May 12th, 2016 by Elma Jane

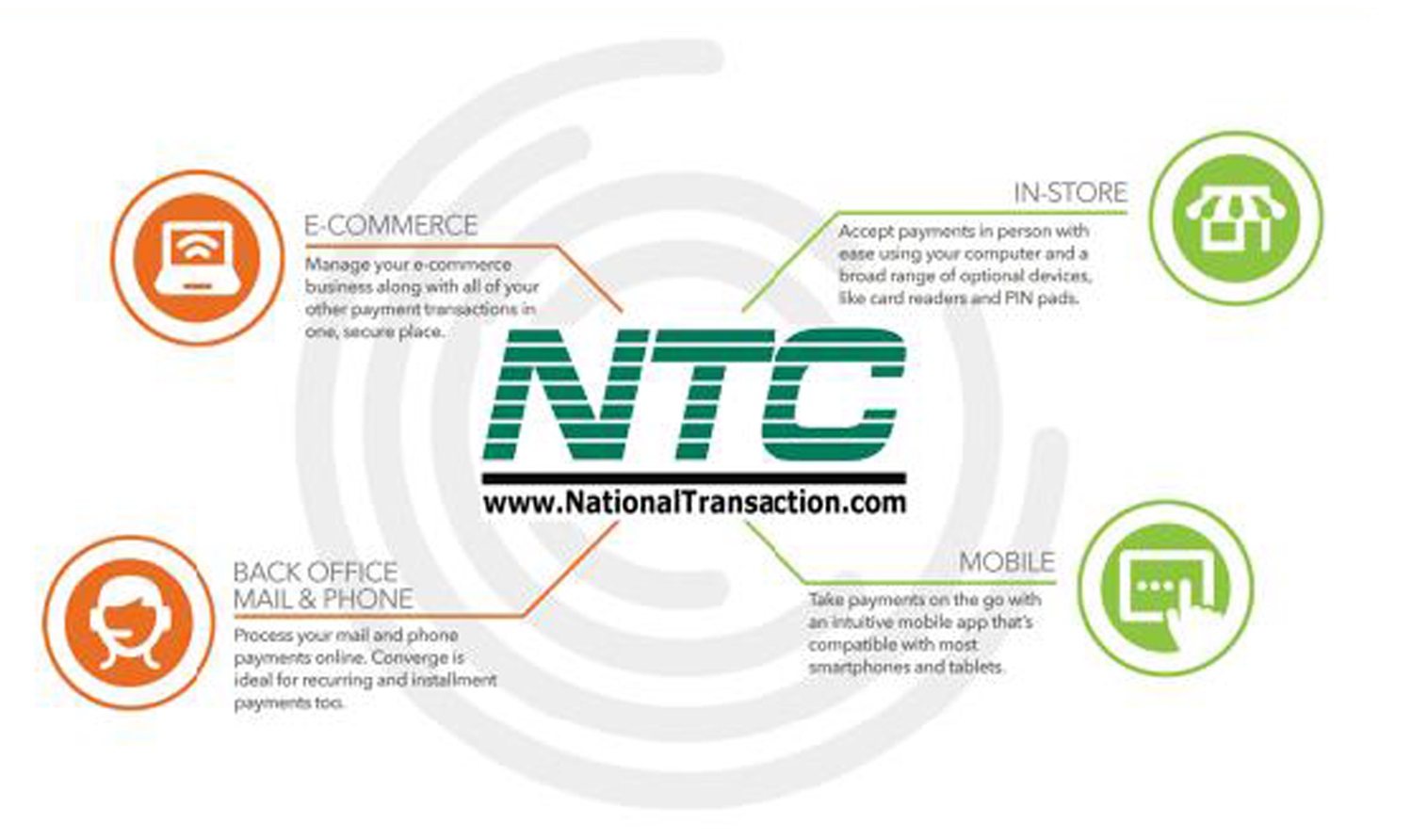

Electronic commerce (eCommerce) is a type of business transaction, that involves the transfer of information on the Internet. This allows consumers to exchange goods and services with no barriers of time or distance electronically.

