June 19th, 2014 by Elma Jane

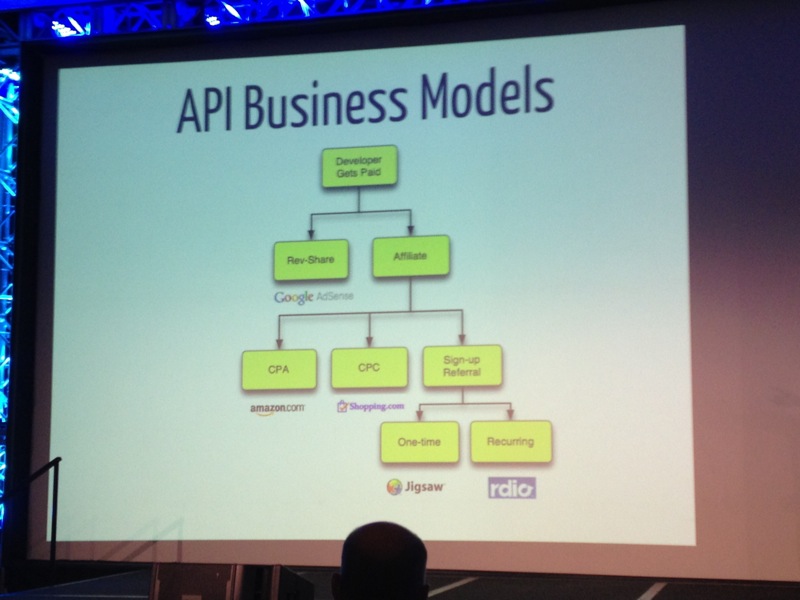

API Software Inc. has created an application ISOs can use to help merchants tabulate the best payment services deals. The Square Deal Pro app for the merchant services industry enables sales reps to compare their company’s rates to those of Square, PayPal, Stripe and other payments aggregators. Essentially, the application takes the mathematics burden off of the merchant and helps an ISO or agent compare bundled pricing with interchange-plus pricing.

Frank Haggar, a software developer, started asking merchants why they chose a certain provider and they just said the pricing was simpler. It might be more expensive, but it was easier for them to understand. That moved to develop Square Deal Pro. It’s a software that salespeople can have right on their phones and it makes a comparison and is easy to understand. Square Deal Pro, which operates on iPhones, Android devices and Windows phones, was established as a vendor-neutral tool that is also available for merchants to download if they were inclined to want to crunch numbers themselves. Service providers pay for the application and all of its sales features, but a free version for price comparisons only is available to merchants.

Merchants are experts in what they know how to do and they may not want something that includes math distracting them from that, but the sales rep can do it for them and use it along the lines of a calculator helping someone figure out mortgage rates. ISOs have various tools at their disposal and lock in key information in their brains to prepare for sales presentations, but most will likely find Square Deal Pro a valuable addition. Something that takes complicated pricing schemes and factors it all into an easy interface that puts out a clear comparison that is valuable, certainly out in the field.

API Software has to deliver something difficult or impossible to copy because that would set this permanently apart as opposed to being a lead to other similar products in the market. An ISO can change rates or make adjustments for a client if the numbers show that another provider is offering a less expensive option, but the numbers in the app don’t lie. The app will show how a bundled rate can work in your favor, such as if you are selling Girl Scouts cookies at $3 a box. Then use Square all day long, but an ISO can compare how his product works compared to others and the app can show, that at a certain time, it might be beneficial to switch over.

Square Deal Pro takes into account factors other than interchange rates, including merchant volume, average ticket price and whether transactions are keyed or swiped or both. All of those things determine where you fit in on the diagram of how your rate should be structured. There is a lot of analysis on minimal focal points. The application may also help defuse potential problems with merchants who sometimes feel their sales rep was not providing a fair assessment of pricing structure or comparisons.

As for the application’s name, Haggar doesn’t want any confusion over whether this might be a new Square product.

Posted in Best Practices for Merchants Tagged with: account, aggregators, Android, assessment, bundled pricing, developer, devices, interchange, interchange rates, interchange-plus pricing, iPhones, ISOs, market, merchant services, merchant volume, Merchant's, mortgage rates, payment, PayPal, phones, pricing, Pro app, products, provider, Rates, sales, Service providers, software, Square, Square Deal Pro app, Stripe, transactions, Windows phones

March 3rd, 2014 by Elma Jane

Interchange is a word that’s talked about a lot in the payments industry. If you didn’t have to pay interchange fees, what would your business spend the money on? At its most basic, interchange is the fees businesses pay to credit card processors to swipe your credit and get paid – or the cost of moving money. Businesses are sick and tired of paying high fees and getting very little in return. Customers are sick and tired of seeing prices of items tick upwards as businesses are forced to charge more to cover the cost of interchange.

