September 22nd, 2014 by Elma Jane

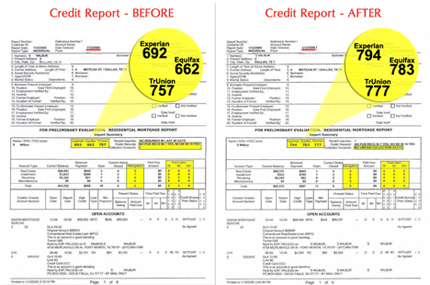

Consumers know how hard it is to obtain a credit card, if your credit score isn’t up to par. A bad credit score can prevent you from getting credit and make it hard to purchase your day to day necessities. People with poor credit don’t know their options. There are a number of ways to get a credit card if you have a poor credit score. There will likely be road blocks and limitations in your search. You won’t have the same options available as someone with pristine credit. But you will be able to get a line of credit if you look in the right place.

COSIGNED CREDIT CARDS If you get a cosigner, you will be able to obtain a card that would not be available to you otherwise. The cosigner has to have good credit, and they are responsible for your debt if you can’t pay. Make sure your cosigner fully recognizes their obligations and what will happen if you are unable to pay.

GIVE AN EXPLANATION FOR POOR CREDIT Explain the circumstances behind your poor credit. You can add a 100-word statement to your credit report such as the loss of a job. If you can tell your story and convince creditors you are on the road to increasing your credit score, they may believe you are more likely to pay back your debts. Divorce and illness are two other instances where individuals may see a drop in their credit score. Make sure whatever you list is true.

IMPROVE YOUR CREDIT One of the most difficult options. Poor credit can seem extremely hard to repair. But there are choices, it is just a process that will take a significant period of time. If you have poor credit, you can open bank accounts and pay off your loans and credit cards on time. If you pay off your debt in a timely manner, your credit score will improve over time and you will gain access to more credit card options.

RETAIL STORE CARDS Retail stores often have store credit cards they offer customers. Retail stores are generally more willing to approve applicants without a stellar credit score. But these cards usually come with extremely high interest rates and relatively low credit limits, so make sure you fully understand the terms of the card before applying.

SECURED CREDIT CARDS You deposit some money into an account, and then a creditor will provide you with a line of credit equal to your deposit. It is essentially a down payment, and if you don’t pay your credit card bill, your creditor is entitled to the money in the account. This might not sound like a favorable position, but remember that secured credit cards can be used as a valuable tool to rebuild your credit. Make sure the card you apply for reports to a credit reporting agency. This will help you start building a credit history. SELECT A CREDIT

CARD DESIGNED FOR THOSE WITH POOR CREDIT There are a number of credit cards offered by Visa and MasterCard designed for people with poor credit. These cards have low limits, a significant number of fees and high interest rates. But for some people, it may be their best option. Talk to your bank’s administrators or with your current credit card company to see if they offer a credit card that fits your personal needs.

SUBPRIME CREDIT CARDS Another option for those with poor credit, but they are ripe with fees that many people who are already short on cash may not be able to handle. Interest rates can be dangerously high for those with poor credit, so beware of these cards. They are often a last resort for individuals who need access to credit. However, like secured credit cards, they can be used to rebuild credit. Make sure you read the fine print and understand the applicable fees before you apply for a subprime credit card. Again, make sure the card reports to a credit reporting agency so you start building a credit history. Finding a line of credit doesn’t have to be a difficult endeavor. If you know what you are looking for, you can find a line of credit that fits your personal needs without breaking the bank. There are limitations, as well as pros and cons, to many of the forms of credit available to those with poor credit scores, such as secured credit cards or subprime credit cards. But those options do give people choices they otherwise may not have, and they help you build credit, so that eventually you will have a greater number of options.

