In today’s fast-paced digital world, customers expect businesses to offer a variety of payment options. Electronic payment processing has become essential for businesses of all sizes, from small startups to large corporations. This article will provide you with all the information you need to know about electronic payment processing and why National Transaction Corporation is the best choice for your business.

What is Electronic Payment Processing?

Electronic payment processing refers to the electronic transfer of funds from a customer’s account to a business’s account. This can be done through various methods, including credit cards, debit cards, e-checks, and mobile payments. Electronic payment processing is faster, more secure, and more convenient than traditional paper-based methods.

Benefits of Electronic Payment Processing

Faster Processing Times: Electronic payments are processed much faster than paper checks, which can take several days to clear.

Improved Security: Electronic payment processing is more secure than traditional methods, as it uses encryption and other security measures to protect sensitive data.

Increased Convenience: Customers can make payments from anywhere at any time, using their computer, smartphone, or tablet.

Reduced Costs: Electronic payment processing can save businesses money on processing fees and other costs associated with traditional methods.

Improved Cash Flow: Businesses can receive payments more quickly, which can improve their cash flow.

Why Choose National Transaction Corporation?

National Transaction Corporation is a leading provider of electronic payment processing solutions. We offer a wide range of services to businesses of all sizes, including:

Credit and Debit Card Processing: We accept all major credit and debit cards, including Visa, Mastercard, American Express, and Discover.

E-Check Processing: We offer e-check processing services, which allow customers to make payments directly from their bank account.

Mobile Payment Processing: We offer mobile payment processing solutions, which allow customers to make payments using their smartphone or tablet.

Online Payment Processing: We offer online payment processing solutions, which allow businesses to accept payments through their website.

At National Transaction Corporation, we are committed to providing our clients with the best possible service. We offer:

Competitive Rates: We offer competitive rates on all of our services.

Reliable Service: We provide reliable service that you can count on.

Excellent Customer Support: We offer excellent customer support, available 24/7.

Secure and Compliant Solutions: We are PCI DSS compliant, ensuring the security of your customers’ data.

Make the Switch to Electronic Payment Processing Today

If you’re not already accepting electronic payments, now is the time to make the switch. National Transaction Corporation can help you get started with our easy-to-use and affordable solutions. Contact us today to learn more about how we can help your business grow.

The way we pay for goods and services has undergone a dramatic transformation. From bartering to coins to paper money, the journey of payment methods has been long and fascinating. But no shift has been as revolutionary as the rise of electronic payments. Let’s dive into this evolution and explore where this exciting technology might lead us next.

Early Days (1950s – 1970s):

1950: The Diners Club card emerges as the first multipurpose charge card, laying the foundation for modern credit card systems.

1958: American Express launches its charge card, initially paper-based, revolutionizing travel and expense tracking.

1966: Barclays Bank in London introduces the first Automated Teller Machine (ATM), allowing customers basic account access outside banking hours.

1970s: Electronic Funds Transfer (EFT) systems gain traction, enabling direct deposit of paychecks and automated bill payments.

Rise of Digital Networks (1980s – 1990s):

1979: Visa introduces the first electronic authorization system and point-of-sale (POS) terminal, paving the way for real-time transaction processing.

1983: Debit cards become more prevalent, allowing consumers to access funds directly from their bank accounts.

1994: First Virtual Holdings pioneers the first secure online payment system, marking the dawn of e-commerce.

Late 1990s: Online banking explodes in popularity, offering customers convenient account management and payment options.

The Internet Age (2000s – Present):

1998: PayPal emerges, simplifying online transactions and boosting consumer confidence in online shopping.

2003: Mobile payments gain momentum in various countries, driven by the increasing adoption of mobile phones.

2010s: Near Field Communication (NFC) technology enables contactless payments, giving rise to mobile wallets like Apple Pay and Google Pay.

2020s: Biometric authentication adds another layer of security to electronic payments, using fingerprints and facial recognition. Real-time payment systems gain popularity, allowing for instant fund transfers.

