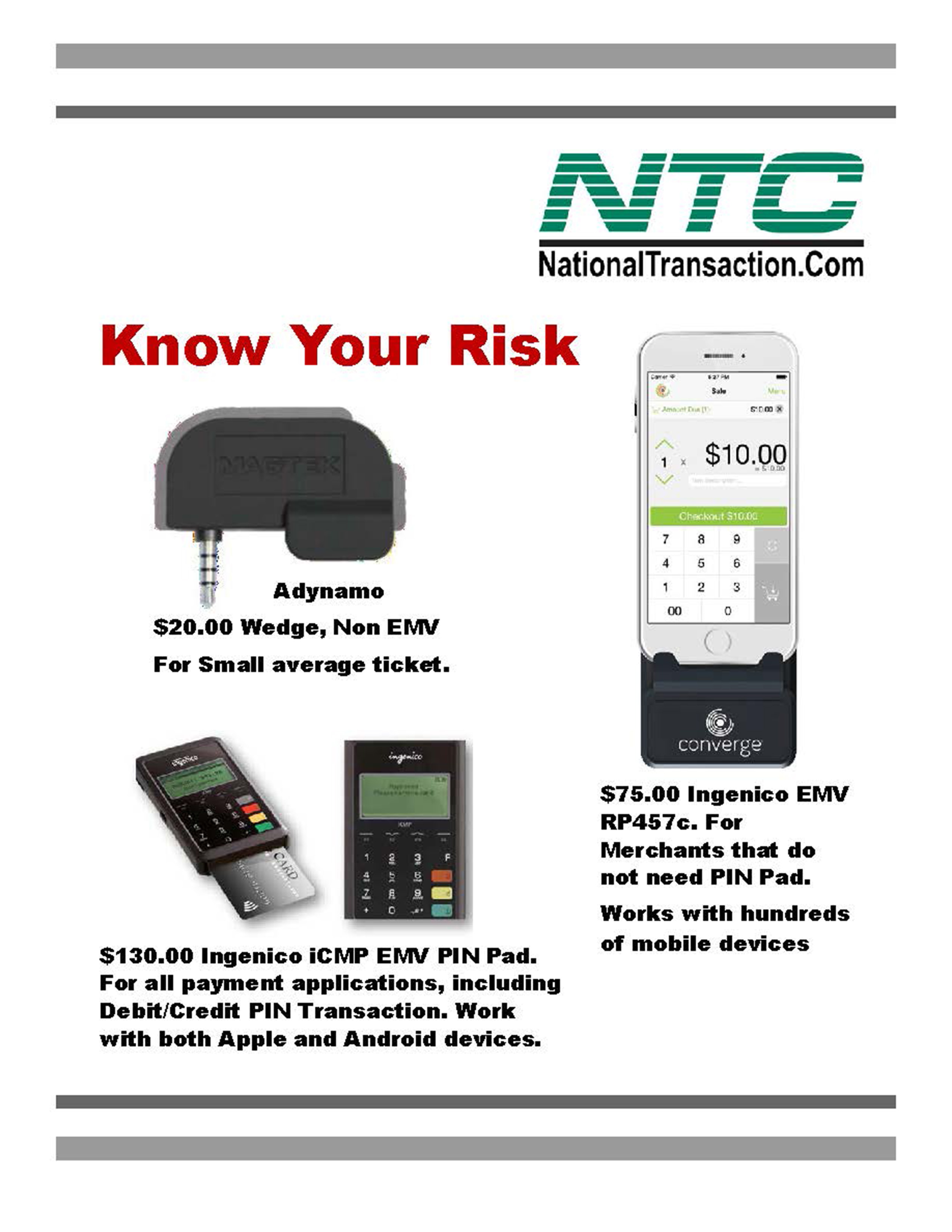

Cybersecurity via Converge:

Converge uses a multi-layered approach to security which helps keep cardholder data safe throughout the entire payment process; from beginning to end.

- EMV: All new Ingenico PIN pads and readers – iCMP and RP457c used with Converge Mobile offer EMV to help protect against counterfeit card use. The PIN pads go a step further in helping protect against lost; stolen and NRI (never received/issued) when a PIN-preferred card is accepted with PIN entry.

- Encryption: All new Ingenico devices also include encryption as a standard security component in addition to protect card data in transit.

- Tokenization: An enhanced security feature that is particularly valuable in card-not-present (CNP) environments when cards are stored on file for processing at a later time, or either for recurring/installment payments.