Posted in Best Practices for Merchants Tagged with: account, applicants, card, consumers, COSIGNED CREDIT CARDS, credit, credit card bill, credit history, credit limits, credit report, credit score, credit-card, creditor, customers, deposit, down payment, good credit, interest rates, low credit limits, MasterCard, payment, poor credit, RETAIL STORE CARDS, retail stores, SECURED CREDIT CARDS, store credit cards, SUBPRIME CREDIT CARDS, visa, Visa and MasterCard

August 29th, 2014 by Elma Jane

High risk credit card processing is electronic payment processing for businesses deemed as HIGH RISK by the MERCHANT SERVICES INDUSTRY

The high risk segment of payment processing has become more important as banks and ISO’s have begun to tighten up their credit restrictions and underwriting policies. Businesses are classified as high risk primarily because of their product or service and the way they go to market. In merchant services, risk is related to CHARGEBACKS or customer disputes.

The more likely a business to have chargebacks, the higher risk the business. For instance, online businesses selling a weight loss product through a free trial offer, is more likely to have chargebacks than a retail store selling the same weight loss product.

Merchants are often unaware their business falls into the high risk category when they first start shopping for a merchant account. Getting a high risk merchant account can be difficult.

These providers have more stringent requirements and the application process is longer compared to traditional merchant account providers.

High risk businesses should expect to pay higher rates and fees for payment processing services. As a general rule of thumb, merchants should count on paying at least more than a traditional merchant account. Most high risk merchant accounts also require a contract of at least 18 months, whereas low risk providers offer accounts without cancellation fees or contracts.

ROLLING RESERVES are also a big part of high risk credit card processing. Most high risk merchants have some sort of rolling reserve placed on the account, especially new accounts without any processing history. A Reserve refers to an account where a percentage of the funds from transactions are held in reserve to cover against any chargebacks or fees that the processor may not be able to collect from the merchant. This is similar to a security deposit, but merchants don’t have to pay it up front. Reserves are a pain point for many small high risk merchants, but they are definitely necessary and without them, processors would not accept any high risk merchants at all.

What Businesses Are High Risk?

As mentioned earlier, businesses are usually classified as high risk due to the product or service they offer, however merchants with severely damaged credit or a recent bankruptcy can also be considered high risk. Below are just of the few common high risk merchant categories:

Adult Websites

Cigars & Pipe Tobacco Online

Collection Agencies

Credit Repair

Debt Consolidation

E-Books & Software

Electronic Cigarettes

Firearms – Online

High Ticket & High Volume

Medical Marijuana Dispensaries

Multi Level Marketing & Business Opportunities

Nutraceuticals like weight loss supplements, cleansers etc.

Penny Auctions

Sports Betting Advice

Ticket Brokers – Online Tickets

TMF Merchants

Travel & Timeshare

Unfortunately this list is growing and some credit card processing companies even classify any start up Internet business, that doesn’t have extensive financials to be high risk. With the recent economic recession in the United States, there has been an increase in these start up Internet ventures. People are either looking to supplement their income or start their own business instead of looking for work.

How To Protect Your Business

Accepting credit cards is the single most important part of most online businesses. Unfortunately, many successful businesses go under after having their merchant account shut down. High risk merchants should always be cognizant of their merchant account and pay attention to chargeback percentages. Below are some tips for high risk merchants looking for payment processing solutions.

Be Upfront: Make sure your processor knows exactly what you sell and how you market the product/service. If they don’t accept your business type, keep shopping for a new merchant account provider. Many merchants will try to fly under the radar by not revealing all their products or fully disclose their marketing methods to the processor. This is a bad move, the processor will eventually find out the details about your business. This is usually from doing an audit on your transactions and contacting your customers.

Negotiate Every 3 Months: Credit card processing companies underwrite applications based on previous processing history. If there is no previous history, the account is riskier and the terms offered are usually more expensive and restrictive. You can always re-negotiate your rates, reserves and other contract terms with your current processor. Once they have 3 months of history to evaluate, they may be able to offer you a better deal. Three months of history is the magic number for most processors. If you applied without the previous history and were declined, there is a chance the same processor will approve your application if you provide 3 months of previous statements.

Prepare For The Worst: All high risk merchants should keep at least 2 active merchant accounts, from different providers. You never know when underwriting guidelines might change, or you may have an influx of chargebacks. Having a backup account or even multiple back up accounts is a good idea. Many high risk providers offer a load balancing gateway, which allows for multiple merchant accounts to be integrated into one payment gateway. This way you can spread transactions across multiple accounts, through one shopping cart/gateway.

