January 21st, 2016 by Elma Jane

HYATT DATA BREACH HITS 250 HOTELS WORLDWIDE

Hyatt hotel company noted that the breach that occurred over the course of almost four months hit 250 different hotels over the span of about 50 countries.

The breach covered payment card data from the cards used at various Hyatt hotels in that range of dates, reports note, and most of the breaches seem to have hit at hotel restaurants. Those who also hit the spas at Hyatt, along with front desks, gold shops, and even parking structures may also have been impacted by the breach.

The company couldn’t confirm how long the network was vulnerable nor if any payment card data had actually been stolen.

Perimeter Defense where data is protected with passwords and firewalls and the like is fine and well, but more needs to be put into protecting the data in the event someone clears security.

Encrypting Data is a great step to take, assuming someone manages to clear the perimeter, the encryption makes the data itself much more difficult to access and use. So while perimeter defense keeps unauthorized users away from data, encryption keeps those who reach the data from being able to readily read it.

Data Security is something none of us can take for granted, so doing what we can to protect that data being vigilant about statements, putting up proper security, encrypting data all of these contribute to better protected data and a safer time online.

Posted in Best Practices for Merchants, Travel Agency Agents Tagged with: card data, cards, data, online, payment, Security

January 19th, 2016 by Elma Jane

2015 was a major period of growth for the online and mobile payment industry. Close to 60 million Americans used mobile payments on a consistent basis, representing close to 18 percent of the population. However, around 52 percent of Americans are aware of mobile payments and how to use them.

Because of both the wide awareness and accessibility of mobile payments, analysts expect consistent mobile payment use to double this year. Millennials and high-income spenders tended to adopt the technology more quickly, at 23 percent and 38 percent consistent usage respectively.

Even more intriguing than the wide-spread use of mobile payments is how large the market grew. In 2015, $8.71 billion passed through online payment services providers. Even more intriguing is the prediction that this market will more than triple to $27.05 billion by the end of this year.

Posted in Best Practices for Merchants Tagged with: mobile payment, online, online payment, payment, payment industry, payment services, provider's, services providers

September 16th, 2014 by Elma Jane

When plastic cards become digital tokens, they become virtual. So how do you say that the Card is Present or Not Present. The legendary regulatory difference that the cards industry has relied on to differentiate between interchange fees for Card Present and Card Not Present transactions.

Apple secured Card Present preferential rates for transactions acquired by iTunes on the basis that the card’s legitimacy is verified with the issuer at the time of registration and the token minimizes probability of fraud. If an API call to the issuing bank is sufficient to say that the Card is Present, who is to say that the same logic can’t apply to online merchants who also verify the authenticity of Cards on File when they tokenize them? How can one arbitrarily say that the transaction processed with token from an online merchant is Card Not Present, but the one processed with Apple Pay is Card Present even though both might have made the same API call to the bank to verify the card’s validity?

In the Apple case, a physical picture of the card is taken and used to verify that the person registering the card has it. It is not that hard for an online merchant to verify that the Card on File converted as a token does belong to the person performing an online transaction.

As we move towards chip and pin the card present merchants will spend substantial money upgrading their hardware and POS systems. That expense will be offset by that savings in losses due to fraud. MOTO and e-commerce transactions ( card NOT present ) will always have a higher cost because the nature of processing is NON face to face transactions. Of course the fraud and losses are higher when the card is manually entered or given to someone over the phone……Face to face will always have the lowest cost per transaction because it is usually the final step in the sale. Restaurants are low risk because you had the transaction AFTER you eat. If there is a dispute it happens before the merchant even sees the credit card.

In the long run, as cards become digital and virtual through tokens, we are all going to wonder if card is present or not present. May be some will say. Card is a ghost.