Get the Ingenico iCMP EMV PIN Pad for only $130.00.

For all payment applications, either Debit or Credit PIN Transaction. Work with both Apple and Android Devices.

Ingenico EMV RP457c card reader for only $75.00.

For Merchants that do not need PIN Pad. Works with hundreds of mobile devices.

Posted in Best Practices for Merchants, Credit Card Security, EMV EuroPay MasterCard Visa, Mobile Payments, Smartphone Tagged with: card, card-not-present, cardholder, data, EMV, mobile, payment, PIN pads, Security, tokenization

September 29th, 2016 by Elma Jane

MerchantConnect is a great tool for merchants because it contains all the information that a merchant needs to manage their electronic payment activity. Furthermore, it’s fast, easy and secure!

- Merchant can either view or update account information and make changes.

- Find copies of statements.

- Furthermore find valuable products and services to help merchant with their business.

View recent deposits and other information about account activity including:

- Batch Details

- Chargeback

- Retrieval Status

- Deposit History

The merchant can also find news and information to help manage payments at your business. Learn how to:

- Best Qualify Transactions

- Reduce Risk

- Manage Chargebacks

- Find reference guides to help operate your payment terminal

The merchant can also utilize the BIN Lookup when you need to inquire about which bank issued a particular card. Simply enter the first six digits on the card and you will receive the information on the issuing bank, including contact information.

If you need a to set-up an account and want to use this tool give us a call at 888-996-2273

Posted in Best Practices for Merchants, Electronic Check Services, Electronic Payments Tagged with: bank, card, chargeback, electronic payment, merchants, payments, risk, terminal, transactions

July 21st, 2016 by Elma Jane

Always ask for the card security codes:

CVV2 for Visa

CVC2 for MasterCard

CID for Discover and American Express.

Always use the Address Verification Service (AVS) and only process sales after receiving a positive AVS response.

Avoid using voice authorizations, unless absolutely necessary.

Billing descriptor must set up properly and shows your phone number. Customer can contact you directly if there is an issue,

Consider using the associations’ 3-D secure services:

Verified By Visa

SecureCode by MasterCard

A 3-D transaction confirmation proves card ownership and protects you from certain types of chargeback. An additional layer of security for online credit and debit card transactions.

Inform your customers by email when a refund has been issued or a membership service cancelled. Notify them of the date the refund was processed and provide a reference number.

Make available customer support phone number and email address on your website so that customers can contact you directly. You need to meet this requirement before opening a merchant account.

Make it easy for your customers to discontinue a recurring plan, membership or subscription. Have a no-questions-asked policy.

Notify your customers by email of each transaction and indicate that their cards will be charged.

Obtain a confirmation of delivery for each shipment.

Process refunds as quickly as possible.

Secure an authorization approval for every transaction.

Secure customers’ written or electronic signatures, for recurring payments or monthly fees. Giving you express permission to charge their cards on a regular basis.

Terms and conditions must be clearly stated on your website. Customers must acknowledge acceptance by clicking on an Agree or a similar affirmative button.

Transaction amount must never exceed the authorized amount.

You are required to reauthorize the transaction before settling it if an authorization approval is more than seven days old.

Posted in Best Practices for Merchants, Credit card Processing, Credit Card Security, Merchant Services Account Tagged with: card, chargeback, credit, customer, debit, merchant, merchant account, online, sales, Security, service, transaction

July 12th, 2016 by Elma Jane

Interchange is where transactions are submitted for payment from the Acquirer or Merchant Processor to the Card Issuer or Debit Network. It also represents the fees paid by the merchant acquirer to the Card Issuer.

At the time the transaction is exchanged fees are paid and vary based on processing method utilized. It is more expensive to process a hand-keyed transaction than a card-swiped transaction.

Several rates may apply to your transactions, depending on your method of processing each transaction and the interchange qualification that is assigned to each transaction by the Card associations for processing transactions.

Rate qualification criteria: The card associations consider the card product used in the transaction, how the transaction data is entered, the time of settlement versus time of authorization.

Interchange Category Based on Card Type: Credit, Debit, and Rewards purchasing.

Industry Type: Retail or E-commerce.

Qualification Elements: Swiped card or Key entered.

When you settle your transactions each day, Acquirer or Merchant Processor like NTC routes them to the Card Associations (Visa, MasterCard, Discover) and debit networks through Interchange.

Visa, MasterCard, Discover (Card Associations and Debit Networks) establish the rules and manage the Interchange of all transactions.