Posted in Best Practices for Merchants Tagged with: account, account providers, accounts, banks, card, chargebacks, contract, credit, credit card processing, credit restrictions, customer, customers, deposit, electronic payment, fees, financials, gateway, High risk credit card, High Ticket & High Volume, ISOs, low risk, marketing, merchant, merchant account, merchant services, multiple accounts, payment gateway, payment processing, processing services, processing solutions, processor, product, Rates, reserves, retail store, risk, ROLLING RESERVES, Security, security deposit, service, shopping cart, statements, terms, TMF Merchants, transactions, travel, underwriting

August 7th, 2014 by Elma Jane

Using Transfer by Facebook, the user can transfer money after logging into their Rakuten Bank account from the Rakuten Bank app, selecting the person they wish to send money to from their list of Facebook friends in the app, and inputting the amount they wish to transfer.The fee-free transfer process can be completed on the app without any of the recipient’s account information and include a 50 character message to accompany the transaction. Money can also be transferred to non-Rakuten Bank account holders, for a fee of Y165. By accessing a URL on Facebook with the transfer notice, the recipient is able to specify a bank account for the money and complete the deposit.

Posted in Financial Services Tagged with: account holders, account information, app, bank account, Bank app, deposit, Facebook, free transfer process, transaction, transfer notice, URL

August 4th, 2014 by Elma Jane

Run through a non-profit organisation, Stellar is a decentralized protocol for sending and receiving money in any pair of currencies, be they dollar, yen or bitcoin. The system works through the concept of gateways that let people get in and out of the network. Users hold a balance with a gateway, which is any network participant that they trust to accept a deposit in exchange for credit on the network. To cash out, a user invokes the promise represented by a gateway’s credits, returning them in exchange for the corresponding currency.

Like Ripple, Stellar comes with its own built-in digital currency, which will be given away for free to people who sign up via Facebook, to nonprofits and to current bitcoin and Ripple holders. Initially there will be 100 billion ‘stellars’ (five per cent of which will be kept back to fund the nonprofit) with the supply increasing at one per cent a year. Although stellars will have a market-determined value, their main purpose will be to provide a conversion path between other currencies. This means that when two parties exchange money through the distributed exchange, stellars sit in the middle. Example, a user might submit a transaction which converts EUR credits to stellar and then converts those stellar to AUD credits. Ultimately, the user will have sent EUR, the recipient will have received AUD, and two exchange orders will have been fulfilled.

Developers are being invited to jump in and work with the open-source code and build applications on top of Stellar. The project has secured the backing of payment industry darling Stripe, which has handed over $3 million in exchange for two per cent of stellars. Stellar is highly experimental, but it’s important to invest effort in basic infrastructure when the opportunity arises. Stellar could become a much better substrate for a lot of the world’s financial systems.

Posted in Internet Payment Gateway Tagged with: AUD credits, bitcoin, code, credit, credits, currencies, deposit, digital currency, EUR credits, Facebook, gateways, network, payment industry, transaction

December 5th, 2013 by Elma Jane

Recently, Consumer Reports reviewed 26 different prepaid cards and evaluated them based on different factors. The cards Consumer Reports considered to be the best scored well in each of these four factors:

- Clarity of Fees — How well the fees are disclosed.

- Convenience — Availability of in-network ATMs, bill pay features and how widely the card network brand is accepted.

- Safety — Whether funds are protected with FDIC deposit insurance.

- Value — How much they cost to use.

This is the first time Consumer Reports has evaluated and ranked prepaid cards, revealing a shift in the market for prepaid. As prepaid cards continue to grow in popularity, consumers are going to become savvier about which prepaid cards they purchase. Consider taking a closer look at this Consumer Report to determine how your financial institution’s (FI’s) prepaid offering measures up.

