October 11th, 2016 by Elma Jane

Cybersecurity via Converge:

Converge uses a multi-layered approach to security which helps keep cardholder data safe throughout the entire payment process; from beginning to end.

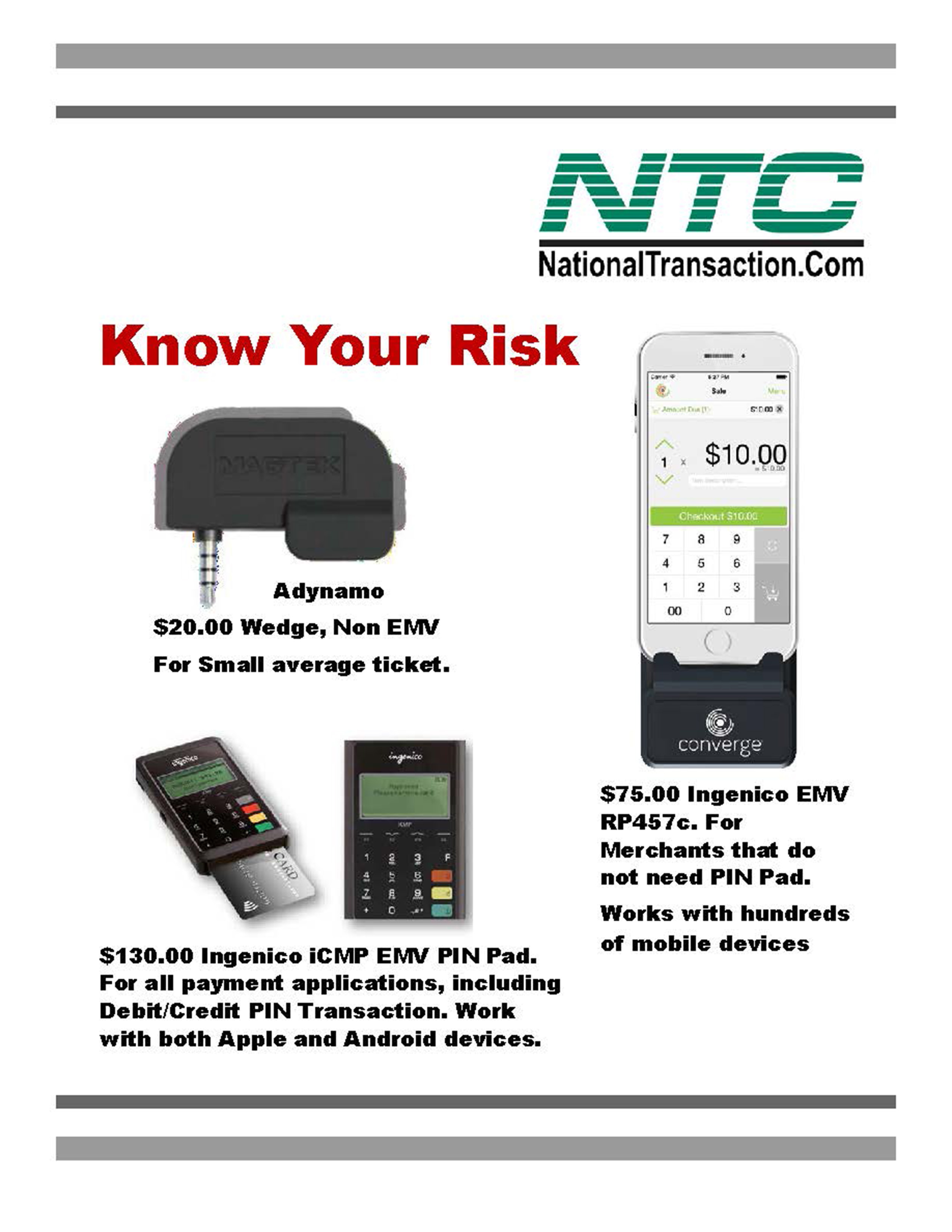

- EMV: All new Ingenico PIN pads and readers – iCMP and RP457c used with Converge Mobile offer EMV to help protect against counterfeit card use. The PIN pads go a step further in helping protect against lost; stolen and NRI (never received/issued) when a PIN-preferred card is accepted with PIN entry.

- Encryption: All new Ingenico devices also include encryption as a standard security component in addition to protect card data in transit.

- Tokenization: An enhanced security feature that is particularly valuable in card-not-present (CNP) environments when cards are stored on file for processing at a later time, or either for recurring/installment payments.