Business-to-Business (B2B) this refers to electronic commerce, between businesses rather than between a business and a consumer. These transactions electronically provide competitive advantages over traditional methods. It’s faster, cheaper and more convenient.

Creating a successful online store can be difficult if you don’t have knowledge of e-commerce and what it is supposed to do for your online business.

What do you need to have an online store?

- Shopping cart – an operating system that allows consumers to buy goods and or services. Track customers, and tie together all aspects of e-commerce into one.

- Or you can check out our NTC e-Pay no shopping cart Solution.

- Taking online payment by getting a merchant account and accept credit cards through an online payment gateway.

You just need to make a better decision in choosing the right shopping cart and a merchant account for your eCommerce shop.

Posted in Best Practices for Merchants, e-commerce & m-commerce Tagged with: b2b, commerce, consumers, credit cards, customers, ecommerce, gateway, merchant, merchant account, NTC e-Pay, online, online payment, payment gateway, shopping cart, transaction

April 27th, 2016 by Elma Jane

Near field communication is a contactless communication protocol between devices like (smartphones, tablets, smartwatches or even credit cards themselves) with a nearby NFC-enabled terminal by simply authorizing your device with a passcode or fingerprint authentication.

Both merchants and customers benefit from near field communication technology, by integrating credit cards, train tickets, and coupons all into one device. Faster payment transaction times and fewer physical cards to carry around.

If your smartphone has an integrated NFC chip, you can use a mobile wallet app like Apple Pay, Android Pay and Samsung Pay for items at retailers that support NFC transactions. Just load up your credit cards on your mobile device and wave or tap your device near an NFC compatible terminal to pay, no card swiping required.

As the technology keeps growing, more NFC compatible smartphones will be available and more businesses will offer NFC card readers for customer’s convenience.

Apple Pay, integrated into the newest generation of Apple mobile devices and incorporates NFC technology. If it becomes widely used by many iPhone users, perhaps merchants will be encouraged to more quickly adopt NFC technology.

Many major banks and credit cards are supporting NFC technology, issuing new cards with embedded NFC chips. This means that you may be able to tap or wave your card at the terminal instead of swiping, no phone required, in the next few years.

Posted in Best Practices for Merchants, Near Field Communication Tagged with: cards, contactless, credit cards, customers, merchants, mobile wallet, Near Field Communication, nfc, payment, Smartphones, tablets, terminal, transaction

April 26th, 2016 by Elma Jane

The PCI-DSS is a security standard for organizations that handle branded credit cards from the major card including Visa, MasterCard, Amex, Discover, and JCB. It is designed to ensure that ALL companies that process credit card information maintain a secure environment.

PCI applies to organization or merchant, that has a Merchant ID (MID), regardless of size or number of transactions, that accepts credit card.

Merchants will fall into one of the four merchant levels based on Visa transaction volume over a 12-month period.

| Merchant Level |

Description |

| 1 |

Any merchant — regardless of acceptance channel — processing over 6M Visa transactions per year. Any merchant that Visa, at its sole discretion, determines should meet the Level 1 merchant requirements to minimize risk to the Visa system. |

| 2 |

Any merchant — regardless of acceptance channel — processing 1M to 6M Visa transactions per year. |

| 3 |

Any merchant processing 20,000 to 1M Visa e-commerce transactions per year. |

| 4 |

Any merchant processing fewer than 20,000 Visa e-commerce transactions per year, and all other merchants — regardless of acceptance channel — processing up to 1M Visa transactions per year. |

Does is each location required to validate PCI Compliance for multiple business locations?

If a business locations process under the same Tax ID, then you are only required to validate once annually for all locations.

Penalties for non-compliance

The payment brands may fine an acquiring bank $5,000 to $100,000 per month for PCI compliance violations. The banks will pass this fine along until it eventually hits the merchant. The bank will also terminate your relationship or increase transaction fees.

PCI Compliance Manager

To help you achieve and report compliance, we have Trustwave PCI Compliance Manager. It’s an online portal that enables you to understand requirements that apply to your business, and guides you through your self-assessment, step by step.

