December 19th, 2024 by Elma Jane

Surcharges and Convenience Fees:

A surcharge is a fee that is added to a card transaction, either as a set amount or a percentage of a transaction. Typically, used to cover the cost of the merchant account charges.

There are rules, exceptions and state laws to observe to ensure you are compliant.

At present there are surcharge bans in the following states:

California, Colorado, Connecticut, Florida, Kansas, Maine, Massachusetts, New York, Oklahoma and Texas. (Appeals are pending for California and Florida)

Surcharge Rules:

- Applicable only to credit card transactions, not debit or prepaid card transactions.

- The surcharge cannot be greater than the merchant’s average discount rate for that brand’s credit card transactions.

- Maximum surcharge allowed is 4%.

- Cardholder must be notified of the surcharge.

- Surcharge must be listed on the receipt as a line item and the primary payment amount must be processed together as one transaction.

A convenience fee is a fee charged for the “convenience” of being able to pay using an alternative payment channel outside the merchant’s customary payment channel.

Any merchant can charge a convenience fee IF the fee charged is for the legitimate convenience of being able to pay using a different payment channel than the merchant’s usual payment channel.

Example: Your business customary payment channel is face-to-face or card present and you provide an alternative payment channel, such as the option to pay by phone using a credit card, that could then charge a convenience fee along with the payment.

Mail Order/Telephone Order (MOTO) merchants and ecommerce merchants, whose customary payment channel is exclusively non face-to-face or card-not-present, are NOT permitted to charge convenience fees.

Convenience Fee Rules:

- Customer must be notified of the convenience fee prior to finalizing payment and given the opportunity to cancel.

- Payment must take place through an alternative payment channel.

- The fee can only be added to a non face-to-face transaction. Must be flat or fixed, regardless of the value of the payment due.

- The fee must be applied to all means of payment accepted through the alternative payment channel. Must be included in the total transaction amount.

Posted in Best Practices for Merchants, e-commerce & m-commerce, Mail Order Telephone Order Tagged with: card-not-present, Convenience Fees, credit card, debit, ecommerce, merchant, moto, payment, prepaid card, Surcharges, transaction

May 19th, 2024 by Elma Jane

NTC Product and Services

To be responsive to the needs of our merchants and to meet that needs NTC offers next day funding. This is a value added service for customers and businesses that need to have their funds available quickly.

With more than 20 years of experience, National Transaction offers a variety of electronic payment services and technology for Retail and Ecommerce industries. From Travel, Medical Industry, Charitable Institution and Franchise.

Our services include:

Loans/Funding Program

Credit and Debit Card Processing

Currency Conversion

Electronic Checks

Electronic Invoicing

Gift and Loyalty Card Programs

Mobile and Online Solutions

Shopping Cart E-commerce Payment Gateway

NTC e-Pay – is an Electronic Invoicing that made simple with NTC e-Pay! Free Setup, nothing to integrate; secure and fast.

Invoice customers Electronically with NTC e-Pay. Our e-Pay Platform can help Merchants bring new customers and encourage repeat business.

Our Virtual Merchant Gateway – accept payments your way! Online, In-Store and On the Go. A payment platform that flexes with your business.

NTC Business Loans – Fast, Affordable, and Simple Application Process.

MediPaid – a medical health insurance claims payment. Delivering paperless, next-day deposits for Health Insurance Payments.

NTC provides services to thousands of customers. NTC maintains a one on one relationships with all its merchants providing them with 24/7 customer service and technical support!

To know more about our product and services give us a call at 888-996-2273

or visit Nationaltransaction.Com

Posted in Best Practices for Merchants, Credit card Processing, Electronic Check Services, Electronic Payments, Financial Services, Gift & Loyalty Card Processing, Mail Order Telephone Order, Merchant Services Account Tagged with: debit card, ecommerce, electronic payment, loans, Loyalty Card, mobile, online, payment gateway, travel

February 9th, 2022 by Admin

John Stewart

January 17, 2022

https://www.digitaltransactions.net/trends-like-open-banking-and-bnpl-will-sustain-e-commerces-hot-streak-a-report-says/

Open banking, single-click checkout wallets, and the hot buy now, pay later trend will all help drive e-commerce volume worldwide in the coming five years, predicts Juniper Research in a report released Monday. This momentum is likely to push online sales long after the short-term impetus from the pandemic subsides, Juniper says.

