Travel environments are unique and transactions are usually keyed in. There’s almost always a delayed delivery period, and large ticket transactions.

One card holder may be paying for multiple tickets and they tend to be seasonal; with peak season months generating an unusual spike in their “average” monthly volume and chargebacks, pose a potential threat by travelers who are unable to complete their trip.

These factors can cause for either a reserve or account termination. Therefore travel merchant accounts are considered high risk.

Most merchants do not realize that merchant processors carry a financial risk on merchant accounts, and normally fund merchants prior to receiving payment from the client’s bank. Therefore, a merchant account is an unsecured loan.

The merchant runs a transaction and at the end of the day they settle their batch. The merchant will receive the funds for that batch in their bank account within 2 business days, even though the travel arrangements the client paid for do not take place right away.

Here at National Transaction Corp, we specialize in understanding what makes your transactions as a travel agent unique and how they affect your merchant account.

Educating the merchant and ensuring they have a good understanding of what makes travel merchant account high risk, is one of our specialties.

Call NTC to speak with a Travel Merchant Account Specialist today!

It’s true that the travel agencies are high risk. This is because of the high chargebacks by travelers who fail to complete their trips or stays due to a variety of reasons. It also has to do with the nature of delayed delivery where items or services are sold today but not used/consumed for a delayed period of time. Using the right merchant solutions can make a difference.

You want merchant solutions that help you to manage chargebacks, errant transactions, and terminal messages. Additionally, you should be able to integrate your software with services such as Sabre Red, Sabre, Trams or other accounting programs such as QuickBooks and Peachtree.

With NTCePay, simply create a pay button for any dollar amount. Then send this digital link to your customers via email. The customer reviews the invoice details and enters their payment information to complete payment. You can also create custom links that can be added to your web site or posted to your social media accounts for payment collection. With advanced invoices, you can easily break down payments into installments.

With this service, you avoid the complexities of integrating the software with your shopping cart, point of sale, or accounting system yet still collect your travel payments in a seamless manner.

For Electronic Payment Set Up Call Now! 888-996-227

Visa 3-D Secure (3DS) is a security protocol designed to add an extra layer of protection to online credit card transactions.It aims to reduce fraud by verifying the cardholder’s identity before the transaction is authorized.Visa’s implementation of 3DS is called “Visa Secure.”

Here’s how it works:

Transaction Initiation: When a customer makes an online purchase with their Visa card, the merchant’s website communicates with the Visa network to initiate the 3DS process.

Risk Assessment: The issuer (the cardholder’s bank) performs a risk assessment based on various factors, such as the cardholder’s history, the transaction amount, and the merchant’s risk profile.

Authentication: If deemed necessary, the issuer challenges the cardholder to authenticate their identity. This usually involves a step-up authentication method, such as:

One-time password (OTP): Sent to the cardholder’s registered mobile phone or email.

Biometric authentication: Fingerprint scan or facial recognition.

Knowledge-based authentication: Security questions or personal information.

Verification: Once the cardholder successfully authenticates, the issuer confirms their identity to the merchant.

Transaction Completion: The merchant can then proceed to process the transaction with increased confidence that the cardholder is legitimate.

Integration and Implementation:

Merchants need to integrate 3DS into their online payment systems.This typically involves working with their payment gateway provider or acquiring bank to implement the necessary APIs and protocols.Visa provides detailed documentation and support for merchants to integrate Visa Secure.

Benefits and Features of 3DS:

Reduced Fraud: By verifying the cardholder’s identity, 3DS significantly reduces the risk of unauthorized transactions and chargebacks.

Improved Security: Adds an extra layer of security to online payments, protecting both merchants and customers from fraud.

Shift in Liability: In many cases, if a fraudulent transaction occurs after successful 3DS authentication, the liability shifts from the merchant to the issuer.This can save merchants significant costs associated with chargebacks and fraud disputes.

Increased Customer Confidence: Demonstrates a commitment to security and builds trust with customers, encouraging them to complete their purchases.

Enhanced User Experience: The latest version of 3DS (EMV 3DS 2.0) offers a smoother and more user-friendly authentication experience, minimizing friction during checkout.

Support for Mobile and Digital Wallets: 3DS is compatible with various payment channels, including mobile devices and digital wallets, providing a consistent and secure experience across all platforms.

In conclusion: Visa 3-D Secure is a powerful tool for merchants to enhance the security of their online transactions, reduce fraud, and improve customer confidence.

By implementing Visa Secure, merchants can protect themselves from financial losses and provide a safer and more trustworthy shopping experience for their customers.