Businesses spend an exorbitant amount of money each year to accept credit cards – to the tune of $50B. Businesses could reinvest the money they’ve been spending on interchange to better connect with customers, enhance marketing initiatives and grow faster and smarter. Just imagine for a second the economic stimulus the country would get if all that money was put back into the business to drive growth, or back into the pockets of customers to lower costs.

In the past 30 years, interchange fees have mainly gone in only one direction: up. Luckily, things are starting to change, and I think we’re going to start seeing interchange being driven down. The days of a 3 -or 4-percent interchange rate are beginning to look numbered and here’s why:

Competition

There are nearly 200 players in the mobile payments space, with more entering daily. New opportunities are providing businesses with alternative payment options that are outside of Mastercard and Visa’s clutches. While there might be 1,000-plus credit card processing companies, they’re all based on the Mastercard/Visa rails, which provides a fixed floor. But not so with many of these new payment options. As such, traditional methods of payment (cash, credit cards) are facing an increasing amount of competition, and merchants are starting to pay attention.

It’s unlikely that cash and credit cards are going away anytime soon, but it only takes a small shift in volume (maybe 5 percent) for the card issuers to start paying attention. There are a number of ways for them to react, but if history is any guide, one of them will be to start lowering their prices. Alternatively, they could find ways to offer more value to their merchants. Either way, competition is offering merchants new ways to accept payments, and this will lower fees over time.

Innovation

The second thing driving down costs for merchants is rapid innovation, and like a good deal of innovation these days, much of it is centered around mobile. Mobile payments are starting to gain significant traction among consumers, accounting for $640M in 2012 and expected to have grown by an additional 234 percent in 2013.

QR codes, NFC, peer-to-peer payments, card emulation – the list of new technologies trying to disrupt the payments space goes on and on. These new alternatives are challenging the current payments system and shedding light on the opportunities for businesses. This innovation is beneficial in two ways. The first, as discussed above is that more competition will naturally drive costs down. The second is that alternative payment options are focusing on value beyond the transaction.

There are new payment options out there that provide tangible information, such as data analytics, which help companies drive sales and increase revenues. New options are allowing small businesses access to the same technology and analytics that were previously reserved for big-box retailers or e-commerce sites only. These additional value propositions not only help businesses, they also provide new ways for payments companies to monetize, removing the need for them to make all of their money from interchange. With two (or more) revenue lines, lowering interchange is suddenly a lot more feasible.

Legislation

The Durbin Amendment is designed to introduce competition in the debit card processing network and limit fees for businesses. For all of its unintended consequences, Durbin legislation is actually helping to drive down interchange; it’s opening up competition for non-card-brand network players and lowering debit card fees. While it is certainly rife with controversy, this amendment is opening up new ways to move money that will, over time, contribute to a less expensive payment processing ecosystem.

Merchant demand

Business owners are smart and savvy. They pay attention to trends, focusing on finding new ways to set their business apart. Business owners are also conscious of ROI, and how much they’re spending to attract and retain customers. They understand there is some cost to accept payments, but are becoming more and more frustrated at the high swipe fee costs from traditional credit card processors and minimal return for those fees.

Businesses are looking to new, innovative solutions to provide more than just payment processing – they want to understand and better connect with their customers. In short, merchants are ready for a new payments ecosystem, and where there’s this much demand from a group this big and influential, a solution can’t stay away for too long.

Interchange rates are not going away entirely in the near future, although it will happen eventually. A lot of powerful wheels are in motion to significantly reduce the interchange rates that merchants currently pay. Right now the impact might be small, but it’s growing quickly. In a few years, 3- to 4-percent interchange could be relegated to the same bit of history as $1.99 international phone calls.

Posted in Credit card Processing, Electronic Payments, Financial Services, Gift & Loyalty Card Processing, Internet Payment Gateway, Small Business Improvement Tagged with: accept credit cards, accept payments, alternative payment, credit card processing, credit card processors, credit cards, debit card processing network, e-commerce, interchange, interchange fees, interchange rates, lowering debit card fees, lowering interchange, Merchant's, Mobile Payments, payment processing, payments, payments industry, swipe your credit card