E-commerce volume totaled $4.9 trillion globally in 2021, a figure the United Kingdom-based research firm forecasts will reach $7.5 trillion in 2026, when China will control a 37% share. Wider availability of multiple e-commerce channels, including mobile devices, will propel the overall growth worldwide, Juniper says. But along with the boom in e-commerce will come a corresponding growth in fraud via identity theft, account takeovers, and fraudulent chargebacks, the report warns. China, for example, will account for more than 40% of fraud losses worldwide in 2025, at more than $12 billion, Juniper forecasts.

Open banking is a trend by which fintechs can verify balances in consumers’ accounts and transfer funds to pay for online purchases. As standards bodies work to promulgate standards for this business, e-commerce payment providers “should … partner with specialists in … specific emerging payment areas to keep pace with changing merchant expectations around acceptance types,” the research firm says in its release, referring to digital wallets and crypto as well as open banking.

Open banking has taken on a higher profile in the global payments market with efforts by both of the global card networks to acquire firms that specialize in this area. Visa Inc. has acquired Tink AB, while Mastercard Inc. bought Aiia and Finicity Corp.

Physical goods will continue to dominate e-commerce spending, the report says, accounting for 82% of payment value by 2026. To tap into the trend, Juniper advises, payments providers should support buy now, pay later plans, which allow consumers to split purchases into four equal installments paid over a six-week period at no interest. BNPL is becoming more controversial, however, as the Consumer Financial Protection Bureau has launched an investigation of the option and as reports emerge that consumers with multiple accounts are more likely to miss a payment.

While still a big trend, e-commerce sales in the U.S. market cooled significantly last year as the pandemic effect lost some of its force. Third-quarter sales in 2021 reached $214.6 billion, up 6.6% year-over-year, according to the Census Bureau, which tracks retail sales. That follows an 8.9% rise in the second quarter and three straight quarters with increases of 32% or more. Fourth-quarter 2021 results are not yet available.

Posted in Credit card Processing, Credit Card Reader Terminal, Credit Card Security, Digital Wallet Privacy, e-commerce & m-commerce, Financial Services, Mail Order Telephone Order, Merchant Account Services News Articles, Merchant Services Account, Mobile Payments, Mobile Point of Sale, Point of Sale, Small Business Improvement, Smartphone, Uncategorized, Visa MasterCard American Express Tagged with: banking and e-commerce, e-commerce, e-commerce businesses, e-commerce merchants, e-commerce processor, e-commerce transactions, ecommerce, ecommerce merchant, ecommerce merchants, ecommerce sites, mobile commerce payment, mobile payment, Mobile Payments, mobile processing transactions, mobile transactions, mobile wallet, mobile wallet transactions, mobile wallets, mobile-commerce payments, online transactions, point-of-sale transactions, transaction processing, transactions, wallet

September 11th, 2020 by Admin

The chargeback process was introduced more than four decades ago as a consumer-protection mechanism. It was meant to inspire consumer confidence in payment cards, which were still a novel concept at the time. Fast-forward to today, though, and these forced payment reversals have evolved into a significant problem for online merchants.

Chargeback abuse—commonly known as friendly fraud—is a major source of loss. In fact, chargeback issuances resulting from friendly fraud were expected to reach $50 billion annually in 2020, according to Mercator Advisory Group.

Even then, this figure is a low estimate. It doesn’t account for current trends in a post-Covid environment, where we’ve seen a dramatic increase in friendly fraud. These attacks were already up by the end of March, and there’s no sign that they’re going to slow down.