Highest ranked cards are those like the ATIRA suite of prepaid cards TMG’s clients issue. They have fewer fees and make it easier for consumers to avoid them, carry FDIC insurance for each cardholder, offer features comparable to traditional checking accounts and do a better job of disclosing fees.

Not surprisingly, the worst prepaid cards reviewed scored poorly in at least one, and sometimes several, of the above categories. All of the lowest ranked cards have high, unavoidable fees, including activation and monthly fees. Additionally, the lower scoring cards fail to make their fees clear and easy for consumers to access and understand.

Specifically, the report found some prepaid cards fail to provide clear explanations of how to use features such as electronic payments, text alerts and mobile remote deposit capture, and the fees that may be charged for them. Further, while all of the cards reviewed claim to offer some form of protection for consumers, the report found in these policies are often not clearly defined.

Consumer Reports also found it problematic that although issuers provide safeguards voluntarily, they can cancel them at any time. Additionally, according to the report, fee information is often hard to find and difficult to understand. The report states this problem is compounded by the lack of consistency with fee names and descriptions” from card to card, making it challenging for consumers to compare fees and costs. Consumer Reports also found that prepaid cards offered by some of the big banks are not necessarily less expensive than other prepaid cards. Also, these big bank offerings may be less attractive to consumers because they often don’t provide the option of making both electronic payments and payment by paper check.

Posted in Credit card Processing, Financial Services Tagged with: accounts, activation, ATMs, banks, bill pay, card network, cardholder, cards, costs, deposit, electronic payments, fees, financial institution, In-network, insurance, mobile remote deposit capture, monthly fees, paper check, prepaid, text alerts

December 2nd, 2013 by Elma Jane

U.S. Bank has announced the U.S. Bank Contour Card – saying that the new card gives customers the convenience of a debit card, the control of a bank account and the freedom of cash. Giving customers innovative options to manage their finances. The Contour Card is the latest example. It’s a great tool to manage expenses by giving you the power to budget your money across multiple prepaid cards under the same account. Customers can use Contour as their primary payment card, but it is also a good fit for anyone who wants a new way to manage money.

Contour gives control over your spending in so many ways. From tracking your spending to transferring money between accounts, Contour gives customers the ability to manage it all from one location through their personal My Contour Dashboard.

Cardholders can open up to five additional card accounts that can be linked to their primary account. Cardholders can use Contour anywhere Visa Debit cards are accepted, get free cash withdrawals at any U.S. Bank or MoneyPass ATMs, and direct deposit paychecks to their accounts at no additional charge.

Posted in Financial Services Tagged with: account, ATMs, budget, card, cardholders, debit card, deposit, finances, money, MoneyPass, paychecks, prepaid, tracking, tranferring, U.S. Bank, US Bank, visa, withdrawals

October 29th, 2013 by Elma Jane

Three dimensions merchants must look for in a payment system PSP and ISO:

1. Ability to adapt and customize the solution.

2. Solutions that support broad range of payment methods.

3. Supports a full set of different channels and devices.

Difference between a PSP and ISO in the payments ecosystem? Online and Mobile Payments:

There are two types of merchant service providers and not all service providers are made equal, Processors and Resellers:

Resellers are known in the industry as Independent Sales Organizations (ISO’s) and/or Merchant Service Providers (MSP’s).

1) Resellers or ISOs – ISOs resell the products or services of one or multiple processors. They can also develop their own or aggregate other value added products and services. ISO’s range from a little sketchy to best in class providers.

2) Processors – Also known as Acquirers, processors are distinguished by their ability to actually process a transaction. To be a processor, a company must have the technical capability to receive transaction data from a merchant via a telephone line or the internet and then communicate with the appropriate financial institutions to approve or decline transactions. Processors must also be able to settle completed transactions through financial institutions in order to deposit funds into the merchant’s bank account.

Processors can be banks or non-banks. While processors do maintain a direct sales force of their own, they primarily work through ISOs to acquire and maintain their merchant base. A processor’s business model is really one of economies of scale. They’re volume shops. They essentially outsource the sales function to ISOs. The processing industry is highly concentrated with the top five processors maintaining over 70% of all transaction volume.

