January 12th, 2017 by Elma Jane

Accepting non-cash payments from your customers are valuable. If you don’t, you will miss out on sales; because of the growing numbers of customers who only carry plastic or wish to pay online. Today, you have many payment solution options.

Credit Card Terminals – you might remember the beginning of the credit card era and i’ts evolution with today’s countertop terminals. From the traditional swipe of their credit, debit or even gift card to make a purchase to today’s modern terminals. Like accepting EMV chip cards (to be in compliance with a PCI mandate) and NFC payments like Apple Pay.

Beyond the basics; these systems are generally supported by reporting sites that can help you monitor sales, and assist you with maintaining customer loyalty programs.

E-Commerce Solutions – online sales are growing every year. If you are considering an expansion of your business online; you need a complete hosted payment solution for transactions in all payment environments. Including in-store, back office mail/telephone order (MO/TO), mobile and e-commerce, that make your customers’ experience as intuitive and efficient as possible.

Point of Sale Systems – smart registers have evolved into high-tech point-of-sale (POS) systems due to technology advances. Not only taking customer payments; but it can transform your business with an advanced marketing programs, inventory management and sales and profitability tracking and reporting. Over the past years these advanced systems have become cost-effective and easy to use.

Wireless Terminals – in today’s hardware you have the option of accepting payments wirelessly, through a full-service terminal that is smaller than a countertop model, or through a mobile card reader plugin for a smartphone or tablet.

The advantage of a full-service wireless terminal is that it allows for receipt printing on the spot through the device and most modern full-service wireless terminals are EMV compliant and accept both EMV (chip card) and NFC payment types.

Call now 888-996-2273 and speak to our payment consultant to know which solution is best for you.

Posted in Best Practices for Merchants, Credit Card Reader Terminal, e-commerce & m-commerce, EMV EuroPay MasterCard Visa, Mail Order Telephone Order, Near Field Communication, Payment Card Industry PCI Security, Point of Sale Tagged with: card reader, chip cards, credit card, debit, e-commerce, EMV, gift Card, mobile, moto, nfc, online, payment solution, payments, PCI, point of sale, smartphone, terminals, transactions

June 21st, 2016 by Elma Jane

The Ingenico iPP320 PIN pad (Item Code: 320CV) is officially launched for Converge, making this the third EMV and NFC-enabled device available to our merchants. The iPP320 accepts mag stripe, chip cards, manual card entry and contactless payments, including Apple Pay.

Don’t Forget!

- Customers can hand-key card information into all of the new Converge PIN pads to encrypt payment information at the point of entry, including card-not-present payment environments. Encryption is a standard feature with all new PIN pads.

- In the February release, gratuity support was launched on devices, which means the consumer will be prompted to add a tip to the payment amount using the PIN pad, versus the business entering an amount into Converge.

For terminal upgrade give us a call at 888-996-2273.

Posted in Best Practices for Merchants Tagged with: card-not-present, chip cards, contactless payments, customers, EMV, merchants, nfc, payment

June 16th, 2016 by Elma Jane

Merchants and cardholders have been challenged by the perceived additional time to complete the EMV transaction.

To address concern over EMV checkout time Visa and MasterCard create an alternate EMV payment process that will improve the speed of transaction:

Quick Chip from Visa is available free-of-charge to acquiring banks, payment networks, and other payment processors to offer to merchants. The enhancement requires only a simple software update to the merchant’s card terminal or point-of-sale system.

M/Chip Fast from MasterCard merchants can easily integrate this with their current systems to provide both speed and security for all chip cards. Designed for select environments where fast transaction times, in addition to security, are at a premium.

The new card network options do not require the financial institution to reissue cards, or the merchants to re-certify their point-of-sale terminals.

Alignment in the payments industry and the ability to process a secure transaction in a timely manner for the consumer experience is important.

Keeping current on the payment industry news like Quick Chip and M/Chip Fast or discussion about EMV developments is a smart move for merchants and cardholder as well.

Posted in Best Practices for Merchants, Credit card Processing, EMV EuroPay MasterCard Visa Tagged with: banks, card, card network, cardholders, chip cards, EMV, financial institution, merchants, payment, payment networks, payment processors, payments industry, point of sale, Security, terminal, transaction

April 28th, 2016 by Elma Jane

You can offer your customers preferred payment method with the next generation point-of-sales terminals, an all-in-one credit card processing experience: which not only support Near Field Communication (NFC) contactless payment transactions such as Apple Pay but chip cards and the traditional magnetic stripe cards; and manual entry transactions as well.