Covid-19 might look like the source of the problem on a superficial level. If we dig deeper, though, we see four underlying factors behind the preexisting upward trend in chargeback filings:

- More fraudsters view the CNP environment as the “channel of least resistance;”

- Inconsistency in technologies and regulations across different markets;

- The rise of mobile banking;

- The response by card networks like Visa and Mastercard.

These four factors carry diverse ramifications for the market. For instance, roughly $118 billion in e-commerce transactions are declined each year, according to Javelin Strategy & Research. Most of these rejected purchases are false positives, meaning the merchant unnecessarily rejected the purchase in hopes of avoiding a chargeback.

Clearly, there’s a growing disconnect between merchants, financial institutions, and card networks regarding how best to address this situation. We can see this reflected in the fact that the rate of chargeback issuances in North America is expected to significantly outpace those in the European market. This is attributed to factors like strong customer authentication protocols required by the Revised Payment Services Directive (PSD2), and more widespread use of 3-D Secure technology.

The pressure is on for industry players to find more comprehensive solutions for chargebacks. These solutions must be data-driven and adaptable, though. Otherwise, the growing disconnect between cardholders, merchants, financial institutions, and card networks will exacerbate existing problems in the market, leading to further losses.

The good news is that, in the meantime, there are strategies merchants can employ to address these concerns. For instance, even though friendly fraud operates by concealing itself behind false chargeback reason codes, it’s still helpful to have a clear understanding of what each reason code means in context.

Merchants can’t avoid friendly fraud in the same way they can detect criminal attacks or eliminate merchant errors. However, they can minimize friendly fraud risk by adopting key best practices, including:

- Notifying customers to remind them about recurring payments;

- Keeping organized and well-documented transaction records;

- Using delivery confirmation when shipping physical goods;

- Providing easy access to round-the-clock, live customer service;

- Providing a quick response to any refund or cancellation requests.

Also, if a merchant identifies a chargeback as friendly fraud, it’s important to engage that dispute through the representment process. This is a complex, time-consuming process, which is why many merchants opt to outsource their chargeback management. It’s still possible to conduct the process with in-house management. However, it will require strong evidence to support the merchant’s case, such as:

- A legible sales receipt

- A tracking number

- Any emails or transcripts of communications you’ve had with the customer

- Delivery confirmation information

- A record of in-store pickup

- Photographic evidence (when available)

This evidence needs to be contextualized with a chargeback rebuttal letter, explaining why the original transaction was valid. Also, merchants are on a tight schedule. In most cases, they have only a few days to provide a response to their acquirer.

Chargeback management can be a difficult and confusing process. But, with the problem of chargeback abuse only set to grow over time, it’s something merchants can’t afford to take for granted.

—Monica Eaton Cardone is the chief operating office and cofounder of Chargebacks911, Clearwater, Fla.

COMMENTARY: What Will the Future Hold for Chargebacks in Digital Payments?

Monica Eaton-Cardone September 11, 2020 Competitive Strategies, E-Commerce, Fraud & Security, Issuing/Originating, Mobile Commerce, Point-of-sale, Transaction Processing

Posted in Best Practices for Merchants, Credit card Processing, Credit Card Security, e-commerce & m-commerce, Electronic Payments, Internet Payment Gateway, Uncategorized, Visa MasterCard American Express Tagged with: chargeback, chargebacks, ecommerce, ecommerce merchant, ecommerce merchants, ecommerce sites, electronic payment, electronic transactions, fraud protection, mobile payment security, strategies, transaction security

September 14th, 2017 by Elma Jane

Payments standards body EMVCo has updated its Payment Tokenisation Technical Framework to introduce the new roles of token programme and token user, refine the roles of token service provider and token requestor and detail their interrelationships within the global payments environment.

EMV Payment Tokenisation Specification — also includes expanded ecommerce use cases and operational management enhancements to support global interoperability and facilitate transaction security.

This latest version offers significant updates and use cases that reflect payment industry input to define how EMV payment tokens are generated, deployed and managed. The level of detail assists in establishing a stable payment environment and delivering a common set of tools to facilitate transaction security.