Posted in Best Practices for Merchants Tagged with: card, card-swiped, credit, debit, e-commerce, merchant, payment, processor, transactions

June 22nd, 2016 by Elma Jane

What is ARC, IATA, and CLIA? what’s the difference? What it does and what type of agents would benefit most from it.

CLIA Number – is issued by the Cruise Lines International Association. It’s a way for vendors to identify you as a travel agent. It serves the same purpose as the ARC or IATA number, it’s just issued by another organization and has different barriers to entry and costs associated with it. CLIA agencies without ARC accreditation cannot issue airline tickets since CLIA numbers were designed specifically for cruise-focused travel agencies. You can always go under an umbrella organization like a host agency, you don’t need to get your own CLIA number if you’re working with a host agency. You can use their identification number and won’t incur the costs associated with obtaining your own CLIA number. While CLIA is accepted nearly everywhere, it’s NOT accepted by the airlines. If you are not issuing airline tickets, CLIA is a practical option.

CLIA vs. ARC/IATA Number – If you’re ticketing air-only reservation, ARC and IATA are must-haves.

ARC (Airlines Reporting Corporation) – gives out these ARC numbers to accredited agencies, which allows travel agencies to issue airline tickets. The use of an ARC number extends from a hotel to a cruise ship booking not only air tickets for travel agencies. For a home-based travel agent or a storefront agency that only books leisure travel (no air), having your own ARC number is too much.

IATA – International Air Transport Association Network (IATAN) use extensive data resource to connect the suppliers to the U.S. travel distribution network. IATAN ID card holders get promotional benefits and concessionary incentives from suppliers (participating members) who identify the agent with an IATA/IATAN number as a valid associate, in addition to approving travel agents for the sale of travel tickets. IATA certifies a referral agent or an affiliate travel agent to find clients for the hosting travel agency’s business needs as well.

Posted in Best Practices for Merchants, Travel Agency Agents Tagged with: agents, card, data, host agency, travel agent, vendors

June 16th, 2016 by Elma Jane

Merchants and cardholders have been challenged by the perceived additional time to complete the EMV transaction.

To address concern over EMV checkout time Visa and MasterCard create an alternate EMV payment process that will improve the speed of transaction:

Quick Chip from Visa is available free-of-charge to acquiring banks, payment networks, and other payment processors to offer to merchants. The enhancement requires only a simple software update to the merchant’s card terminal or point-of-sale system.

M/Chip Fast from MasterCard merchants can easily integrate this with their current systems to provide both speed and security for all chip cards. Designed for select environments where fast transaction times, in addition to security, are at a premium.

The new card network options do not require the financial institution to reissue cards, or the merchants to re-certify their point-of-sale terminals.

Alignment in the payments industry and the ability to process a secure transaction in a timely manner for the consumer experience is important.

Keeping current on the payment industry news like Quick Chip and M/Chip Fast or discussion about EMV developments is a smart move for merchants and cardholder as well.

Posted in Best Practices for Merchants, Credit card Processing, EMV EuroPay MasterCard Visa Tagged with: banks, card, card network, cardholders, chip cards, EMV, financial institution, merchants, payment, payment networks, payment processors, payments industry, point of sale, Security, terminal, transaction

May 24th, 2016 by Elma Jane

Top terms in your Merchant Statement:

Interchange – are the variable fees charged by the card payment networks for processing transaction. Credit card brands set these non-negotiable rates based on card type, business size, and industry.

Ancillary Fees – this include statement, batch and customer service fees, monthly minimums and more.

Authorizations – this section shows the charges per authorization that come from an interchange plus provider and is then split by card brand and transaction type. On your statement, you will see these charges as either AUTH or WAT charges.

Deposit Summary – following the summary is the deposit summary, where lists of your account activity broken down by day and card type.

Discount Rate – every transaction percentage that is deducted as a fee. Rates are categorized as qualified, mid-qualified and non-qualified.

Processing Services – this states your discount rate charges that you receive from your interchanges plus processor. This is divided by card brand and sales volume.

Summary – summary shows the processed sales by AMEX, Discover, JCB, MasterCard or Visa, as well as the total fees paid in order to process these sales. You can find this at the top of your statement.

Other items included in the summary:

Account adjustments, chargebacks, the breakdown of sales by card brand and number of refunds.

Understanding these terms on your statement will give you the confidence to read your merchant account statement with ease.

Posted in Best Practices for Merchants Tagged with: card, chargebacks, credit card, customer, fees, merchant, merchant account, payment, refunds, service, transaction