The Future of Electronic Payments:

Invisible Payments: Imagine a world where payments happen seamlessly in the background. Technology like Amazon Go is already showcasing this, with customers simply walking out of stores with their purchases.

Cryptocurrency and Blockchain: While still in its early stages, the potential of cryptocurrencies and blockchain technology to disrupt traditional payment systems is enormous. Expect to see more integration and wider acceptance in the coming years.

AI-Powered Payments: Artificial intelligence will play a crucial role in fraud prevention, personalized payment experiences, and the development of even more innovative payment solutions.

Increased Financial Inclusion: Electronic payments have the potential to bring banking services to underserved populations, promoting financial inclusion on a global scale.

The evolution of electronic payments is an ongoing journey. As technology continues to advance, we can expect even more exciting developments that will reshape the way we transact and interact with the world around us.

In our second installment, we talked about NTC’s newest solution, NTC ePay. This third and final reason in this series we will go over how NTC keeps your cashflow going.

Due to the history of travel businesses, many travel agencies are given a travel merchant account with monthly credit card processing volume caps. This means merchants are only permitted to handle a specific number of credit card transactions or volume amount per month. Once that limit amount is reached, the merchant can no longer take credit cards for purchases that month. This keeps a business, especially an e-commerce merchant that relies on credit card payments, from operating effectively.

Imagine the impact on as a travel agent when you no longer have to worry about having your cash flow stopped. We work very hard to eliminate holds and reserves on all our travel merchant accountsaccounts.

Now imagine getting approved for large volume.

You will agree that those two factors will have a huge positive impact on your business growth.

Most merchant providers usually hold funds from travel agents, because historical data shows that consumers are much more likely to dispute and chargeback travel agency transactions because of a change in their travel plans.

You may be wondering, why do we not hold your funds?

Well simply said, because we understand your business. NTC has been doing business with travel professionals like you for over 20 years and we understand that holding funds creates a huge hassle for your operation. We understand that cash flow is essential to your continued success.

With NTC travel agents can feel confident that they will maintain cash flow to help their business operate smoothly and efficiently without interruptions.

Why do travel merchants flag large transactions?

Many times travel merchants run tens of thousands of dollars worth of transactions and their processor tells them they’re going to simply hold the funds and pay the merchant at a later date.

We understand how critical it is to have funds available because many agents have shared how with other merchant providers, their cash flow has come to a complete halt at times.

Remember that when you choose a travel payment processor, you must be sure to choose one with experience in working with travel agencies like NTC.

At NTC, we assist you in developing and implementing your fraud prevention procedures, so that you can be proactive in identifying and correcting potential weak spots in your processing cycle.

Over these past three blog articles, we have shared the three main reasons why travel agents like you prefer National Transaction Corporation. Now we want to hear from you as to which of these three reasons is most important for your travel agency business. We’d love to read your comments below.

When it comes to software, businesses face a fundamental choice: open or proprietary systems. Each offers distinct advantages and disadvantages, and understanding these differences is crucial for making informed decisions that align with your specific needs and goals.

Proprietary Systems: Control and Support

Proprietary systems, like Microsoft Windows or Adobe Photoshop, are owned and licensed by a specific company.The source code is typically kept secret, giving the vendor tight control over the software’s functionality, distribution, and licensing.

Benefits:

Strong Support: Vendors often provide comprehensive customer support, including documentation, training, and dedicated help desks.

Ease of Use: Proprietary software is often designed with user-friendliness in mind, offering intuitive interfaces and streamlined workflows.

Integration: Proprietary systems may integrate seamlessly with other products from the same vendor, creating a unified ecosystem.

Regular Updates: Vendors typically release regular updates, including new features, bug fixes, and security patches.

Drawbacks:

Cost: Proprietary software often requires licensing fees, which can be a significant expense, especially for smaller businesses.

Vendor Lock-in: Reliance on a single vendor can limit flexibility and create dependency.