For e-Commerce Electronic Payments set up with 3D Secure

Fighting chargebacks is important to a business. Whether you process transactions at a point of sale location or operate an e-Commerce business making sure you have implemented a process to dispute your chargebacks is critical.

Basic concepts that can be used to begin learning how to dispute chargebacks:

Keep accurate records of data that is easily accessible. Keeping track of your sales and products have a much easier time in collecting the information necessary to combat a chargeback.

Act quickly, don’t wait! You only have 10 days to respond to a chargeback or retrieval request. If you do not respond in 10 days you lose to a chargeback, and It gets worse; as you will not be able to re-present your case.

Compile and submit the documents to your processor. Make sure the documents have the original chargeback documents attached as well as the other supporting documents.

Follow up to make sure they have been received. Your processor may have an online system that allows you to submit documents directly into the processor chargeback system and some even allow you to view submitted documents in REAL TIME.

Monitor your chargebacks, this will help you understand what processes work for each specific chargeback type.

The chargeback process was introduced more than four decades ago as a consumer-protection mechanism. It was meant to inspire consumer confidence in payment cards, which were still a novel concept at the time. Fast-forward to today, though, and these forced payment reversals have evolved into a significant problem for online merchants.

Chargeback abuse—commonly known as friendly fraud—is a major source of loss. In fact, chargeback issuances resulting from friendly fraud were expected to reach $50 billion annually in 2020, according to Mercator Advisory Group.

Even then, this figure is a low estimate. It doesn’t account for current trends in a post-Covid environment, where we’ve seen a dramatic increase in friendly fraud. These attacks were already up by the end of March, and there’s no sign that they’re going to slow down.

Covid-19 might look like the source of the problem on a superficial level. If we dig deeper, though, we see four underlying factors behind the preexisting upward trend in chargeback filings:

More fraudsters view the CNP environment as the “channel of least resistance;”

Inconsistency in technologies and regulations across different markets;

The rise of mobile banking;

The response by card networks like Visa and Mastercard.

These four factors carry diverse ramifications for the market. For instance, roughly $118 billion in e-commerce transactions are declined each year, according to Javelin Strategy & Research. Most of these rejected purchases are false positives, meaning the merchant unnecessarily rejected the purchase in hopes of avoiding a chargeback.

Clearly, there’s a growing disconnect between merchants, financial institutions, and card networks regarding how best to address this situation. We can see this reflected in the fact that the rate of chargeback issuances in North America is expected to significantly outpace those in the European market. This is attributed to factors like strong customer authentication protocols required by the Revised Payment Services Directive (PSD2), and more widespread use of 3-D Secure technology.

The pressure is on for industry players to find more comprehensive solutions for chargebacks. These solutions must be data-driven and adaptable, though. Otherwise, the growing disconnect between cardholders, merchants, financial institutions, and card networks will exacerbate existing problems in the market, leading to further losses.

The good news is that, in the meantime, there are strategies merchants can employ to address these concerns. For instance, even though friendly fraud operates by concealing itself behind false chargeback reason codes, it’s still helpful to have a clear understanding of what each reason code means in context.

Merchants can’t avoid friendly fraud in the same way they can detect criminal attacks or eliminate merchant errors. However, they can minimize friendly fraud risk by adopting key best practices, including:

Notifying customers to remind them about recurring payments;

Keeping organized and well-documented transaction records;

Using delivery confirmation when shipping physical goods;

Providing easy access to round-the-clock, live customer service;

Providing a quick response to any refund or cancellation requests.

Also, if a merchant identifies a chargeback as friendly fraud, it’s important to engage that dispute through the representment process. This is a complex, time-consuming process, which is why many merchants opt to outsource their chargeback management. It’s still possible to conduct the process with in-house management. However, it will require strong evidence to support the merchant’s case, such as:

A legible sales receipt

A tracking number

Any emails or transcripts of communications you’ve had with the customer

Delivery confirmation information

A record of in-store pickup

Photographic evidence (when available)

This evidence needs to be contextualized with a chargeback rebuttal letter, explaining why the original transaction was valid. Also, merchants are on a tight schedule. In most cases, they have only a few days to provide a response to their acquirer.

Chargeback management can be a difficult and confusing process. But, with the problem of chargeback abuse only set to grow over time, it’s something merchants can’t afford to take for granted.

—Monica Eaton Cardone is the chief operating office and cofounder of Chargebacks911, Clearwater, Fla.

Safe-T for SMB streamlines the PCI process while providing the layered security needed to protect card data

EMV – Fraud protection at the point of sale

EMV chip technology keeps the consumer’s card in their hand. It also helps protect the business from card-present fraud related chargebacks.

Encryption – Protection of payment card data in-transit

Safe-T scrambles cardholder data using advanced encryption technology, so data is protected at the point of entry, and throughout the authorization process.

