September 14th, 2015 by Elma Jane

The security rules for fraud liability of credit and debit cards will change in the United States, starting October 1, 2015.

The new security rules would prompt major plastic card brands like MasterCard and Visa to upgrade their magnetic stripe based cards to more modern and secure chip technology based cards.

Credit and debit card fraud amount in the U.S. reached around $11.27 billion, in 2012.

With the new rules, any financial institution and payment processing merchant who would not upgrade their cards to chip technology would be held responsible for any committed fraud with their cards instead of their customers. This new rule would effectively transfer the liability in case of a fraud from the consumer to the least secure card provider. The rule specifically says that liability will fall on the bank or retailer with the least secure technology.

If the bank has not given you a new chip card, and you use your magnetic swipe card and there’s resulting fraud, the bank will be responsible for that.

All merchants who do not offer payment terminals that support chip based cards would be held liable for any fraud committed on their premises as well, from October 1. The new rules say that if the card is chip based and the merchants fail to offer a chip based terminal, and a fraud is committed, they would be held liable instead of the card holder.

With chip based cards, the customer would need to insert their card inside a chip enabled payment terminal while making a purchase. Then, they need to confirm the amount and enter a private pin to verify their identity. The customer would also sign for the purchase like using a regular magnetic card.

Besides MasterCard, Visa has already rolled out the new chip based terminals in the U.S. under its Zero Liability Policy.

The chip based cards are more secure compared to the old magnetic technology. That is one of the reasons why the new rules are promoting the chip based technology over the 55 years old magnetic cards.

Not all merchants have to replace their old magnetic terminals and it is still an optional decision, but industry analysts think that the shift of liability in case of fraud from consumers to financial institutions and merchants would likely prompt them to start using chip based technology.

Posted in Best Practices for Merchants, Credit Card Security Tagged with: bank, card holder, card provider, chip card, debit cards, magnetic swipe, magnetic terminals, merchants, payment processing, payment terminals