Limited Customization: Modifying proprietary software is generally restricted, making it difficult to tailor to specific needs.

Open Systems: Flexibility and Collaboration

Open systems are based on open standards, allowing different software components to interoperate and communicate with each other.Open-source software, like Linux or the Apache web server, takes this a step further by making the source code freely available.

Benefits:

Cost-effectiveness: Open-source software is often free to use, distribute, and modify, reducing upfront costs.

Flexibility and Customization: Users have the freedom to adapt the software to their specific needs and integrate it with other systems.

Community Support: A vibrant community of developers and users often contributes to the development, support, and documentation of open-source projects.

Increased Security: With many eyes reviewing the code, vulnerabilities can be identified and addressed quickly.

Drawbacks:

Support: While community support is often available, dedicated support may be limited or require a paid subscription.

Usability:Some open-source software may have a steeper learning curve or lack the polished user interface of proprietary alternatives.

Compatibility: Ensuring compatibility with existing systems and infrastructure may require additional effort.

Making the Choice: Factors to Consider

The decision between open and proprietary systems depends on several factors:

Budget: Open-source solutions can be more cost-effective, especially for startups and small businesses.

Technical Expertise: Open systems may require more technical expertise for installation, configuration, and maintenance.

Customization Needs: If extensive customization is required, open-source software offers greater flexibility.

Support Requirements: Consider the level of support needed and whether community support or paid support options are available.

By carefully evaluating these factors, businesses can make informed decisions about the software that best aligns with their unique requirements and long-term goals.

To Set up your payment processing merchant account call 888-996-2273 now or go to NationalTransaction.Com