Contactless payment transactions are happening now. NTC are here to help.

Posted in Best Practices for Merchants Tagged with: chip cards, contactless payment, credit card processing, customers, magnetic stripe cards, Near Field Communication, nfc, payment, point-of-sales, terminals, transactions

April 27th, 2016 by Elma Jane

EMV Cards (Europay, MasterCard, and Visa) are smart cards (chip cards or IC cards) which store their data on integrated circuits rather than magnetic stripes. They can be contact cards that must be physically inserted or dipped into a card reader. Payment cards that comply with the EMV standard are often called chip-and-PIN or chip-and-signature cards, depending on the authentication methods required.

Posted in Best Practices for Merchants Tagged with: card reader, cards, chip cards, data, EMV, payment

December 18th, 2015 by Elma Jane

A leading provider of mobile point of sale and mobile payment technology, published today the EMV Migration Tracker.

Many merchants have deployed EMV capable terminals while cardholders have received cards with EMV chips, but not much data has been published about the real world use of EMV chip card technology in the U.S. Most published statistics rely on surveys or forecasts rather than real transactional data.

The EMV Migration Tracker shows new data and insights since the October 1 liability shift, including:

- Over 50% of all cards in use now have EMV chips on them. From October to November, the percent grew 5% as banks and card issuers accelerated their rollout of new chip cards.

- Over 83% of American Express cards have EMV chips, while Discover lags at 40%

- Over 63% of the cards used in Hawaii have EMV chips, but Mississippi sees just 11% penetration of chip cards.

While EMV chip card technology has been implemented in Europe years ago, the rollout of EMV in the U.S is just beginning. The rollout came earlier this year with the October 1 liability shift in card present transaction, meaning that merchants who have not upgraded their POS system can become liable for counterfeit card fraud losses that occur at their stores. This is an early step in an ongoing process that the Payments Security Task Force predicts will lead to 98 percent of U.S. credit and debit cards containing EMV chips by the end of 2017.

http://www.finextra.com/news/announcement.aspx?pressreleaseid=62506

Posted in Best Practices for Merchants Tagged with: American Express, banks, card issuers, card present, card technology, cardholders, chip cards, credit, data, debit, Discover, EMV, EMV chips, merchants, mobile payment, mobile point of sale, payment technology, point of sale, POS, provider