September 3rd, 2015 by Elma Jane

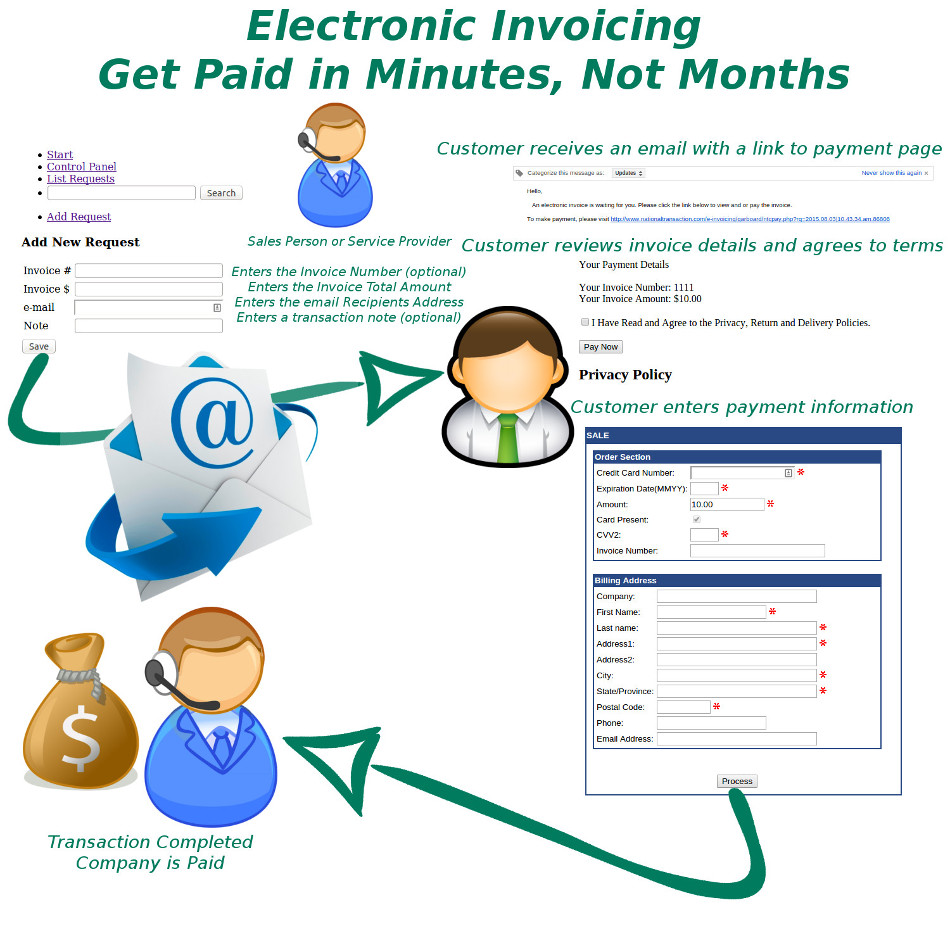

Today, there are numbers of dedicated invoicing software solutions to choose from, but also, specifically built to handle all aspects of invoicing. Whether you send out invoices in the mail, electronically or both. NTC’s Cloud-based invoicing software is a way to simplify your invoicing processes.

National Transaction help merchants consider making the switch to online invoicing methods.

If you’re considering making the transition, check National Transaction’s Electronic Invoice.

Once the transaction is approved a confirmation email is sent to the merchant and consumer.

Benefits of Electronic Invoicing:

Ease of use – Merchants only needs to enter the email address and the amount of sale to complete order.

Better security – Card Holder enters credit card data directly into an acquiring bank system. Bank stores such sensitive information in an encrypted format on remote servers. This reduces your liability and makes it so you won’t lose all your important data if your server gets hacked or destroyed.

Collect useful sales information – Most invoicing software has reporting capabilities which let you track payments, projected income and client history.

Get paid faster – E-Invoice can be paid the same day. The sooner you send your invoices, the sooner you are likely to get paid. With NTC Electronic Invoice, you can schedule invoices to be sent out ASAP, which means faster, more reliable income for your business.

Look more professional – Invoicing software typically includes professional-looking invoice templates, which you can customize with your business name and logo.

Emailing clients invoices instead of mailing them printed bills, is approximately 10 times cheaper than paper invoicing.

Send invoices from anywhere – Cloud-based invoicing software can be accessed from anywhere with an internet connection. This means you can easily invoice customers or access your business’s billing information wherever you are in the world, and even from your phone if you need to.

Interested in Electronic Invoicing? Give us a call 888-996-2273 or go to our website www.nationaltransaction.com

Posted in Best Practices for Merchants Tagged with: bank, card, card data, credit card, Electronic Invoice, invoicing, merchants

August 17th, 2015 by Elma Jane

It can be hard to see the benefits of accepting credit cards for some startups and small business merchants – especially if the business has been cash only since opening day. However, there is a big downside to being cash only and you could really be limiting the customers you bring in.

While cash is the simplest form of payment, but it’s not always the best form of payment for small businesses.

Some consequences of accepting cash only.

- Being cash only can mean you will need to do additional paperwork come tax time. You must file Form 8300, Report of Cash Payments over $10,000 Received in a Trade or Business, if your business receives more than $10,000 in cash from one buyer as a result of a single transaction or two or more related transactions. This same rule applies to cash equivalents including traveler’s checks, bank drafts, cashier’s checks and money orders. The form does require that you have your customer’s name, address and social security number.

- Credit cards and debit cards are very popular; in fact, most people only carry a small amount of cash or no cash at all. Because of this, being cash only can cause your business to lose both existing and potential customers. A cash only policy can make them feel inconvenienced and cause them to take their business elsewhere.

- If your customers don’t have the cash to purchase an item they want from your business, then they are more likely to walk away from the purchase.

- Keeping a large sum of cash at your business can put you at an increased security risk. It can also increase the amount of time you will spend at your business managing finances because of the time it can take to count cash and change.

If your Business is ready to accept credit cards give us a call 888-996-2273 or go to our website www.nationaltransaction.com

Posted in Best Practices for Merchants Tagged with: bank drafts, cash, cashier’s checks, credit cards, debit cards, merchants, money orders, payment, transactions, traveler’s checks

August 13th, 2015 by Elma Jane

The credit card processing industry, have been working towards including EMV technology in all of the point of sale systems.

Many processors have sent out EMV capable devices that will need to be adjusted before they can start accepting EMV card transactions.

See which category you fall into so you are prepared when October 1 rolls around.

First, check and see if your credit card machine has the slot to accept EMV cards (it’s either a slot in front, or on the top of, the unit). If you don’t, you need to contact your processors or sales agent to update your equipment .

If you do have the slot for EMV cards, you’ll need to contact National Transaction to see if your EMV capable machine has been enabled to accept EMV cards.