Get the Ingenico iCMP EMV PIN Pad for only $130.00.

For all payment applications, either Debit or Credit PIN Transaction. Work with both Apple and Android Devices.

Ingenico EMV RP457c card reader for only $75.00.

For Merchants that do not need PIN Pad. Works with hundreds of mobile devices.

Posted in Best Practices for Merchants, Credit Card Security, EMV EuroPay MasterCard Visa, Mobile Payments, Smartphone Tagged with: card, card-not-present, cardholder, data, EMV, mobile, payment, PIN pads, Security, tokenization

September 21st, 2016 by Elma Jane

PCI compliance applies to any company, organization or merchant of any size or transaction volume that either accepts, stores or transmits cardholder data.

Any merchant accepting payments directly from the customer via credit or debit card must be Compliant. The merchant themselves are therefore responsible for becoming Compliant, as the deadline for the merchant becomes overdue.

Understanding and knowing the details of Payment Card Industry Compliance can help you better prepare your business. Because failing and waiting to become compliant or ignoring them, could end up being an expensive mistake.

The VISA regulations have to adhere to the PCI standard forms as part of the operating regulations. The regulations signed when you open an account at the bank. The rules under which merchants are allowed to operate merchant accounts.

The Payment Card Industry Data Security Standard (PCI DSS) is a proprietary information security standard for organizations that handle branded credit cards from the major card schemes including Visa, MasterCard, American Express, Discover, and JCB.

Posted in Best Practices for Merchants, Credit Card Security, Payment Card Industry PCI Security, Visa MasterCard American Express Tagged with: American Express, cardholder, compliance, credit, customer, data, debit card, Discover, jcb, MasterCard, merchant, Payment Card Industry, payments, PCI, transaction, visa

September 16th, 2016 by Elma Jane

National Transaction offer valuable features and benefits, if you want to improve your business’s productivity, you should look for the following features below, that you need from your Electronic Payments provider.

Advanced Security Options – 6 out of 10 small businesses close within six months of a card data breach, it is important that Point-of-Sale devices should have appropriate security measures, particularly EMV, encryption and tokenization. NTC offer Safe-T for Small and Medium Businesses and Safe-T for Large Businesses. The Top-tier security is important on your business’s data especially customer information, consider adding additional authentication procedures.

Fast Payment Processing – first step is having up-to-date technology, because some customers might leave, the sooner you have the money processed by your provider, the bigger and stronger your business can become. NTC is adept at administering payments quickly and efficiently. We can provide regular funding or next day funding.

Feature Flexibility – obtaining the features you need from your payment services provider is very important. Look for a provider that appropriately addresses your payment concerns.

Mobile Payment Processing – NTC offer Virtual Merchant/Converge Mobile that gives you the ability to accept payments using your smartphone or tablet anywhere you go. Furthermore, the app works with most Apple and Android mobile devices. Accept a key-entered transactions or swipe cards using an encryption reader. You can now take chip card payments using Ingenico iCMP PIN Pad or the new RP457c card reader.

Reliable Customer Support – NTC is available 24/7, the phones are answered by humans and not automated systems. You got support with your hardware, answer questions and guide you to better understand the process. Customer support is the most important feature of any business partnership you make. At NTC we are very passionate about that.

Up-to-Date Tech – futuristic features, like mobile payment abilities, EMV/NFC, contactless payments are worth investing. Modern consumers are generally more familiar with up-to-date payment systems. Seeing a payment service provider offer a swipe-only terminal should be a red flag, because the recent regulations require merchants to have EMV to provide better data security.

Posted in Best Practices for Merchants, Credit Card Security, Electronic Payments, EMV EuroPay MasterCard Visa, Mobile Payments, Mobile Point of Sale, Near Field Communication, Point of Sale, Smartphone Tagged with: Breach, card data, card reader, chip card, contactless payments, data, EMV, encryption, merchants, mobile, mobile payment, nfc, payments, Payments provider, point of sale, provider, Security, service provider, smartphone, swipe, tablet, terminal, tokenization, transactions

September 15th, 2016 by Elma Jane

Storing credit card data for recurring billing are discouraged.

But many feels storing is necessary in order to facilitate recurring payments.

Using a third party vault provider to store credit card data for recurring billing is the best way.

It helps reduce or eliminate the need for electronically stored cardholder data while still maintaining current business processes.

For recurring billing a token can be use, by utilizing a vault. The risk is removed from your possession.