If you have any questions regarding your PCI Compliance please call our office at 888-996-2273. We would be more than happy to help.

Posted in Best Practices for Merchants, Credit Card Security, Payment Card Industry PCI Security Tagged with: banks, credit cards, merchant, PCI-DSS, Security, transactions

February 24th, 2016 by Elma Jane

Merchants can bring in new customers and encourage repeat business by using their point-of-sale terminal as a marketing tool. A point-of-sale terminal allows you to process payment and accept debit and credit cards, and generate more business by using the right tools.

Customize Receipts – a customized receipt becomes an advertisement. The customer knows where that receipt is from should they want to contact you.

Gift Cards Program – Gift card recipient are likely to spend over the face value of the card. Customers will appreciate simplified gift shopping.

Loyalty Program – Loyalty program makes customers think of your business first and encourages them to come back often to earn a reward.

Referral Rewards – Print an offer to reward referrals, so they can send people to you.

A merchant account is not just an expense by finding the right tool you can generate more income for your business!

visit www.nationaltransaction.com today, or call 888-996-2273 Extension 1

Posted in Best Practices for Merchants, Credit Card Reader Terminal, Point of Sale Tagged with: credit cards, customers, debit, gift Card, loyalty program, merchant account, merchants, payment, point of sale, terminal

January 26th, 2016 by Elma Jane

The convenience, simplicity and security of Apple Pay are now available to customers who use U.S. Bank FlexPerks American Express Cards.

U.S. Bank which is the fifth-largest bank in the nation will add TouchID biometric capabilities to its mobile app in March.

The company made the disclosure as part of a notable iOS app update released last Friday. Release appears to include, among other enhancements, improvements such as easier navigation, quicker accessibility to account information, and the ability to search transactions from previous months.

U.S. Bank Minneapolis did not give many details about how TouchID will be used within its iOS app, other than to say for fingerprint authentication for enabled devices.

Many major banks already have TouchID implemented in their mobile apps, including Citibank, Wells Fargo and Bank of America. Citibank, for example, implemented TouchID last July. Apple introduced TouchID in mid-2013.

Last week, U.S. Bank enabled for Apple Pay use the last of its debit and credit cards that had not been Apple Pay-capable. Apple Pay relies on TouchID for security and authentication.

Apple Pay is now available with the:

- U.S. Bank FlexPerks Reserve American Express Card.

- U.S. Bank FlexPerks Travel Rewards American Express Card.

- U.S. Bank FlexPerks Select+ American Express Card.

Posted in Best Practices for Merchants Tagged with: account, bank, biometric, cards, credit cards, customers, debit, mobile, mobile app, Security, transactions

December 7th, 2015 by Elma Jane

Most payments will probably be made with apps in phones or smartwatches in less than a decade from now, using NFC, biometrics or other mechanisms that don’t involve swiping or using plastic cards.

If your mobile device has an integrated NFC chip, you can use a mobile wallet app like Apple Pay and Android Pay to pay for items that support NFC transactions at a retail store. Simply wave your device near an NFC compatible terminal to pay, no card swiping required.

Both Apple Pay and Android Pay have fingerprint scanners on phones, you can enable payments with just a fingerprint scan.

In some countries, it’s easy for consumers to get credit cards with imbedded NFC chips. This means that you may be able to wave your card at the terminal instead of swiping, no phone required. In America, though, because NFC hasn’t caught on until recently, analysts expect that NFC via smartphone and smartwatch services such as Apple Pay and Android Pay will dominate contactless transactions in the next few years.

Just as credit cards replaced cash, credit cards will be replaced by digital payments which will continue to rely on the credit infrastructure but will obscure the plastic card itself.

As consumers, we love to see better products. When it comes to payments, we need Standards and Reliability.

Posted in Best Practices for Merchants, Mobile Payments, Mobile Point of Sale, Near Field Communication, Smartphone Tagged with: biometrics, cards, contactless transactions, credit cards, digital payments, mobile wallet, nfc, NFC chip, payments, smartphone, terminal

November 19th, 2015 by Elma Jane

The Ingenico iCMP PIN pad is now available with Converge in the US! This EMV-enabled device is flexible to use with a USB connection and Converge or with a Bluetooth connection and Converge Mobile (launching soon!).