What is the difference between EMV capable and EMV enabled?

- EMV Capable – EMV capable means that your credit card machine is equipped with the hardware (i.e. the slot) and has the capability to do a transaction, but first you’ll have to update the application to enable you to process the cards. At National Transaction, we have a support specialist to assist you with step-by-step instructions to switch your credit card Point-of-Sale System, from EMV capable to EMV enabled.

- EMV Enabled – When your machine is EMV enabled, your terminal is ready to accept EMV transactions. According to MasterCard, 73 percent of consumers say owning a chip card would encourage them to use their card more often. In addition, 75 percent of consumers expect to use their chip card at the merchants where they shop today. Keeping these numbers in mind, it only makes sense to equip your business with an EMV enabled credit card POS system.

What makes EMV technology so important?

EMV is a global payment system that adds a microprocessor chip into credit cards and debit cards, and reduces the chance a transaction is being made with a stolen or copied credit card. Unlike traditional magnetic-stripe cards, anytime you use an EMV card, the chip in the card creates a unique transaction sequence that can’t be replicated. Because the number will never be valid again, it makes it hard for hackers to fake these cards. If they attempt to use the copied EMV card, the transaction would be denied.

The rollout of EMV technology is ongoing, but even with the October 1 deadline, it’s estimated that only 70 percent of credit cards and 40 percent of debit cards in the U.S. will support EMV. Despite these numbers, that doesn’t mean you shouldn’t update your equipment.

Following the deadline, card present fraud liability will shift to whoever is the least EMV compliant party in a fraudulent transaction.

Make sure that’s not you!

Posted in Best Practices for Merchants, Credit card Processing, Credit Card Reader Terminal, Credit Card Security, EMV EuroPay MasterCard Visa, Point of Sale Tagged with: card present, card transactions, chip, chip card, credit card, credit card processing, debit cards, EMV, EMV capable, EMV enabled, emv technology, magnetic stripe cards, merchants, payment system, point of sale, POS, processors, terminal

July 28th, 2015 by Elma Jane

The annual ASTA Global Convention is set to take place in Washington, D.C., August 29 to September 2, 2015.

A conference that is designed for all travel merchants, whether they are home, office or storefront-based.

American Society Of Travel Agents (ASTA) plays such a vital role in government lobbying and regulation, travel agent awareness and education.

This year’s convention will feature a full roster of speakers, educational seminars, networking events and local sightseeing.

ASTA Global Convention will feature pre-convention events including the chance to see a Washington Nationals baseball game, special tours of Washington, D.C. and the annual ASTA Advocacy Dinner.

The convention will take place at the Omni Shoreham Hotel near Georgetown. Hotel rates start at $169, booking with the dedicated room block ends August 7.

ASTA registration rate will increase on August 1 by $25.

For more information or to register, click on ASTA Global Convention.

Posted in Best Practices for Merchants, Travel Agency Agents Tagged with: merchants, travel, travel merchants

July 23rd, 2015 by Elma Jane

The digital payments landscape is changing at a rapid pace. Consumers are finally adopting digital wallets, like Apple Pay and Android Pay.

The deadline for merchants to become EMV compliant, the global standard that covers the processing of credit and debit card payments using a card that contains a microprocessor chip, is quickly approaching.

Today’s consumers show an increasing desire to use new payment methods because they’re convenient. However, this presents a challenge to merchants, as many have not made the switch to the modern technology required to accept these methods since they’re generally hard-wired to resist technology changes.

Merchants must evolve with technology or they’ll find themselves unable to compete and in danger of losing customers.

Looking long term, the benefits of adopting new payment technology will outweigh the cost of transitioning. The fact is that new payment technology will reduce fraud risk due to counterfeit cards, provide greater insight into shoppers with sophisticated data and will ultimately lower costs for merchants over time.

The value merchants will get out of new payment methods:

Security

Investing in new payment technology will help reduce the risk of fraud. EMV, as an example. Beginning in October 2015, merchants and the financial institutions that have made investments in EMV will be protected from financial fraud liability for card-present fraud losses for both counterfeit, lost, stolen and non-receipt fraud.

EMV is already a standard in Europe, where fraud is on the decline. In turn, American credit card issuers are being pressured to replace easily hacked magnetic strips on cards with more secure “chip-and-PIN” technology. Europe has been using Chip, and Chip & Pin for years.