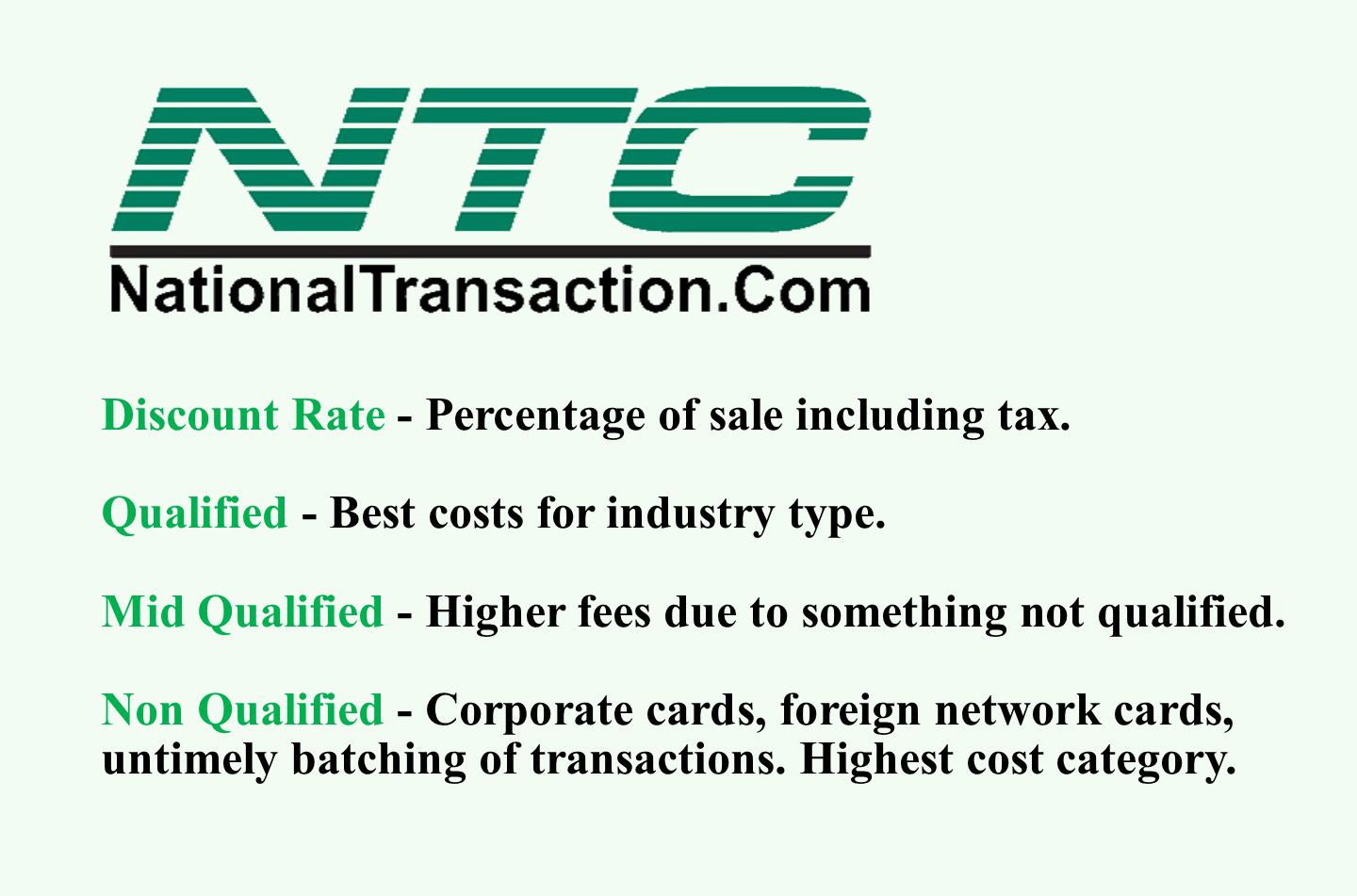

Credit card transaction types are categorized based on the level of risk and processing cost associated with them. Here’s a breakdown of the common types:

1. Qualified

Definition: These are considered the “safest” and least expensive transactions for processors to handle.They typically involve traditional credit or debit cards processed in person with a physical card swipe or chip insertion.

Characteristics:

Card is present during the transaction

Cardholder’s signature is captured (if required)

AVS (Address Verification Service) matches the billing address on file

CVV (Card Verification Value) is provided and matches

Transaction meets all security protocols and risk assessment criteria set by the card issuer and processor.

Examples:Swiping a standard Visa or Mastercard credit card at a retail store.

2. Mid-Qualified

Definition: These transactions fall in between qualified and non-qualified in terms of risk and processing cost. They often involve card-not-present transactions or cards with higher reward structures.

Characteristics:

Manually keyed-in transactions (online, over the phone, or mail order)

Rewards cards with higher cashback or points benefits

Business or corporate cards

Transactions where AVS or CVV information is not provided or doesn’t match

Examples: Entering your credit card details online to purchase something, using a rewards card with travel benefits.

3. Non-Qualified

Definition: These transactions are considered the riskiest and most expensive to process.They often involve international cards, manually keyed transactions without proper security measures, or cards with very high reward programs.

Characteristics:

International credit cards

Manually keyed transactions without AVS or CVV verification

High-risk businesses like online gambling or adult entertainment

Keyed transactions for business or corporate cards

Examples: Using a foreign-issued credit card, manually processing a transaction without verifying the cardholder’s address.

Why does this matter?

Processing Fees: Merchants are charged different fees for each transaction type.Qualified transactions have the lowest fees, while non-qualified transactions have the highest.

Tiered Pricing: Many payment processors use tiered pricing models, categorizing transactions into these types and charging accordingly. This can sometimes be confusing or lead to unexpected costs for merchants.

Interchange Fees: The card networks (Visa, Mastercard, etc.) also charge interchange fees for each transaction, which vary based on factors similar to those used for transaction type categorization.

Understanding these transaction types is crucial for merchants to:

Negotiate better processing rates: By understanding the factors that influence transaction categorization, merchants can negotiate better fees with their processors.

Optimize payment processing: Merchants can take steps to minimize the number of mid-qualified and non-qualified transactions, such as encouraging in-person payments or using address verification systems.