The technical framework needs to capture these industry requirements and be flexible enough to interoperate with the existing payment ecosystem while supporting ecommerce, new payment methods and regional variations.

EMVCo is calling on the payments community to get involved and provide feedback.

EMVCo was formed by Europay International, MasterCard International, and Visa International to manage, maintain and enhance the EMV specifications for payment systems.

Posted in Best Practices for Merchants Tagged with: ecommerce, EMV, payments, Security, service provider, token, Tokenisation

April 6th, 2017 by Elma Jane

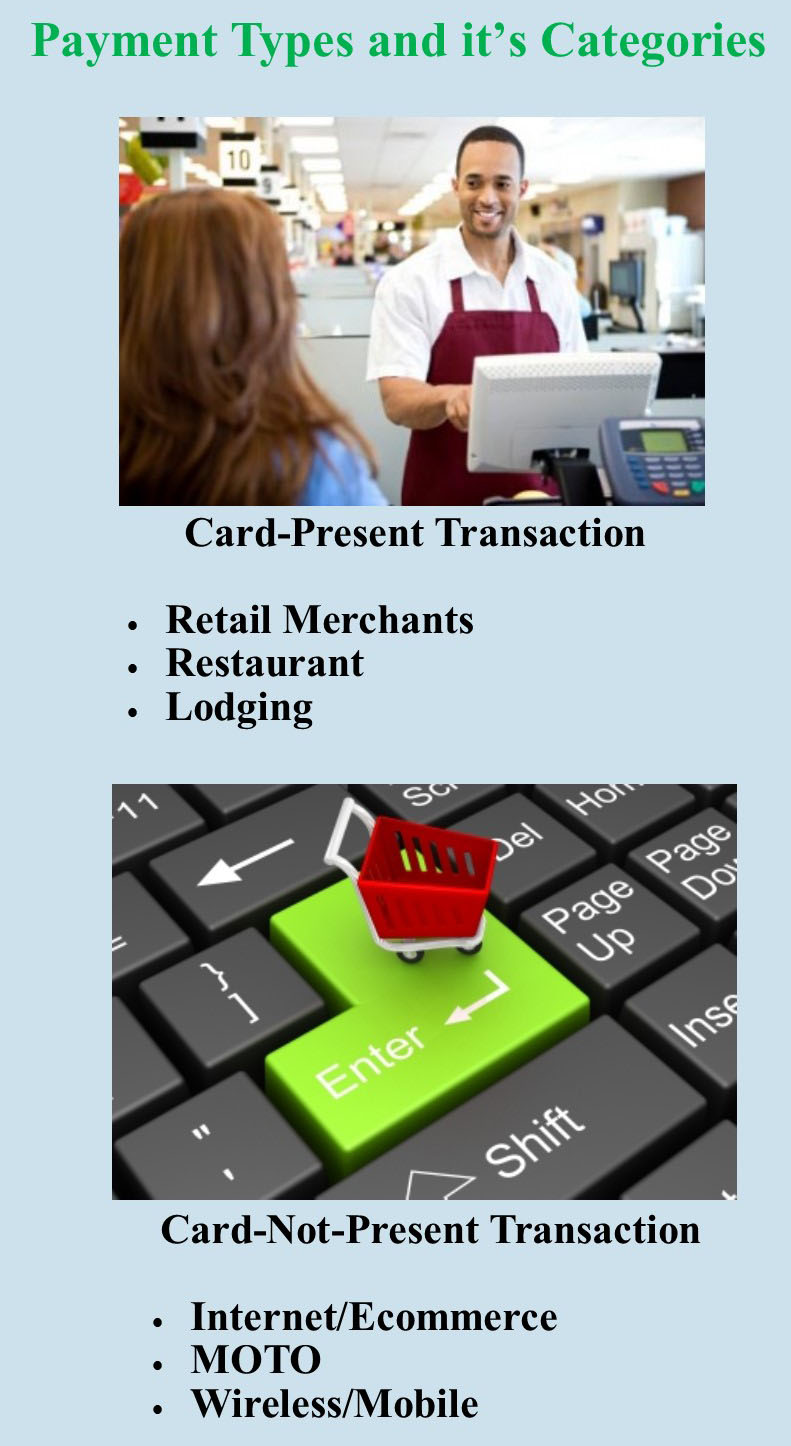

Payment types and it’s categories

The two main category types when it comes to credit card processing are swiped and keyed. Card present or card-not-present.