There’s nothing that can guarantee 100 percent security, but when EMV is coupled with other payment innovations, like tokenization that separate the customer’s identity from the payment, much of the cost and risk of identity theft is eliminated. If hackers get access to the token, all they get is information from one transaction. They don’t have access to credit card numbers or banking accounts, so the damage that can be done is minimal.

As card fraud rises, there’s a strong case to upgrade to a payment system that works with a smartphone or tablet and accepts both EMV chip cards and tokens.

Insight into Customer Behavior

In addition to added security, upgrading to new payment technology opens up a door to greater customer insights, improved consumer engagement and enables merchants to grow revenue by providing customers with receipts, rewards, points and coupons. By collecting marketing data at the point of sale a business can save on that data that they only dreamed of buying.

Investment Outweighs the Cost

New technology does have upfront costs, but merchants need to think about it as an investment that will grow top-line revenue. Beware of providers offering free hardware. Business can benefit by doing some research on the actual cost of the hardware.

By increasing security, merchants are further enabling mobile and emerging technologies, which will make shopping easier.

Customers will also be more confident in using their cards.

As an added bonus to merchants, most EMV-enabled POS equipment will include contactless technology, allowing merchants to accept contactless and mobile payments. This will result in a quicker check-out experience so merchants can handle more transactions.

Faster customer checkout.

The best system for is the one that makes the merchant as efficient and profitable as possible, as well as improves the customer checkout experience.

Retail climate is competitive, merchants have two choices:

Do nothing or embrace the fact that payments are changing. Transitions from old systems to new ones require work and risk, but merchants who use modern technology are investing in the future and will certainly outperform those who choose to do nothing.

Posted in Best Practices for Merchants, EMV EuroPay MasterCard Visa, Mobile Payments, Near Field Communication, Point of Sale Tagged with: American credit card, card, card present, chip, Chip and PIN, contactless technology, credit, data, debit card, digital payments, Digital wallets, EMV, EMV compliant, EMV EuroPay MasterCard Visa, merchants, Mobile Payments, payment innovations, payment methods, payment technology, payments, point of sale, POS, provider's, smartphone, tablet, token, tokenization, transaction

June 25th, 2015 by Elma Jane

A product or service using a credit card or debit card should be efficient, fast and most importantly safe. There are a lot of regulations in place to make sure that the processing of payments using a card is safe and secure. One of the way is the EMV (Europay, MasterCard and Visa) technology, where payment cards used in an ATM and POS Terminals have been embedded with microchips. This form of payment technology has long been in use and is widely accepted in many regions such as Europe, Canada and Asia Pacific. The US, which is considered to be the largest number of plastic card users is one of the countries that have not yet fully optimized this otherwise global standard.

Advantages Of EMV – EMV embedded chip is a lot more secure than the traditional magnetic stripe, especially when it comes to face-to-face credit/debit card transactions. Credit card fraud is rampant, but using this embedded chip has added another layer of protection against consumer fraud. Once the card has been inserted into a terminal, the payment will then be authenticated and processed using the EMV network. The chip within the card is hard to duplicate.

What Does This Mean For Your Business? – You will create more credibility and garner more customers in the market place by utilizing this more safe and secure payment method. There will be increased in consumer confidence.

What Happens When You Don’t Upgrade? – There is a Liability Shift. Currently, If a payment processing transaction has been approved and it turns out to be fraud, it’s the card issuer loss. With the new rule, liability shifts to merchants who has not implemented the EMV technology. When fraud happens, the responsibility falls on the business owner who makes the transaction.

How To Prepare Your Business For EMV? – Upgrade your terminal. Contact National transaction and we’ll help you prepare your business for the EMV migration.

Upgrading your current payment processing system is easy with NTC.

Give Us A Call Now! 888-996-2273

Check our website http://nationaltransaction.com click Demos and Videos to learn more!

Posted in Best Practices for Merchants, Credit card Processing, Credit Card Reader Terminal, Credit Card Security, EMV EuroPay MasterCard Visa, Point of Sale Tagged with: atm, card, chip, credit card, Credit card fraud, debit card, Debit Card transactions, EMV, EMV migration, EMV network, EuroPay, magnetic stripe, MasterCard and VISA, merchants, microchips, payment, payment cards, payment processing, payment technology, payments, POS terminals, terminal

June 15th, 2015 by Elma Jane

Merchants Provided Access to Digital Payments Innovations for Store-Branded Cards through Partnerships with Synchrony Financial and Citi Retail Services

Purchase, NY – June 15, 2015 – MasterCard today became the first payment network to provide tokenization services to private label (store-branded) credit card issuers, enabling merchants to take advantage of the latest digital payment innovations. BJ’s Wholesale Club, Kohl’s and JCPenney will be among the first retailers to bring mobile payments to their private label cardholders later this year. The company also announced partnerships with some of the largest private label credit card issuers in the U.S., including Synchrony Financial and Citi Retail Services, to enable consumers to use their eligible credit cards within participating mobile payment and digital wallet services.