Posted in Best Practices for Merchants, Credit card Processing, EMV EuroPay MasterCard Visa, Visa MasterCard American Express Tagged with: (POS) systems, API call, Apple secured Card Present, bank, Card Not Present transactions, card present, card present merchants, cards, cards industry, chip, credit-card, digital and virtual, digital tokens, e-commerce transactions, fees, fraud, hardware, industry, interchange, interchange fees, issuer, issuing bank, low risk, Merchant's, moto, NON face to face transactions, online, online merchants, online transaction, PIN, Processing, Rates, token, transactions

September 10th, 2014 by Elma Jane

If your businesses considering an iPad point-of-sale (POS) system, you may be up for a challenge. Not only can the plethora of providers be overwhelming, but you must also remember that not all iPad POS systems are created equal. iPad POS systems do more than process payments and complete transactions. They also offer advanced capabilities that streamline operations. For instance, they can eliminate manual data entry by integrating accounting software, customer databases and inventory counts in real time, as each transaction occurs. With these systems, you get 24/7 access to sales data without having to be in the store. The challenge, however, is knowing which provider and set of features offer the best iPad POS solution for your business. iPad POS systems vary in functionality far more than the traditional POS solutions and are often targeted at specific verticals rather than the entire market. For that reason, it’s especially important to compare features between systems to ultimately select the right system for your business.

To help you choose a provider, here are things to look for in an iPad POS system.

Backend capabilities

One of the biggest benefits of an iPad POS system is that it offers advanced features that can streamline your entire operations. These include backend processes, such as inventory tracking, data analysis and reporting, and social media integration. As a small business, two of the most important time saving and productivity-boosting features to look for are customer relationship management (CRM) capabilities and connectivity to other sales channels. You’ll want an iPad POS that has robust CRM and a customizable customer loyalty program. It should tell you which products are most and least frequently purchased by specific customers at various store locations. It should also be able to identify the frequent VIP shoppers from the less frequent ones at any one of your store locations, creating the ultimate customer loyalty program for the small business owner. If you own an online store or use a mobile app to sell your products and services, your iPad POS software should also be able to integrate those online platforms with in-store sales. Not only will this provide an automated, centralized sales database, but it can also help increase total sales. You should be able to sell effortlessly through online, mobile and in-store channels. Why should your customers be limited to the people who walk by your store? Your iPad POS should be able to help you sell your products through more channels, online and on mobile. E-commerce and mobile commerce (mCommerce) aren’t just for big box retailers.

Cloud-based

The functions of an iPad POS solution don’t necessarily have to stop in-store. If you want to have anytime, anywhere access to your POS system, you can use one of the many providers with advanced features that give business owners visibility over their stores, its records and backend processes using the cloud. The best tablet-based POS systems operate on a cloud and allow you to operate it from any location you want. An iPad POS provider, with a cloud-based iPad POS system, businesses can keep tabs on stores in real time using any device, as well as automatically back up data. This gives business owners access to the system on their desktops, tablets or smartphones, even when not inside their stores. Using a cloud-based system also protects all the data that’s stored in your point of sale so you don’t have to worry about losing your data or, even worse, getting it stolen. Because the cloud plays such a significant role, businesses should also look into the kind of cloud service an iPad POS provider uses. In other words, is the system a cloud solution capable of expanding, or is it an app on the iPad that is not dependent on the Internet? Who is the cloud vendor? Is it a premium vendor? The type of cloud a provider uses can give you an idea about its reliability and the functions the provider will offer.

Downtime and technical support

As a small business, you need an iPad POS provider that has your back when something goes wrong. There are two types of customer support to look for: Downtime support and technical support.

iPad POS systems are often cheaper and simpler than traditional systems, but that doesn’t mean you can ignore the product support needs. The POS is a key element of your business and any downtime will likely result in significant revenue loss. You could, for instance, experience costly downtime when you lose Internet connectivity. iPad POS systems primarily rely on the Web to perform their core functions, but this doesn’t mean that when the Internet goes down, your business has to go down, too. Many providers offer offline support to keep your business going, such as Always on Mode. The Always on Mode setting enables your business to continue running even in the event of an Internet outage. Otherwise, your business will lose money during a loss of connectivity. Downtime can also happen due to technical problems within the hardware or software. Most iPad POS providers boast of providing excellent tech support, but you never really know what type of customer service you’ll actually receive until a problem occurs.

Test the friendliness of customer service reps by calling or emailing the provider with questions and concerns before signing any contracts. This way, you can see how helpful their responses are before you purchase their solution. Your POS is the most important device in your store. It’s essentially the gateway to all your transactions, customer data and inventory. If anything happens to it, you’ll need to be comfortable knowing that someone is there to answer your questions and guide you through everything.