Control costs: By being aware of the different transaction types and their associated costs, merchants can better manage their payment processing expenses.

Remember: The specific criteria for each transaction type can vary depending on the payment processor, card network, and individual merchant account. It’s always best to clarify with your payment processor to understand their specific categorization rules and fee structures.

To establish a merchant account for your business call now 888-996-2273 or click here NationalTransaction.Com

To be responsive to the needs of our merchants and to meet that needs NTC offers next day funding. This is a value added service for customers and businesses that need to have their funds available quickly.

With more than 20 years of experience, National Transaction offers a variety of electronic payment services and technology for Retail and Ecommerce industries. From Travel, Medical Industry, Charitable Institution and Franchise.

Our services include:

Loans/Funding Program

Credit and Debit Card Processing

Currency Conversion

Electronic Checks

Electronic Invoicing

Gift and Loyalty Card Programs

Mobile and Online Solutions

Shopping Cart E-commerce Payment Gateway

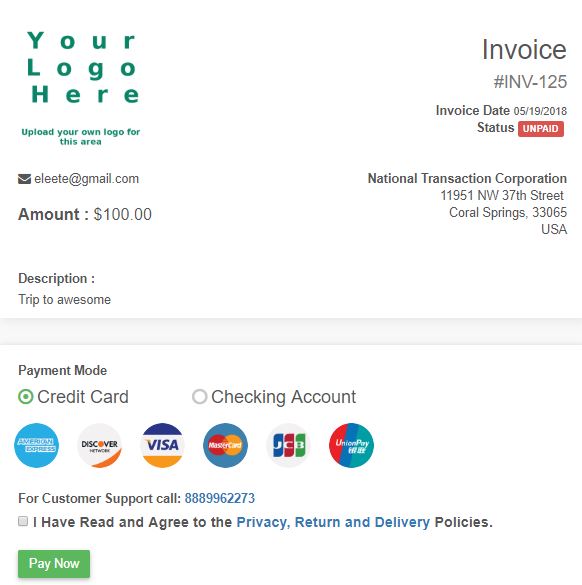

NTC e-Pay – is an Electronic Invoicing that made simple with NTC e-Pay! Free Setup, nothing to integrate; secure and fast.

Invoice customers Electronically with NTC e-Pay. Our e-Pay Platform can help Merchants bring new customers and encourage repeat business.

Our Virtual Merchant Gateway – accept payments your way! Online, In-Store and On the Go. A payment platform that flexes with your business.

NTC Business Loans – Fast, Affordable, and Simple Application Process.

MediPaid – a medical health insurance claims payment. Delivering paperless, next-day deposits for Health Insurance Payments.

NTC provides services to thousands of customers. NTC maintains a one on one relationships with all its merchants providing them with 24/7 customer service and technical support!

To know more about our product and services give us a call at 888-996-2273

Travel Agents prefer NTC ePay because they get paid faster with their very own “Buy Now” button or simply by requesting payments by email!

In our last installment, we shared how the security of NTC Payment Processing works for you. In this second part of our three-part series, we discuss the ways that the technology behind NTCePay helps your travel agency.

NTCePay offers travel agents the most innovative technology because it is fast, mobile friendly and easy to use.

Whether you use Quickbooks, Peachtree or any other accounting application, you can enter the invoice number into the ePay application for reconciliation, and you can customize your pricing to any amount you choose. Your agency can create invoice and payment links that can be posted to your website or any social media website for payment.

Things flow better when everything seems to work together, making your day a lot easier? Technology is something that can get your daily workflow to go smoothly, and NTC ePay works for you. If you need a customized solution to go with your workflow, NTC can make most anything a reality for your business workflow.

National Transaction Corporation is one of the few travel payment processing companies that can directly integrate with both TRAMS and SABRE. You can perform your bookings like you always have but have the payment flow the way you need it to. We also integrate with many booking engines and shopping carts allowing you many options that are not available by host agencies.