Swiped or card present transaction – merchants do a face-to-face transaction. A merchant can capture card information by dipping the chip or swiping the card in the terminal or POS. Merchants directly interact with a customer so the risk is low.

Card-Present Sub Categories:

Retail Merchants – conduct transactions face to face in a retail environment.

Face to Face (mobile) – this type of merchant is typically on the go, such as a vendor at a trade show. You can use a service like converge mobile that allows you to take the information in person.

Restaurant – the same as retail merchants, the difference is they may require the ability to add tips to their charges.

Lodging – processes their transactions like retail merchants except they may adjust the settlement amount depending on the customer’s length of stay.

Keyed or card-not-present are high risk, because merchants indirectly collect customers card information, and can process transactions in various ways.

Card-Not-Present Sub categories:

Internet/Ecommerce – conducts business through a web site by utilizing a shopping cart and an Internet payment gateway service. The payment gateway then collects the credit card information and processes it in real time.

Mail & Telephone Order (MOTO) – typically take the customer’s credit card information over the phone, by mail or through the Internet. They then manually process the transaction by keying it into either a credit card machine or through a virtual terminal such as Converge.

Talk to our payment consultant to know the best solution for your business.

NationalTransaction.Com 888-996-2273

Posted in Best Practices for Merchants Tagged with: card present, card-not-present, credit card, customer, ecommerce, merchants, payment, payment gateway, POS, swiped and keyed, terminal, virtual terminal

December 21st, 2016 by Admin

Ways to Prevent CHARGEBACK:

Provide Receipts for every single transaction. Receipt serves as a good reminder to the purchase they make and decreases the likelihood of a charge back. Have the conditions of sale written on the receipt

Be clear about refunds, returns and cancellation policies – include refund, return and cancellation policy on your website.

Make sure charge descriptions are clear. Use dynamic descriptors – with dynamic descriptors, you can include specifics like the product purchased, business name, business location and contact information. Include a number as part of the charge description.

Provide accurate descriptions of products and services – accurate product descriptions are particularly important for online ecommerce where customers often dispute transactions because the product they received is not as it was described online.

Get signed proof of delivery products – especially if you’re an online ecommerce vendors that ships products regularly.

Communicate with customers about renewals – if your customer accounts are set to automatically renew, make sure you notify those customers of their renewal months leading up to the renewal day.

When a cardholder contacts their credit card-issuing bank and asks for a refund on a transaction for a purchase or service made on their card is called chargeback.

Most Common Reasons for Chargebacks:

Point-of-sale processing errors

Customer disputes like, customer doesn’t recognize the charge, customer claims they didn’t receive the item they ordered.

Fraud, or potential fraud (customer claims the transaction is fraudulent – the purchase was made with a stolen card).

Posted in Best Practices for Merchants Tagged with: bank, cardholder, chargeback, credit card, customer, ecommerce, fraud, online, point of sale, transaction

May 12th, 2016 by Elma Jane

Electronic commerce (eCommerce) is a type of business transaction, that involves the transfer of information on the Internet. This allows consumers to exchange goods and services with no barriers of time or distance electronically.

Business-to-Business (B2B) this refers to electronic commerce, between businesses rather than between a business and a consumer. These transactions electronically provide competitive advantages over traditional methods. It’s faster, cheaper and more convenient.

Creating a successful online store can be difficult if you don’t have knowledge of e-commerce and what it is supposed to do for your online business.

What do you need to have an online store?

- Shopping cart – an operating system that allows consumers to buy goods and or services. Track customers, and tie together all aspects of e-commerce into one.

- Or you can check out our NTC e-Pay no shopping cart Solution.

- Taking online payment by getting a merchant account and accept credit cards through an online payment gateway.