According to Equifax’s National Consumer Credit Trends Report, the number of open retail credit card accounts exceeded the 195 million mark by the fall of 2014. As the only network to offer private label support for wallet service offerings, MasterCard continues to enable consumers to pay when, where and how they want – and on the device of their choice.

Tokenization support for private label issuers is made possible through the MasterCard Digital Enablement Service (MDES), which enables a connected device to be securely used for everyday shopping and payments. MDES supports contactless (NFC) payments with a mobile device at a physical point of sale, as well as from within a mobile app. Transactions are secured using industry-standard EMV cryptography and take full advantage of the most secure payments technology in the world.

“Thanks to our ongoing innovation and strategic partnerships, we are helping shape the future of how private label credit cards work in whichever digital wallet customers choose,” said Margaret Keane, president and CEO of Synchrony Financial. “It was recently announced that our retail partner, JCPenney, will be among the first to offer its private label credit cardholders the ability to checkout with Apple Pay later this year. We are committed to working with our retail partners, MasterCard, and key payments industry players to preserve the benefits of our private label credit cards and patented Dual Cards in third-party digital wallets.”

“We’re seeing significant momentum and innovation around digital wallets, and a key focus for MasterCard is that consumers can leverage these new offerings safely and securely. MDES was developed to ensure that any connected device can be used to make purchases, and deliver the simplicity, security and convenience people have become accustomed to when using a MasterCard account of their choice,” said Ed McLaughlin, chief emerging payments officer, MasterCard. “MasterCard is helping merchants capitalize on mobile payments, ensure the best possible consumer experience for their consumers and encourage both repeat business and customer loyalty.”

Since the announcement of MDES in 2013, millions of MasterCard accounts have been tokenized for use in popular digital wallet services. MDES currently provides tokenization services for credit, debit, co-brand, prepaid and small business cards, with private label tokenization beginning in the third quarter of this year.

Posted in Best Practices for Merchants Tagged with: credit cards, digital paymets, Digital wallets, merchants, Mobile Payments, payment network, technology innovation, tokenization

June 5th, 2015 by Elma Jane

Traditionally, travel-related merchants have a difficult time obtaining merchant accounts. National Transaction Corporation (NTC) is a full service merchant account provider with extensive experience in the travel arena and related markets, servicing thousands of travel-related merchant accounts by specializing in non-cash electronic transactions. Our services include processing credit card transactions, gift card transactions, and e-commerce transactions, among others. We offer a full line of products including credit card terminals, cellular devices, supplies, and accessories for each model sold. We offer aggressive rates and pricing for mail/telephone order, retail/restaurant, wireless, and online transactions while specializing in the travel and high volume sectors of merchant processing, and we are proud to be the preferred merchant provider for ASTA.

NTC is dedicated to providing the highest caliber of service and solutions in the merchant processing industry. We actually answer the phone when you need assistance! NTC has a team of dedicated employees providing personalized service to each account holder and are available directly through their toll free number, never hidden behind a menu system. Our excellent service truly separates us from everyone else in the industry. The principals of NTC have extensive experience in the processing arena for over 25 years, with experience in all facets of operation, including credit cards, credit initiation, credit investigation, loss prevention, deployment, and customer and terminal support. We employ internal sales associates as well as independent sales agents who offer many opportunities through their referral reward services and Independent Sales Organization (ISO) programs.

NTC’s online gateway allows for processing transactions, reviewing account history, and interacting with various shopping cart and accounting applications such as QuickBooks, Peachtree, and many other titles. Reservation software such as Trams are compatible and integrate well with all National Transaction merchant accounts. Whether you are a travel agency or an independent agent, we offer many solutions that cater to the travel industry and will increase your revenue with quicker deposits into your bank account.