Modern payment gateways allow card tokenization.

Any business that storing data needs to review and follow PCI DSS requirement in order for the electronic storage of cardholder data to be PCI compliant.

On the primary account number, an appropriate encryption will be applied. In this situation, the numbers in the electronic file should be encrypted either at the column level, file level or disk level.

Posted in Best Practices for Merchants, Credit Card Security Tagged with: billing, cardholder, credit card, data, payment gateways, payments, PCI, recurring, token, tokenization

August 9th, 2016 by Elma Jane

Businesses are discouraged from storing credit card data, but many feel the practice is necessary in order to facilitate recurring payments. Merchants that need to store credit card data are doing it for recurring billing.

Using a third party vault provider is the best way to store credit card data for recurring billing, it helps reduce or eliminate the need for electronically stored cardholder data while still maintaining current business processes. The risk of storing card data is removed from your possession and you are given back a token that can be used for the purpose of recurring billing, by utilizing a vault. Modern payment gateways allow card tokenization.

Any business that storing data via hard copy needs to review and follow PCI DSS requirement in order for the electronic storage of cardholder data to be PCI compliant. Appropriate encryption must be applied to the PAN (primary account number). In this situation, the numbers in the electronic file should be encrypted either at the column level, file level or disk level.

Posted in Best Practices for Merchants, Payment Card Industry PCI Security, Travel Agency Agents Tagged with: cardholder, credit card, data, merchants, payment gateways, payments, PCI, provider, tokenization

July 14th, 2016 by Elma Jane

PCI Compliance applies to every merchant who is accepting credit cards large or small. Refusing or delaying to become PCI Compliant can end up being a costly mistake.

If you accept any credit or debit card payment, you need to be PCI Compliant no matter the volume is.

PCI applies to any company, organization or merchant of any size or transaction volume that accepts, stores or transmits cardholder data. Any merchant accepting payments directly from the customer via credit or debit card must be PCI Compliant.

The merchant themselves are responsible for becoming PCI Compliant, as the deadline for merchants to become Compliant is long overdue

Understanding and knowing the details of PCI Compliance can help you better prepare your business. Failing and waiting to become compliant or ignoring them, could end up being an expensive mistake.

The VISA regulations have to adhere to the PCI standard forms part of the operating regulations, the regulations signed when you open an account at the bank. The rules under which merchants are allowed to operate merchant accounts.

Posted in Best Practices for Merchants, Travel Agency Agents Tagged with: cardholder, credit cards, customer, data, debit card, merchant, payment, PCI Compliance, transaction

June 22nd, 2016 by Elma Jane

What is ARC, IATA, and CLIA? what’s the difference? What it does and what type of agents would benefit most from it.

CLIA Number – is issued by the Cruise Lines International Association. It’s a way for vendors to identify you as a travel agent. It serves the same purpose as the ARC or IATA number, it’s just issued by another organization and has different barriers to entry and costs associated with it. CLIA agencies without ARC accreditation cannot issue airline tickets since CLIA numbers were designed specifically for cruise-focused travel agencies. You can always go under an umbrella organization like a host agency, you don’t need to get your own CLIA number if you’re working with a host agency. You can use their identification number and won’t incur the costs associated with obtaining your own CLIA number. While CLIA is accepted nearly everywhere, it’s NOT accepted by the airlines. If you are not issuing airline tickets, CLIA is a practical option.

CLIA vs. ARC/IATA Number – If you’re ticketing air-only reservation, ARC and IATA are must-haves.

ARC (Airlines Reporting Corporation) – gives out these ARC numbers to accredited agencies, which allows travel agencies to issue airline tickets. The use of an ARC number extends from a hotel to a cruise ship booking not only air tickets for travel agencies. For a home-based travel agent or a storefront agency that only books leisure travel (no air), having your own ARC number is too much.

IATA – International Air Transport Association Network (IATAN) use extensive data resource to connect the suppliers to the U.S. travel distribution network. IATAN ID card holders get promotional benefits and concessionary incentives from suppliers (participating members) who identify the agent with an IATA/IATAN number as a valid associate, in addition to approving travel agents for the sale of travel tickets. IATA certifies a referral agent or an affiliate travel agent to find clients for the hosting travel agency’s business needs as well.