You just need to make a better decision in choosing the right shopping cart and a merchant account for your eCommerce shop.

Posted in Best Practices for Merchants, e-commerce & m-commerce Tagged with: b2b, commerce, consumers, credit cards, customers, ecommerce, gateway, merchant, merchant account, NTC e-Pay, online, online payment, payment gateway, shopping cart, transaction

April 20th, 2016 by Elma Jane

ECS: An Electronic Mode Of Funds Transfer From One Bank Account To Another

- Paper check conversion

- Debit Processing

- Automated Returns Management

- Reporting: Merchant Connect, ACS Standard and Custom Files, Enquire and Corporate Management Reports

- Monthly Statement

- Risk Services: Verification, Conversion

- Image

ACH E-CHECK: Uses Bank Routing and Account Number In a CNP Environment.

- Card-Not-Present e-Processing of ACH Debit

- Known Relationship B/Consumer and Business

- NOT for Ecommerce “Sale of Goods and Services”

- Debit Processing

- Automated Returns Management

- Reporting: Merchant Connect, ACS Standard and Custom Files, Enquire and Corporate Management Reports

- Monthly Statement

- Risk Services: Verification, Conversion

- No Image

Posted in Best Practices for Merchants, e-commerce & m-commerce Tagged with: account, ACS, bank, card-not-present, cnp, consumer, debit, ecommerce, ECS, merchant, risk, services

November 17th, 2015 by Elma Jane

Within the payment processing industry, Merchant accounts are categorized according to how they process their transactions.

There are two primary merchant account categories:

Swiped (Card Present) and Keyed (Card-Not-Present).

Swiped or Card-Present Transactions: Are those in which both the card and the cardholder are present at the time the payment is processed, they physically swipe their customers credit card through a terminal or point-of-sale system.

The sub-categories within this group include:

Retail Merchants – Normally conduct their business in an actual storefront or office space. They primarily use counter-top terminals or Point-of-Sale systems. Restaurant Merchants – Requires a special set-up that allows for tips to be added to the final sale amount by settling the transaction with an adjusted price that will include the tip amount.

Wireless / Mobile Merchants – They use wireless terminals or mobile phones to run these transactions in Real-Time. Have the ability to accept credit cards transactions wherever they are located out on the road.

Hotel / Lodging Merchant – Will authorize a customer’s credit card for a certain sale amount.

Card-Present Transactions also include grocery stores, department stores, movie theaters, etc. Card acceptance settings where cardholders use unattended point-of-sale (POS) terminals, such as gas stations, are also defined as card-present transactions.

Keyed-In or Card-Not-Present Transactions: Whenever the transaction is completed and the cardholder (or his or her credit card) is not physically present to hand to the seller.

The sub-categories within this group include:

Mail Order / Telephone Order (MOTO) – The customers card information is gathered via over the phone, fax, email or internet and then manually key-entered into a terminal or payment gateway software. Once the transaction is approved and completed, the product is then shipped to the customer for delivery.

eCommerce / Internet – Conduct ALL of their business over the internet through a web site. So all credit card transactions are processed online via a payment gateway in real-time. The payment gateway is integrated into the web sites shopping cart. The cardholders card is charged instantly.

Travel Merchants is one example of Keyed or Card-Not-Present Transactions.

Start processing credit card payments today whether Swiped or Keyed.

Give us a call now at 888-996-2273 so more details!

Posted in Best Practices for Merchants, e-commerce & m-commerce, Mail Order Telephone Order, Mobile Payments, Mobile Point of Sale, Point of Sale, Smartphone, Travel Agency Agents Tagged with: Card Not Present transactions, card present, card-not-present, card-present transactions, cardholder, credit card, credit card payments, credit card transaction, ecommerce, keyed, Lodging Merchant, mail order, merchant accounts, merchants, mobile merchants, moto, payment gateway, payment processing, point of sale, POS terminals, Restaurant Merchants, Retail Merchants, shopping cart, swiped, telephone order, terminal, transactions, travel merchants