Tokenization – Token ID protection of stored payment card data

Safe-T returns a token ID or an alias, consisting of a random sequence of numbers to the point-of-sale so the actual card number is never stored. Token IDs can be used for follow up transactions (i.e. recurring payments, voids, etc.).

Reduced PCI – Protection from complex PCI compliance

Maintaining PCI Compliance can be intimidating – second only, perhaps, to completing your taxes. Safe-T eases this process for customers by reducing the number of PCI Self-Assessment questions by more than 60% from 80 questions to 31.

Financial Reimbursement – Financial protection from a card data breach

Recovering from a card data breach can be costly for a small business. Safe-T offers Card Data Breach Reimbursement to financially protect your customer’s business in the event of a card data breach – regardless of the type of card data breach.

For Electronic Payment Set up with this feature call now! 888-996-2273

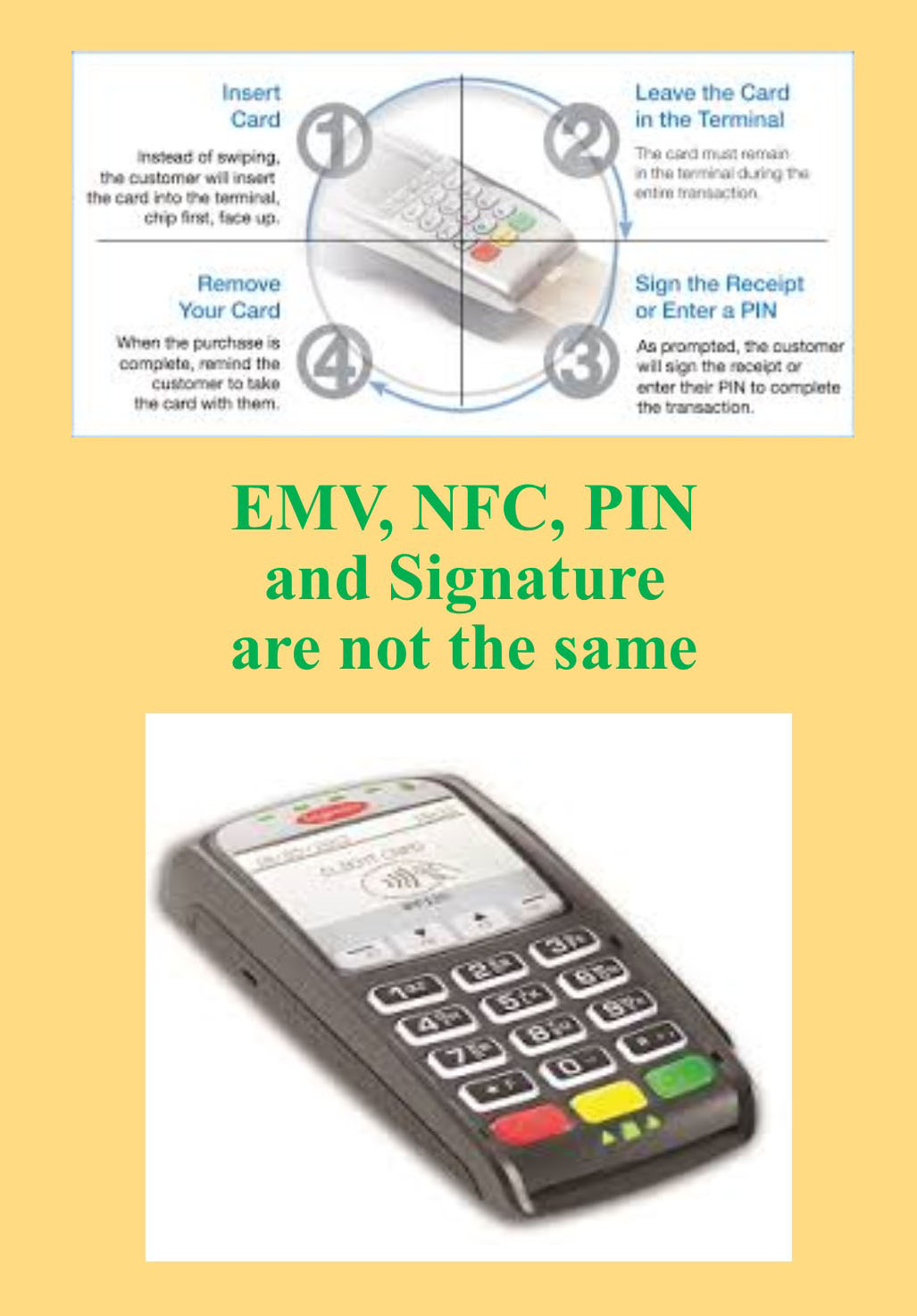

EMV (Europay, MasterCard and Visa) is a payment technology.