NTC ePay is simple, secure and sets up in just minutes. It’s a web application, so you can use it on any device you already own: your desktop, laptop, tablet or phone. It lets you add inventory items or use the quick send feature for simplified invoicing.

Our ePay product was designed from the ground up with your security in mind. Even though we encrypt data back and forth to the payment gateway, we also use the gateway to handle the cardholder’s input. NTC’s cutting-edge technology doesn’t store credit card data, nor does it transmit that data. What that means to you is that the liability is 100% on the bank and not your business, as is typically the case. The application is written and hosted on our own servers, so you can set up and be in the e-commerce business within minutes.

By the way, there are also many customizations available to you with NTC ePay which can be set up very easily by your users. Inquire with your specific process and we will meet your specific needs in the travel payment scope.

Now, when you run a social media campaign you can leverage our NTCePay technology to help you increase sales. Use our ePay links to post vacation travel packages or special sales and have customers pay in two clicks.

Next week we will share the third reason in this series why National Transaction Corporation is the preferred choice for travel agents like you.

Remember, when you need a safe and technologically advanced gateway to manage all your travel agency payments, look no further than NTC.

Feel free to call us now at 888-996-2273, if you are ready to start using NTC ePay today.

The chargeback process was introduced more than four decades ago as a consumer-protection mechanism. It was meant to inspire consumer confidence in payment cards, which were still a novel concept at the time. Fast-forward to today, though, and these forced payment reversals have evolved into a significant problem for online merchants.

Chargeback abuse—commonly known as friendly fraud—is a major source of loss. In fact, chargeback issuances resulting from friendly fraud were expected to reach $50 billion annually in 2020, according to Mercator Advisory Group.

Even then, this figure is a low estimate. It doesn’t account for current trends in a post-Covid environment, where we’ve seen a dramatic increase in friendly fraud. These attacks were already up by the end of March, and there’s no sign that they’re going to slow down.

Covid-19 might look like the source of the problem on a superficial level. If we dig deeper, though, we see four underlying factors behind the preexisting upward trend in chargeback filings:

More fraudsters view the CNP environment as the “channel of least resistance;”

Inconsistency in technologies and regulations across different markets;

The rise of mobile banking;

The response by card networks like Visa and Mastercard.

These four factors carry diverse ramifications for the market. For instance, roughly $118 billion in e-commerce transactions are declined each year, according to Javelin Strategy & Research. Most of these rejected purchases are false positives, meaning the merchant unnecessarily rejected the purchase in hopes of avoiding a chargeback.

Clearly, there’s a growing disconnect between merchants, financial institutions, and card networks regarding how best to address this situation. We can see this reflected in the fact that the rate of chargeback issuances in North America is expected to significantly outpace those in the European market. This is attributed to factors like strong customer authentication protocols required by the Revised Payment Services Directive (PSD2), and more widespread use of 3-D Secure technology.

The pressure is on for industry players to find more comprehensive solutions for chargebacks. These solutions must be data-driven and adaptable, though. Otherwise, the growing disconnect between cardholders, merchants, financial institutions, and card networks will exacerbate existing problems in the market, leading to further losses.

The good news is that, in the meantime, there are strategies merchants can employ to address these concerns. For instance, even though friendly fraud operates by concealing itself behind false chargeback reason codes, it’s still helpful to have a clear understanding of what each reason code means in context.

Merchants can’t avoid friendly fraud in the same way they can detect criminal attacks or eliminate merchant errors. However, they can minimize friendly fraud risk by adopting key best practices, including:

Notifying customers to remind them about recurring payments;

Keeping organized and well-documented transaction records;

Using delivery confirmation when shipping physical goods;

Providing easy access to round-the-clock, live customer service;

Providing a quick response to any refund or cancellation requests.

