September 22nd, 2015 by Elma Jane

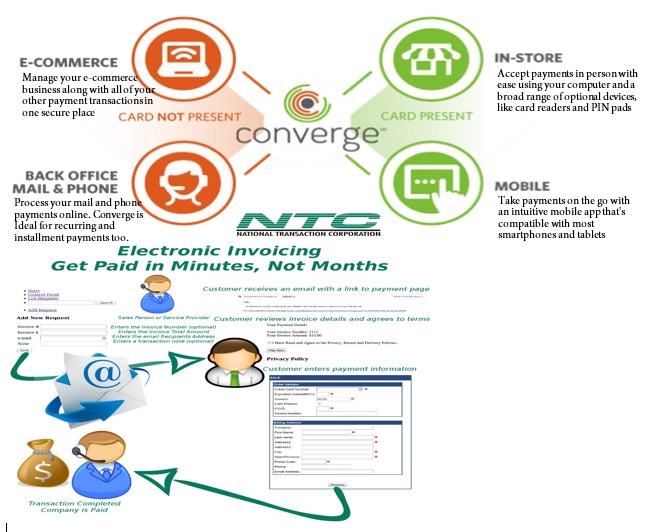

Virtual Merchant/Virtual Merchant Mobile now called Converge, is a popular product offering solutions for retail stores, Non Face to Face businesses along with E-commerce/Internet sites. Converege can be access anywhere with internet. Users can download the application on their smartphone or tablet. Converge also gives users the convenience of sending an invoice to customers electronically with NTC e-Pay!

For Retail store National Transaction offers the latest in EMV and NFC technologies. NTC customers can accept contactless payment with the same NFC technology used by Apple Pay, Google Wallet and SoftCard. NTC offers different solutions that cater to your business needs. For those already using a POS system, NTC integrates with most systems. NTC has you covered.

Posted in Best Practices for Merchants, e-commerce & m-commerce, Electronic Payments, Mobile Payments, Mobile Point of Sale Tagged with: Apple Pay, contactless payment, Converge, e-commerce, EMV, Google Wallet, nfc, POS system, smartphone, tablet, virtual merchant

September 2nd, 2014 by Elma Jane

While Apple doesn’t talk about future products,latest report that the next iPhone would include mobile-payment capabilities powered by a short-distance wireless technology called near-field communication or NFC. Apple is hosting an event on September 9th, that’s widely expected to be the debut of the next iPhone or iPhones. Mobile payments, or the notion that you can pay for goods and services at the checkout with your smartphone, may finally break into the mainstream if Apple and the iPhone 6 get involved.

Apple’s embrace of mobile payments would represent a watershed moment for how people pay at drugstores, supermarkets or for cabs. The technology and capability to pay with a tap of your mobile device has been around for years, you can tap an NFC-enabled Samsung Galaxy S5 or NFC-enabled credit card at point-of-sale terminals found at many Walgreen drugstores, but awareness and usage remain low. Apple has again the opportunity to transform, disrupt and reshape an entire business sector. It is hard to overestimate what impact Apple could have if it really wants to play in the payments market.

Apple won’t be the first to enter the mobile-payments arena. Google introduced its Google Wallet service in May 2011. The wireless carriers formed their joint venture with the intent to create a platform for mobile payments. Apple tends to stay away from new technologies until it has had a chance to smooth out the kinks. It was two years behind some smartphones in offering an iPhone that could tap into the faster LTE wireless network. NFC was rumored to be included in at least the last two iPhones and could finally make its appearance in the iPhone 6. The technology will be the linchpin to enabling transactions at the checkout.

Struggles

The notion of turning smartphones into true digital wallets including the ability to pay at the register, has been hyped up for years. But so far, it’s been more promise than results. There have been many technical hurdles to making mobile devices an alternative to cash, checks, and credit cards. NFC technology has to be included in both the smartphone and the point-of-sale terminal to work, and it’s been a slow process getting NFC chips into more equipment. NFC has largely been relegated to a feature found on higher-end smartphones such as the Galaxy S5 or the Nexus 5. There’s also confusion on both sides, the merchant and the customer, on how the tech works and why tapping your smartphone on a checkout machine is any faster, better or easier than swiping a card. There’s a chicken-and-egg problem between lack of user adoption and lack of retailer adoption. It’s one reason why even powerhouses such as Google have struggled. Despite a splashy launch of its digital wallet and payment service more than three years ago, Google hasn’t won mainstream acceptance or even awareness for its mobile wallet. Google hasn’t said how many people are using Google Wallet, but a look at its page on the Google Play store lists more than 47,000 reviews giving it an average of a four-star rating.