NFC (Near-Field Communication) is a technology that enables contactless EMV.

Apple Pay, Android Pay and Samsung Pay uses NFC technology to process payments in a tap at any contactless payment terminal.

NFC payments made with a mobile phone in-store by tapping the phone to an NFC-capable terminal are considered card-present transactions. NFC in-app purchases are considered card-not-present transactions.

Not all EMV terminals has NFC technology. NFC Technology/EMV terminals can be considerably more expensive than standard EMV.

There are EMV terminals that NFC capable but not enabled.

Payment cards that comply with the EMV standard are often called Chip and PIN or Chip and Signature cards, depending on the authentication methods employed by the card issuer.

PIN Debit are transactions routed through (EFT) electronic funds transfer. It immediately deducts the transaction amount from the customer’s checking account, which is linked to the debit card used for payment. EFT processing takes place when the customer chooses debit when prompted and then enters her PIN. PIN debit transactions are often referred to as online transactions because they require an electronic authorization.

PIN Based Transactions have no chargebacks rights as they are considered cash not credit.

Signature-based debit transactions are authorized, cleared and settled through the same Visa or MasterCard networks used for processing credit card transactions. Signature debit processing is initiated when the customer selects creditwhen prompted by the POS terminal. Signature debit transactions are referred to as offline transactions because a PIN debit network does not play a role in processing.

When it comes to electronic payments, certain types of businesses are considered high risk.

Most merchants do not realize that electronic payment processors carry a financial risk on merchant accounts, and normally fund merchants prior to receiving payment from the client’s bank.

Essentially, a merchant account is an unsecured loan.

Different factors used to determine when a business is a high risk are:

Types of products

Services they sell how

How they sell them

Online transactions are considered high risk because there are increased risks of fraud.

A key factor used to determine the risk of a business is chargebacks.

Chargebacks include customer refunds and fraudulent transactions.

Payment providers assess this risk to determine the percentage of chargebacks your business is likely to experience.

Businesses that are considered high risk where they take advanced payments:

Travel agencies

Ticketing services

Electronic payments provider is necessary if you want to accept debit and credit card transactions.

For high-risk electronic payments please feel free to call us at 888-996-2273.

Interchange – are the variable fees charged by the card payment networks for processing transaction. Credit card brands set these non-negotiable rates based on card type, business size, and industry.

Ancillary Fees – this include statement, batch and customer service fees, monthly minimums and more.

Authorizations – this section shows the charges per authorization that come from an interchange plus provider and is then split by card brand and transaction type. On your statement, you will see these charges as either AUTH or WAT charges.

Deposit Summary – following the summary is the deposit summary, where lists of your account activity broken down by day and card type.

Discount Rate – every transaction percentage that is deducted as a fee. Rates are categorized as qualified, mid-qualified and non-qualified.

Processing Services – this states your discount rate charges that you receive from your interchanges plus processor. This is divided by card brand and sales volume.

Summary – summary shows the processed sales by AMEX, Discover, JCB, MasterCard or Visa, as well as the total fees paid in order to process these sales. You can find this at the top of your statement.

Other items included in the summary:

Account adjustments, chargebacks, the breakdown of sales by card brand and number of refunds.

Understanding these terms on your statement will give you the confidence to read your merchant account statement with ease.

Double refunds are when a customer is provided with two refunds for the same transaction. Chargebacks can be involved in a double refund.

Double Refunds Happen When:

Chargebacks are filed after a refund is issued. The consumer contacts the merchant and requests a refund, but the funds aren’t returned immediately. The consumer thinks the request for the refund was ignored and files a chargeback. Then both the chargeback and the refund are being processed.

Chargebacks are filed before a refund is issued. The consumer calls the bank and initiates a chargeback. Then, the consumer calls the merchant and expresses dissatisfaction. To try to avoid a chargeback, the merchant provides a refund. However, the merchant has no idea of the fact that a chargeback has already been filed because the consumer calls the bank first

Even thou a merchant provided a refund with a customer that doesn’t guarantee that a chargeback won’t be initiated. Same thing with chargeback that has been filed doesn’t guarantee that customer won’t contact the merchant and demand a refund as well.

Just because a merchant provided a customer with a refund that doesn’t guarantee that a chargeback won’t be initiated. Same thing with chargeback that has been filed doesn’t guarantee that customer won’t contact the merchant and demand a refund as well.

It is possible for the customer to receive a double refund for the one purchase transaction.