Travel environments are unique in that your transactions are usually keyed; there is almost always a delayed delivery period, and large ticket transactions are not uncommon since one card holder may be paying for multiple tickets. They also tend to be seasonal, with peak season months generating an unusual spike in their “average” monthly volume, and charge-back’s pose a potential threat by travelers who are unable to complete their trip. Combine even a few of these factors together and you have cause for a reserve, or even account termination. National Transaction Corp specializes in understanding what makes your transactions unique, as a travel agent, and how they affect your merchant account.

The importance of customer service is something that is over looked when merchants compare the overall cost of monthly fees with their merchant account. That is, until the moment they need assistance with their account. Whether searching for missing deposits, having problems processing transactions, issuing refunds, processing voids, or questioning their billing statement, a merchant should always remember you get what you pay for. If you wonder why they can offer you no monthly fee, they are offering you no LIVE customer support. Customer support for them will come via means of email. You will wait hours for answers, and even days for a simple confirmation or general email, let alone a resolution.

National Transaction Corporation has over 17 years of dedication and experience in providing quality solutions in the credit card processing arena. From internet e-commerce applications to food stamp processing, from small start up businesses to fortune 500 companies, NTC has a complete product selection to customize a solution to grow with your business. We at NTC pride ourselves on being a full service, member service provider. It is our mission to provide the same dedication and service in maintaining your business as you experience in us earning your business. NTC will provide service after the sale. It is that service that sets us apart! For more information, contact NTC for world class service and solutions.

Contact National Transaction Corporation today at 888-996-2273 to see how we can help you with your travel merchant account, or visit us online at www.nationaltransaction.com for more information.

by Elizabeth Cody (Travel Research Online)

Posted in Best Practices for Merchants, Credit card Processing, e-commerce & m-commerce, Gift & Loyalty Card Processing, Merchant Account Services News Articles, Merchant Cash Advance, Travel Agency Agents Tagged with: ASTA, bank account, billing statement, credit card terminals, credit card transactions, credit cards, customer service, deposits, e-commerce, e-commerce transactions, electronic transactions, gift card transactions, Independent Sales Organization, ISO, merchant account provider, merchant accounts, merchants, service provider, travel, travel agency, travel agent, travel industry

May 28th, 2015 by Elma Jane

No such thing as FREE, but with National Transaction, Customer Relationship Management Software can be! Take advantage of technology and use it for your business success.

What is CRM? Customer relationship management is a system for managing a company’s interactions with current and future customers. It often involves using technology to organize, automate and synchronize sales, marketing, customer service and technical support.

Free CRM comes in two categories: FREE, but limited, and OPEN SOURCE.

Free, but limited versions – set caps on the amount of free users, contacts, storage, extra features, or some combination.

Open source – offers an unlimited, fully functional CRM to users, is extremely customizable. Most open source CRM companies also offer a preconfigured version and/or installation and support for a price.

There are a whole host of affordable CRM options you should be considering even though not free, may be the perfect fit for your organization.

Each CRM system is different and each one will serve some companies better than others. CRM is a category that’s very rich in free and open source programs.

Why is the value of CRM great for Merchants?

It allows you to register your leads and contacts. You need some basic categories to make your data efficient so that you can implement your CRM strategy to fulfill their needs. With a CRM you can store and manage hundreds of clients and let a computer system handle the task of memory and recall.

You can track all customer interaction – A customer relations management system put all the pertinent client information in one central location that was easy to update and easy to see when other’s updated. All communication can be kept in one spot, nothing gets lost and you can now see and share with the rest of your team. This history builds a long-time relationship. Emails should be in your system, and not in each person’s mailbox.

Every time you make a call, send an email, or contact that customer or prospect you can update your CRM with their current status.

It reveals possibilities. Most companies keep their current supplier until they are ignored. That’s why keeping them alive and kicking in your CRM database is so important. And if you have an opt-in newsletter or a great seminar plan, their business might be yours for the next quarter.

It makes your most valuable asset – the customer data – remain. People change jobs. Have you ever experienced someone leaving you, and nothing is left behind? The pipeline wasn’t up to date. The contacts wasn’t updated. The important contacts wasn’t registered – because all relevant information was stored locally. Don’t let it happen. Customer relations systems help keep all conversations in one place and make it easy for you to quickly look back in time and see how things have progressed. See for yourself the progression of a client and their communication as well as your company’s notes and responses. You’ll be able to save more customers from leaving by catching something you would have otherwise missed, and you can learn from your history.

Posted in Best Practices for Merchants Tagged with: crm, CRM database, customer data, customer service, data, database, merchants, open source