Posted in Best Practices for Merchants, Travel Agency Agents Tagged with: agents, card, data, host agency, travel agent, vendors

June 7th, 2016 by Elma Jane

Merchants need to stay competitive by offering the most modern forms of electronic payment processing technology to satisfy customers, because, in today’s world of smartphones and one-the-go payments, consumers have options in how they conduct their transactions. With proper education on the types of payment options, merchants can make the right decision for their business.

NTC is here to discuss that payment options.

EMV – or Europay, MasterCard, Visa is a fraud-reducing technology to protect card issuers, merchants, and consumers from counterfeit or stolen cards. The customer inserts or dips the chip card into the EMV terminal, rather than swiping the card at the point of sale. A one-time-use code is created for that transaction. This code makes it virtually impossible for anyone to duplicate, leaving customers safer from fraud.

NFC – stands for near field communication is a method of contactless data exchange between two electronic devices. NFC is used in mobile wallets such as Apple Pay, Android Pay, and Samsung Pay. More and more consumers leaning towards mobile wallets, merchants should be prepared to accept NFC payments by incorporating NFC-enabled equipment.

Virtual Merchant Mobile Payments – Mobile Payments are popular, you can take payments anywhere. Ideal for retail, restaurant and service businesses of any size. Accept payments your way online, in-store and on the go. Anytime and anywhere.

Offers flexibility you want with the payment security you and your customer need:

- Accept credit and debit cards, including mag stripe, chip cards, and contactless payments/NFC, like Apple Pay and other mobile wallets.

- Calculate discounts, taxes, and tips automatically.

- Email customer receipts.

- Help protect cardholder data with an encrypted, chip card device.

- Record cash transactions.

- Use your own smartphone or tablet (works with most IOS and Android mobile devices).

Check out NTC’s electronic payment solutions that are EMV-capable, NFC-enabled and mobile wallet ready.

Posted in Best Practices for Merchants, Electronic Payments, EMV EuroPay MasterCard Visa, Mobile Point of Sale, Near Field Communication, Point of Sale, Smartphone, Travel Agency Agents Tagged with: chip card, consumers, contactless payments, customers, data, debit cards, electronic payment, EMV, fraud, merchants, mobile wallets, Near Field Communication, nfc, online, payment, payment processing, point of sale, Security, Smartphones, terminal, transactions

May 26th, 2016 by Elma Jane

NFC stands for Near Field Communication. It is a technology that allows contactless data exchange between two electronic devices

Contactless Payment is a description for the ability to pay without touching anything.

How do mobile wallets fit into NFC?

Mobile wallets like Apple and Android Pay use NFC technology. NFC technology allows the data to securely pass back and forth between each device to make a contactless payment.

How secure are NFC Payments?

Tokenization converts or replaces cardholder data with a unique token ID. This eliminates the possibility of having card data stolen. These tokens help heighten protection and security for the consumer.

As a merchant, preparing to accept payments that meet customers satisfaction is needed. With the mobile wallet transaction process, it makes the traditional transaction quick and efficient.

NTC terminals allow merchants to accept NFC Payments, allowing you to process more transactions. For more information give us a call at 888-996-2273.

Posted in Best Practices for Merchants, Credit Card Security, Mobile Point of Sale, Near Field Communication, Smartphone Tagged with: cardholder, consumer, contactless, customers, data, merchant, mobile wallets, Near Field Communication, nfc, payment, Security, terminals, tokenization, transaction

May 23rd, 2016 by Elma Jane

Today, the information thieves want most from your customers is not their credit card numbers but their email addresses and account passwords. Criminals used stolen credentials to gain control of consumer accounts and open new accounts using their names to defraud merchants.

Data encryption and payment security are crucial for merchants, but so is helping customers keep their credentials secure. Encouraging customers to keep their information secure is a good thing.

Help customers practice good password habits – set up your system to require good passwords. Have account rules in place that require more secure passwords. ( a minimum number of characters and a mix of character types).

Remind customers what they can expect from your business – like your employee will never ask for customer account passwords or payment account information via email or no one from your company will call to ask for account passwords or credit-card information.

Offer security tips ahead of peak season – by reminding them ahead of time about account safety. Your business may receive a high volume of travel booking which means peak time for fraud attempts that need to be screened for fraud.

Keep your own fraud-prevention program updated – fraud prevention is an ongoing cost of doing business for merchants, but it doesn’t have to be too much expense. Working with your customers to keep their data and yours secure, will strengthen your business with them while protecting your business from fraud.

Posted in Best Practices for Merchants, Travel Agency Agents Tagged with: credit card, customers, data, fraud, merchants, payment, payment security, Security, travel