November 19th, 2015 by Elma Jane

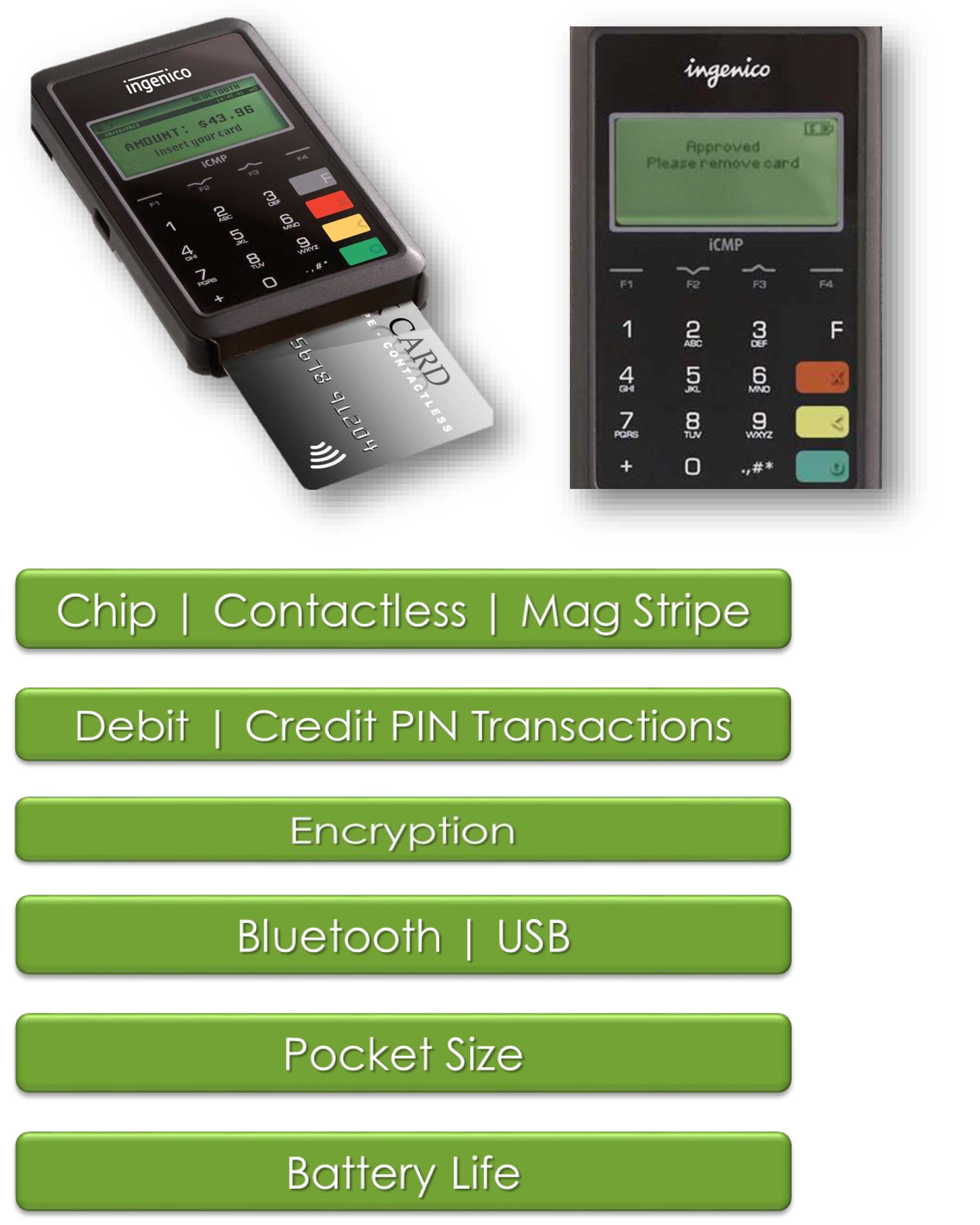

The Ingenico iCMP PIN pad is now available with Converge in the US! This EMV-enabled device is flexible to use with a USB connection and Converge or with a Bluetooth connection and Converge Mobile (launching soon!).

Key features of the Ingenico iCMP include:

Chip, Contactless and Mag Stripe

Accept EMV chip cards, including Chip & Pin and Chip & Signature as well as mag stripe cards and contactless payments – mobile wallets like Apple Pay and contactless cards. The EMV-capabilities of the PIN pad help protect our customers from counterfeit card fraud.

Debit and Credit PIN Based Transactions

Accept debit and credit cards using PIN capabilities on the device. This is important to help further protect our customers from lost, stolen and NRI (not received/issued) fraud.

Encryption

Encrypted to keep card data separate and away from the mobile app/device and safe as it travels through the payment network.

Bluetooth or USB

Connect with a USB connection when using a computer and Converge www.convergepay.com or Bluetooth when using with the upcoming Converge Mobile app.

Pocket size

Takes up little space on a countertop, and it’s easy to carry when on the go.

Give us a call now at 888-996-2273.

Posted in Best Practices for Merchants Tagged with: Apple Pay, card data, Chip & PIN, Chip & Signature, chip cards, contactless cards, contactless payments, Converge, Converge Mobile, credit cards, Debit and Credit, EMV, encryption, ingenico, mag stripe, mobile wallets, payment network, transactions

November 5th, 2015 by Elma Jane

EMV-compliant POS systems are now being equipped with NFC technology to accept contactless payments. What does this mean for the future of payments?

EMV lays the foundation for increased card-present and contactless payments security, with EMV, magnetic stripe cards are soon to be a bygone technology. Plastic EMV cards will not have a long lifespan as payments move into a more digital space, security and NFC upgrades merchants and consumers now will carry over into the digital and mobile payments space.

Consumers are constantly looking for more convenient ways to transact, which is made possible by the simultaneous adoption of EMV and NFC. While EMV supports plastic chip cards, payments are going digital and POS systems equipped with NFC technology save consumers from digging through their wallets, making it easier for consumers to transact via mobile devices. Mobile payments should be simple, scalable and affordable in today’s payment landscape and consumers should have the option to securely store and use multiple cards within their digital wallets or applications they most often use.