Also, if a merchant identifies a chargeback as friendly fraud, it’s important to engage that dispute through the representment process. This is a complex, time-consuming process, which is why many merchants opt to outsource their chargeback management. It’s still possible to conduct the process with in-house management. However, it will require strong evidence to support the merchant’s case, such as:

A legible sales receipt

A tracking number

Any emails or transcripts of communications you’ve had with the customer

Delivery confirmation information

A record of in-store pickup

Photographic evidence (when available)

This evidence needs to be contextualized with a chargeback rebuttal letter, explaining why the original transaction was valid. Also, merchants are on a tight schedule. In most cases, they have only a few days to provide a response to their acquirer.

Chargeback management can be a difficult and confusing process. But, with the problem of chargeback abuse only set to grow over time, it’s something merchants can’t afford to take for granted.

—Monica Eaton Cardone is the chief operating office and cofounder of Chargebacks911, Clearwater, Fla.

Have you ever had issues with your credit card processing provider only to get turned around and around by the rep on the phone? IF you can even get someone on the phone. You hang up feeling frustrated, angry, and without any answers.

Sometimes it’s a small problem, but what happens when they “misplace” your money, or there’s a problem with your account and you can’t receive any payments – and no amount of calling, emailing, or “chatting” seems to help you resolve anything?

There’s a better alternative to credit card payment processing, a company that’s been around for a long time, and is backed by one of the biggest banks in the country. National Transaction Corporation. And we have live, knowledgeable, friendly advisors waiting to pick up your calls and help you with your questions – no runaround, no excuses, no delays.

That’s the NTC way: Help when you need it, on a human level.

You may have had to make a lot of phone calls about chargebacks if you are using one of the more familiar service providers like PayPal, Stripe or Square. Chargebacks are a primary cause of business owners’ complaints with these companies, because these services will usually side with the cardholder in the event of a dispute as they arbitrate the chargeback themselves.

NTC does business fairly and sensibly. When you process your credit card sales through NTC, you will be dealing with Visa, MasterCard, American Express or other credit card companies directly.

When you work with those other service providers, you may be worried about where your money might end up – especially if you’ve read all the nightmarish complaints that business owners like you have posted on trusted sites like the Better Business Bureau and Consumer Affairs.

Imagine you’ve processed a credit card transaction, and the cash seems to disappear? You call and you write and you chat, but no one has anything helpful to offer you and you wonder just where your money went, and what will happen to it now.

NTC knows that’s not how you build trust with your customers. We pride ourselves on our outstanding customer support, ease of use of our services, and the confidence and integrity that comes from being backed by one of the biggest banks in the country, US Bank.

National Transaction Corporation aims to make growing your business easier and more profitable by tailoring our services to your specific needs. We do this because we like you to establish a long-term partnership with us.

Whether you are a florist, a restaurant, or any other kind of merchant, remember to look beyond just the advertised rate when looking for the best credit card payment processing service provider.

If after reading this article and you would like to speak to one of our live customer service representatives, simply call NTC today at 888-996-2273.

Paying with a credit card seems like a simple process. You charge the customer, they swipe their card, and then they walk out the door.

But behind the scenes, it’s a bit more complicated.

A credit card payment involves four parties.

The Merchant

The Customer

The Issuing Bank

The Merchant Services Provider

You know who the Merchant and Customer are – that’s the easy part.

The Issuing Bank is the institution that lends money to the Customer.

When the Customer swipes their card, the Issuing Bank lends them the sale amount. This loanis given with the understanding that the Customer will pay the amount back within 30 days or repay it with interest.

Before the Merchant sees any of that money, it goes through the Merchant Services Provider. In exchange for their credit card processing services, they take out a fee before paying that money to the Merchant.

These fees vary between Merchant Services Providers, but one thing is certain: The Merchant always receives less money than the Customer paid them.

This might seem like a raw deal. However, accepting credit cards can lead to more sales than if you only accept cash.

On our next article we will discuss how to start accepting credit card payments and understanding the processing fees….so stand by for more information about Electronic Payment Processing.