Key features of the Ingenico iCMP include:

Chip, Contactless and Mag Stripe

Accept EMV chip cards, including Chip & Pin and Chip & Signature as well as mag stripe cards and contactless payments – mobile wallets like Apple Pay and contactless cards. The EMV-capabilities of the PIN pad help protect our customers from counterfeit card fraud.

Debit and Credit PIN Based Transactions

Accept debit and credit cards using PIN capabilities on the device. This is important to help further protect our customers from lost, stolen and NRI (not received/issued) fraud.

Encryption

Encrypted to keep card data separate and away from the mobile app/device and safe as it travels through the payment network.

Bluetooth or USB

Connect with a USB connection when using a computer and Converge www.convergepay.com or Bluetooth when using with the upcoming Converge Mobile app.

Pocket size

Takes up little space on a countertop, and it’s easy to carry when on the go.

Give us a call now at 888-996-2273.

Posted in Best Practices for Merchants Tagged with: Apple Pay, card data, Chip & PIN, Chip & Signature, chip cards, contactless cards, contactless payments, Converge, Converge Mobile, credit cards, Debit and Credit, EMV, encryption, ingenico, mag stripe, mobile wallets, payment network, transactions

October 19th, 2015 by Elma Jane

If you’re a merchant accepting credit cards, you’re probably aware that things are changing. As of October 1st, 2015, merchants are now liable for any fraudulent activity that occurs as a result of non-EMV-compliant. For those Merchants who haven’t yet updated their POS terminal, you need to talk with your processor to get a new equipment.

Things Merchant should know to be EMV ready:

What is EMV Chip Cards? Chip Cards are standard bank cards that are embedded with a micro-computer chip. Some may require a PIN instead of a signature to complete the transaction process. The new cards will still have magnetic stripes, at least for the time being, so you technically can continue to process payments with the same old equipment you’ve been using for years. But by refusing to upgrade your hardware, you are taking on responsibility for any fraud that might have otherwise been prevented with the new technology.

How does EMV Chip Cards Work? Instead of swiping your card, you are going to do what is called card dipping, which means inserting your card into a terminal slot and waiting for it to process.

When a Chip Card or EMV Card is dipped, data flows between the card chip and the issuing financial institution to verify the card’s legitimacy and create the unique transaction data.

This process isn’t as quick as a magnetic-stripe swipe. It will take a little longer for that transmission of data.

What Must a Merchant Do? For merchants and financial institutions, the switch to EMV chip cards means adding new in-store technology and internal processing systems, and complying with new liability rules. Merchants who have not yet purchased new POS Terminal may be held liable for fraud as of October 1st, 2015. Implementing EMV technology isn’t an option, it’s a necessity. If you are one of those in the retail business or retailers using mobile payment devices who missed the Oct. 1st deadline, you are already at risk. Upgrading should be a top priority.

Posted in Best Practices for Merchants, Credit Card Reader Terminal, Credit Card Security, EMV EuroPay MasterCard Visa, Point of Sale Tagged with: bank cards, chip cards, credit cards, data, EMV, financial institutions, magnetic stripes, merchant, mobile payment, PIN, POS terminal, processor, retail business, terminal slot

October 8th, 2015 by Elma Jane

Rules have changed in regards to swiping credit cards October 1st, 2015 with the EMV Liability Shift; which may not cause much concern for most consumers, but for merchants.

EMV compliance isn’t a legal requirement. However, if you’re a merchant that accepts credit cards in-person, then you need to find out whether you’re meeting the EMV Standard. The new rule for the liability shift applies October 1st, regardless of the size or type of business.

What Is EMV Standard?

EMV stands for EuroPay, MasterCard, and Visa, the three companies that originally created the standard.

The EMV Shift is to provide enhanced security and prevent fraudulent activity with credit cards. Updated equipment is also necessary for processing the new computerized cards, and unfortunately, the responsibility of securing up-to-date hardware falls on the merchant.