The Puzzle

Apple has quietly built the foundation to its mobile-payment service in Passbook, an app introduced two years ago in its iOS software and released as a feature with the iPhone 4S. Passbook has so far served as a repository for airline tickets, membership cards, and credit card statements. While it started out with just a handful of compatible apps, Passbook works with apps from Delta, Starbucks, Fandango, The Home Depot, and more. But it could potentially be more powerful. Apple’s already made great inroads with Passbook, it could totally crack open the mobile payments space in the US. Apple could make up a fifth of the share of the mobile-payment transactions in a short few months after the launch. The company also has the credit or debit card information for virtually all of its customers thanks to its iTunes service, so it doesn’t have to go the extra step of asking people to sign up for a new service. That takes away one of the biggest hurdles to adoption. The last piece of the mobile-payments puzzle with the iPhone is the fingerprint recognition sensor Apple added into last year’s iPhone 5S. That sensor will almost certainly make its way to the upcoming iPhone 6. The fingerprint sensor, which Apple obtained through its acquisition of Authentic in 2012, could serve as a quick and secure way of verifying purchases, not just through online purchases, but large transactions made at big-box retailers such as Best Buy. Today, you can use the fingerprint sensor to quickly buy content from Apple’s iTunes, App and iBooks stores.

The bigger win for Apple is the services and features it could add on to a simple transaction, if it’s successful in raising the awareness of a form of payment that has been quietly lingering for years. Google had previously seen mobile payments as the optimal location for targeted advertisements and offers. It’s those services and features that ultimately matter in the end, replacing a simple credit card swipe isn’t that big of a deal.

Posted in Best Practices for Merchants, Mobile Payments, Mobile Point of Sale, Smartphone Tagged with: app, Apple, card, card swipe, cash, checkout machine, checks, chips, credit, credit card swipe, credit-card, customer, debit card, Digital wallets, fingerprint recognition, fingerprint sensor, Galaxy S5, Google Wallet, iOS, Iphone, market, merchant, mobile, mobile device, mobile payment, mobile wallet, Near Field Communication, network, Nexus 5, nfc, payment, payment service, platform, point of sale, products, sensor, services, smartphone, software, statements, swiping card, terminals, transactions, wireless technology

June 4th, 2014 by Elma Jane

Zavers, the online coupon program that was launched through Google 17 months ago, is just going to be one of those things that didn’t work out. Google announced yesterday that it is pulling the program, due to lack of interest. Zavers allowed users to clip coupons online and use them in-store. It was intended to help merchants’ build more targeted and effective loyalty and reward programs.

Zavers was basically a coupon program tied with the merchant point-of-sale system. The integration process with the POS systems were proving to be challenging and retailers were not too keen on sharing their data with Google.

Google has said it will continue to work closely with users through the transition away from Zavers and that it continues to move forward with greater focused on more successful areas of their initial entrance into payments such as product listing ads, Google Shopping Express and Google Wallet.

Posted in Uncategorized Tagged with: (POS) systems, coupon program, data, google, Google Shopping Express, Google Wallet, integration, loyalty and reward programs, merchant point-of-sale system, Merchant's, online coupon program, payments, point of sale, POS, retailers

February 10th, 2014 by Elma Jane

Is traditional POS on its way out? Not so fast. It is likely to be an enhancement rather than a replacement to traditional POS.

Trending topic when it comes to POS is all about the mobile kind because Mobile Point of Sale (POS) systems have rocked the retail world. When one searches the term POS, nearly every article that comes up is all about mobile. Many seem to believe it will change the retail industry.

There is definitely a need and a place for both.

Retailers everywhere have incorporated the Internet into their business model by creating multi-channel sales strategies, such as e-commerce, digital marketing, social media marketing, online product information, specifications, reviews and online customer service.

In addition to their online presence, these same retailers have started to bring the Internet in-house by integrating such services as customer centric promotions at point of sale, introducing loyalty programs and member registration, facilitating digital signage, offering e-receipts via email, and self check out centers; all at the traditional POS kiosk. In fact, 95% of all sales transactions are conducted via traditional POS terminals.