EMV standards increase security for card-present payments, which are relevant to many consumers today, but the convenience of mobile and contactless payments is the future. In an era of EMV, NFC plays as critical a role in propelling both technologies forward. Retailers and card issuers alike must recognize the opportunity to take advantage of both.

Posted in Best Practices for Merchants, Credit Card Security, EMV EuroPay MasterCard Visa, Smartphone Tagged with: (POS) systems, card present, chip cards, contactless payments, Digital wallets, EMV, magnetic stripe cards, merchants, Mobile Payments, nfc technology, payments

October 22nd, 2015 by Elma Jane

Adoption of EMV technology in the U.S is important, because it provides protection against losses from counterfeit cards.

EMV, or chip cards, are the standard for secure point-of-sale (POS) transactions. Unlike magnetic stripe cards, chip cards are very difficult to counterfeit because of an embedded microchip that exchanges unique, dynamic data with a terminal each time it’s used.

To encourage the timely adoption of EMV, the leading payment networks have implemented an EMV Fraud Liability Shift that began in October 2015.

Both parties, card issuer and the merchant need to invest with EMV technology. If only one party has adopted EMV technology, the party that didn’t make the investment will be held liable.

For the card issuer, they came out with the chip cards, where all credit and debit cards have this security chips that are harder to counterfeit than magnetic strips.

For the merchant, an EMV capable terminals or POS hardware that can take advantage of the card’s security chip is needed.

With any new technology, there is a learning curve, and here are the things that you need to know.

For cardholders – with a chip card instead of swiping your card, you are going to do what is called card dipping; by inserting your card face-up and chip-first into the terminal slot. Wait and follow the terminal prompts, and only remove your card once the transaction is complete.

If you did a swipe on a chip card, an EMV-enabled terminal should prompt you to insert the card instead. If the terminal is not enabled for chip, you can still be able to swipe your card.

Employees will benefit from training – Once a merchant enables their EMV terminals, it is important to train your staff with talking points about why chip cards benefit consumers with greater security, and how they are used by helping customers with the new checkout process.

New mobile payment methods leverage both EMV and NFC, so the industry is now seeing greater interest in mobile payments among merchants and consumers.

There’s a lot of resources out there to help businesses make the transition with this EMV technology.

Posted in Best Practices for Merchants, Credit Card Security, EMV EuroPay MasterCard Visa, Near Field Communication Tagged with: card issuer, chip cards, debit cards, EMV, magnetic stripe, merchants, microchip, Mobile Payments, nfc, payment networks, point of sale, POS, terminal slot

October 19th, 2015 by Elma Jane

If you’re a merchant accepting credit cards, you’re probably aware that things are changing. As of October 1st, 2015, merchants are now liable for any fraudulent activity that occurs as a result of non-EMV-compliant. For those Merchants who haven’t yet updated their POS terminal, you need to talk with your processor to get a new equipment.

Things Merchant should know to be EMV ready:

What is EMV Chip Cards? Chip Cards are standard bank cards that are embedded with a micro-computer chip. Some may require a PIN instead of a signature to complete the transaction process. The new cards will still have magnetic stripes, at least for the time being, so you technically can continue to process payments with the same old equipment you’ve been using for years. But by refusing to upgrade your hardware, you are taking on responsibility for any fraud that might have otherwise been prevented with the new technology.

How does EMV Chip Cards Work? Instead of swiping your card, you are going to do what is called card dipping, which means inserting your card into a terminal slot and waiting for it to process.

When a Chip Card or EMV Card is dipped, data flows between the card chip and the issuing financial institution to verify the card’s legitimacy and create the unique transaction data.

This process isn’t as quick as a magnetic-stripe swipe. It will take a little longer for that transmission of data.

What Must a Merchant Do? For merchants and financial institutions, the switch to EMV chip cards means adding new in-store technology and internal processing systems, and complying with new liability rules. Merchants who have not yet purchased new POS Terminal may be held liable for fraud as of October 1st, 2015. Implementing EMV technology isn’t an option, it’s a necessity. If you are one of those in the retail business or retailers using mobile payment devices who missed the Oct. 1st deadline, you are already at risk. Upgrading should be a top priority.

Posted in Best Practices for Merchants, Credit Card Reader Terminal, Credit Card Security, EMV EuroPay MasterCard Visa, Point of Sale Tagged with: bank cards, chip cards, credit cards, data, EMV, financial institutions, magnetic stripes, merchant, mobile payment, PIN, POS terminal, processor, retail business, terminal slot