Since card evolves more instead of cash in our society, fraud and data breaches is on the increase, and now a common occurrence. Adapting new technology is therefore necessary. A hassle for many merchants, but there are actually benefits from all parties involved in a credit card transaction.

Data shows that fraud decreases dramatically when EMV Standards are implemented In Europe. The region has experienced an 80% reduction in credit card fraud, while the USA has seen a 47% increase by NOT implementing EMV standards.

The new liability rules took effect on October 1st in the US, and any party that has not yet implemented EMV-compliant machines might now be liable for fraud committed with counterfeit chip cards. Note that this liability shift only applies to in-person transactions. Phone order and web order transactions will be dealt with as they always were.

For Merchants, it means you’ll eventually need to get new equipment for processing credit cards payments in-person (unless you’ve already done so not too long ago, as nearly all POS terminals sold in the USA nowadays are EMV compliant). For most business owners, it’s a good idea to implement the new system sooner rather than later.

Step to take as a Merchant Until you get your EMV equipment

- Ask for an official ID from customers whose credit card you process.

- Conduct some research to see which EMV system would be best for your business.

- Start shopping around for new payment processing options that are EMV compliant.

If you already have a machine that can process chip cards, you’re fully EMV-compliant.

If you don’t accept any in-person payments, then you’re all set.

If you do accept in-person payments and you do not have a chip card machine, chances are you’ll be fine for a little while. But those of you with a high risk of encountering a fake card (if you are a high-volume business with a large average ticket, for instance) should probably upgrade soon.

Fraudsters are going to be taking advantage of businesses that haven’t upgraded so it’s a great time to switch!

Check out NTC’s EMV/NFC Capable Terminal!

Posted in Best Practices for Merchants, Credit Card Reader Terminal, Credit Card Security, EMV EuroPay MasterCard Visa, Point of Sale Tagged with: chip cards, credit card transaction, credit cards, credit cards payments, EMV, EMV equipment, EuroPay, high risk, MasterCard, merchants, nfc, payment processing, POS terminals, visa

October 6th, 2015 by Elma Jane

If you accept credit cards and don’t know what EMV is here is what you need to know.

EMV stands for Europay, MasterCard and Visa. A credit card that had a chip embedded in it is an EMV. EMV Cards have been standard in Europe for more than 10 years because they’re more secure than magnetic stripe cards. Magnetic stripe cards doesn’t change, it has static data, which makes them easy to clone. The chip embedded card makes it more difficult and costly to counterfeit because the data that is transmitted changes each time the card is read. This means less fraud.

Liability Shift rules set by Visa and MasterCard as of October 1st. The liability for fraud carried out in physical stores with counterfeit cards belongs to the merchant if it has not yet upgraded its POS system to accept EMV-enabled chip cards.

- Calculate your risk – Consider the cost of replacing your point-of-sale (POS) terminal vs. potential risk. Whether you replace it now or at a later time, eventually all businesses will have to replace their POS terminals.

- Educate your staff – Educated employees translate to better-educated customers. Merchants can help customers better understand this change and what it means for them.

- Upgrade your POS system – Consider using an EMV compliant credit-card reader on a wireless device for an ultra-secure mobile solution. This is also a chance to upgrade other options, such as near field communication NFC technology, which lets consumers use their mobile devices to make payments at the point of sale.

National Transaction Terminals with EMV and NFC (near field communication) Capability To accept Apple Pay, Android Pay and other NFC Transactions at your business. You will need to adopt point-of-sale devices with NFC/contactless readers.

National Transaction offer a range of options to suite your specific needs.

If you’re using Virtual Merchant Mobile now called Converge please contact our office at 888-996-2273 to know your options.

Posted in Best Practices for Merchants, Credit Card Reader Terminal, Credit Card Security, EMV EuroPay MasterCard Visa Tagged with: Android Pay, Apple Pay, chip cards, contactless readers, Converge, credit cards, EMV, EuroPay, magnetic stripe, MasterCard, merchants, Near Field Communication, nfc, payments, POS, terminal, Virtual Merchant Mobile, visa