Why bother with mobile POS anyway?

While it’s true that traditional POS system won’t be going anywhere soon and with good reason, mobile POS systems have allowed retailers to make great strides when it comes to efficiency and customer service, as well as customer satisfaction.

Companies have made big changes in the way they handle customer transactions in-store, thus affording faster checkout, waiting line reduction, consultative selling and more.

List of mobile POS benefits goes on:

Email Receipts – Better for the environment, more convenient for customers and faster to process, a digital purchase receipts sent via email tells the customer that you care about the earth and about them.

Expanded Reach – With mobile POS, your sales are no longer confined within the four walls of your brick and mortar store. Sidewalk sales, seasonal mall kiosks, and special sponsorship events are just a few examples of all the places you can take your retail sales to, with a POS in hand.

Inventory and Price Search – When customers can be assisted with finding an item color, size or availability on the spot, rather than having to wait in line to do so, it makes them happier. The same can be said for pricing. POS in the hands of store reps can go a long way toward customer satisfaction.

Inventory Return Stations – There is always a certain volume of returns, but that volume increases for retailers particularly after the holidays. The implementation of mobile POS allows for retailers to set up additional return stations in order to avoid long lines and customer frustrations.

Mobile POS goes Mobile – Your investment in your company POS system doesn’t need to be one size fits all, regardless of store traffic volume in one location or another. Retailers may opt to have a blow out sale in one location, thus require additional checkout power for that location for a specific period of time. With mobile POS, devises and licensing can be utilized throughout different store locations on an as needed basis.

Optional Seasonal Subscription – The great thing about mobile POS is that you needn’t pay for a POS system year round if you’re not using it year around. Seasonal spikes in retail sales warrant the additional cost of extra POS licensing and hardware, but the rest of the year your budget shouldn’t need to encompass more than what is needed. Mobile lets you better manage your overall POS investment.

Storewide Promotion Opportunities – Mobile POS has allowed retailers to drive sales in various sections of the store by holding demonstrations or promotions in different departments to tout products or services. Customers can be marketed and sold to, on the spot.

The growing industry of mobile payments doesn’t stop at in-store mobile POS. Digital wallets like Google Wallet and Apple Passbook, mobile-to-mobile cell phone transfers, Near Field Communication (NFC) payments, mobile device credit card swipe and other emerging technologies are quickly changing our cash and credit card world.

What about traditional POS?

Mobile payment systems are indeed terrific. So, when should you consider going with traditional POS? The reality is, in addition to the aforementioned benefits of traditional checkout kiosk functions, there times when mobile POS simply will not suffice.

Mobile POS is great when a customer wants to choose and pay for one item while on the sales room floor, but what about when the customer has a multitude of items? Ringing up and bagging groceries, removing anti-theft mechanisms, neatly folding and bagging clothing items and managing the sales of numerous agents, stations or departments are just a few examples of situations that often require the traditional POS checkout station.

By combining traditional POS strategies with mobile POS flexibility, retailers can leverage the command of a complex, and multi-dimensional, marketing and retail sales management system.

Posted in Credit card Processing, e-commerce & m-commerce, Electronic Payments, Internet Payment Gateway, Mobile Payments, Mobile Point of Sale, Near Field Communication, Point of Sale, Smartphone Tagged with: apple passbook, checkout station, credit card swipe, customer satisfaction, e-commerce, e-receipts via email, faster process, Google Wallet, Loyalty Programs, mobile payment system, mobile point of sale, mobile pos, mobile-to-mobile cell phone transfers, MPOS, multi-channel sales strategies, Near Field Communication, nfc, online customer service, online presence, POS, retail industry, retail sales, retail sales management system, traditional POS kiosk

August 1st, 2013 by Admin

With mobile payment services clamoring for space in the digital wallet domain movers and shakers are positioning themselves for growth opportunities presented in mobile commerce settings. Google Wallet has been live for a while but now a new player is entering the arena. ISIS is rounding the ninth month of it’s pilot program in Austin Texas, and Salt Lake City Utah using near field communications based mobile payments. AT&T Mobility, T-Mobile. and Verizon Wireless have partnered with ISIS and will be providing the electronic wallet services later this year. Read more of this article »

Posted in Mobile Payments Tagged with: Coca-Cola, contactless, Digital Wallet, Google Wallet, ISIS, mobile, near field communications, nfc