Types of ISOs:

1. Banks – Banks of all shapes and sizes are ISOs. Banks entered into the merchant services business because it was a natural fit with their product and service offerings. It’s a way to increase revenue per customer. Most, but not all banks, will private label the services so that it’s difficult to distinguish whether they are a processor or ISO. The benefit of working with a bank is that you can consolidate your financial services. The drawback is, the you usually get out of the box solutions and service.

2. Non-banks – These types of ISOs range from some of the most dynamic and capable providers to firms who don’t represent the industry very well.

Industry Dynamics – There are a few dynamics that make the industry landscape quite interesting. First, there are very barriers to entry due to the lack of certifications, licenses, and capital requirements. Secondly, there really is no active regulatory body that oversees and enforces acceptable practices. So naturally, with these two market conditions, merchants need to be mindful and thorough in selecting a provider.

Processors versus ISOs In comparing the two, ISOs offer all of the products and services that processors do (because they are reselling) but processors can’t always offer the same products and services as ISOs. This is because ISOs can resell for multiple processors and can either develop their own technologies or aggregate solutions from other providers. ISOs have largely been the most successful creators of value-added services. ISO’s also tend to be smaller, which usually (but not always) leads to better customer service.

Processors are usually a safer bet for newer merchants that are still learning about the industry. Most still maintain what consider less-than-upfront pricing practices, but with their services it is less common to hear about some of the more serious problems that merchants encounter when they deal with the wrong ISO. As for price, in most cases, there really is very little to no difference. I argue, and fully disclose my vested interest, that in nearly any situation a best in class, non-bank ISO can provide more value than a processor.

Posted in Best Practices for Merchants, Credit card Processing, Electronic Payments, Financial Services, Mail Order Telephone Order, Merchant Services Account, Visa MasterCard American Express Tagged with: account, acquirers, aggregate, approve or decline, bank, best in class, channels, customize, data, deposit, devices, financial, independent sales organizations, internet, ISO, merchant service providers, Merchant's, mobile, msp, non-banks, online, payment methods, payment system, payments, processors, psp, resellers, solution, telephone, transaction, value added

October 24th, 2013 by Elma Jane

You will be happy to learn that these days there is less hassle when setting up credit card payments online. In the past, companies were required to open a merchant account through a bank in order to be able to accept credit cards. Today, several services enable you to accept credit cards online without opening your own merchant account.

With more than 50 million users worldwide, Paypal is probably the most widely used such service. The company’s Payflow service is a turn-key solution with several added advantages such as recurring billing and fraud protection.

If you still want to take actual credit card payments online, a merchant account service is your best option. To open an Internet merchant account, you must fill in a merchant application and provide support documents. First, you must supply proof that you established a checking account for your Internet business.

If you have sole proprietorship or a micro business, you can open either a personal checking account or business checking account. If you opt for a personal checking account, the account must be in the name of the sole proprietor. If your internet business is a corporation, you must set up a corporate checking account.

This account will be used to deposit sales generated through your internet merchant account, but also to withdraw fees such as online payment gateway fees.

Posted in Best Practices for Merchants, Credit card Processing, e-commerce & m-commerce, Electronic Payments, Internet Payment Gateway, Visa MasterCard American Express Tagged with: accept, application, checking account, companies, credit-card, deposit, fraud protection, internet business, merchant account, merchant account service, micro business, online, payment gateway fees, payments, PayPal, recurring billing, sales, support, turn-key, worldwide

Mobile ascertain deposit, one time a reduced main concern expertise for banks, has become one of the most searched out Mobile banking app characteristics. But along with attractiveness and increased use, the promise for deception is emerging for smartphone ascertain down payments.

A latest report from ath Power Consulting recognizes isolated deposit arrest as Mobile banking users’ most desired app characteristic.

Banks are responding. Research from Celent displays that in 2009, 72% of reviewed financial institutions had no designs to offer Mobile isolated deposit arrest (RDC). By 2012, only 18% were holdouts. Read more of this article »

Posted in Mobile Payments Tagged with: deposit, Mobile ascertain deposit, RDC technology, smartphone