Grows with your business

All growing businesses need tech solutions that can grow right along with them. Not all iPad POS systems are scalable, so look for a provider that makes it easy to add on more terminals and employees as your business expands. Pay attention to how the software handles growth in sales and in personnel. As a business grows, so does it sales volume and the required software capabilities. Some iPad POS solutions are designed for very small businesses, offering very limited features and transactions. If you have plans for growth, look for a provider that can handle the changes in transactions your business will be going through. Find out about features and customization. Does the system do what you want it to do? Can it handle large volume? How much volume? What modules can you add, and how do you interface to third parties? You should also consider the impacts of physical expansion and adding on new equipment and employees. If there are plans in the future for you to open another store location, you’ll need to make sure that your point of sale has the capabilities of actually handling another store location without adding more work for you. If you plan on hiring more employees for your store, you’ll also want to know that the solution you choose can easily be learned, so onboarding new staff won’t take up too much of your time.

Security

POS cyber attacks have risen dramatically over the past couple of years, making it more critical than ever to protect your business. Otherwise, it’s not just your business information at risk, but also your reputation and entire operations. iPad POS system security is a bit tricky, however. Unlike credit card swipers and mobile credit card readers that have long-established security standards namely, Payment Card Industry (PCI) compliance — the criteria for the iPad hardware itself as a POS terminal aren’t quite so clear-cut. Since iPads cannot be certified as PCI compliant, merchants must utilize a point-to-point encryption system that leaves the iPad out of scope. This means treating the iPad as its own system, which includes making sure it doesn’t save credit-card information or sensitive data on the iPad itself. To stay protected, look for PCI-certified, encrypted card swipers.

Posted in Best Practices for Merchants, Mobile Point of Sale, Point of Sale Tagged with: (POS) systems, accounting, app, business, card, cloud-based, credit, credit card readers, credit-card, crm, customer, customer relationship management, customer support, data, data analysis, database, desktops, e-commerce, inventory, iPad Point-Of-Sale, loyalty program, mcommerce, mobile, mobile app, mobile commerce, online, online platforms, Payment Card Industry, payments, PCI, platforms, POS, POS solution, products, sales, Security, security standards, services, Smartphones, social media, software, tablets, terminal, transactions, web

August 28th, 2014 by Elma Jane

Merchants are still using pedestrian passwords that crooks can easily break, security company Trustwave has found. Of the nearly 630,000 stored passwords that Trustwave obtained during penetration tests in the past two years, its technicians were able to crack more than half in just a few minutes and 92% within 31 days. Even though adding new information about weak passwords or ongoing malware investigations gets frustrating because the same problems facing the financial and payments industries persist, it does not surprise Trustwave researchers. For a lot of software or hardware developers, their main concern is availability of the service. They want to make sure their POS is available and running to accept credit cards, often at the cost of a lot of security controls. It is difficult to implement security and to do it correctly.

Trustwave recommends longer passwords with more characters, rather than shorter ones with letters and numbers. A longer password that is a phrase not easily figured out is better than a shorter, complex password. These findings have been added to an online version of the 2014 Trustwave Global Security Report. To accommodate the fast changing nature of security threats, Trustwave is regularly updating its research and making the information available to consumers and payments industry stakeholders on the company’s site. The criminals stealing data are a constantly moving target. It no longer made sense for those interested in our research to have to wait a year to see new statistics. Having access to updated security reporting should be helpful to merchants. They can see how trends are tracking over time, instead of constantly having to go online to see what is relevant to them or rely on the trade groups to keep them informed. This provides one switch to keep them in the know, so there is some value there and it’s a smart move on Trustwave’s part. Since the new Payment Card Industry security requirements call for security measures to be embedded in software development lifecycles, there is some utility in Trustwave’s new approach to sharing research information.

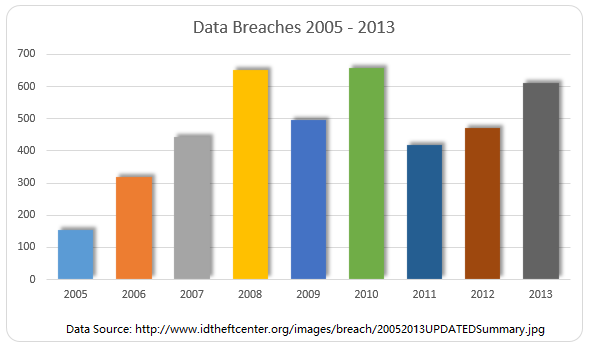

Trustwave said the trend of businesses detecting breaches continues to rise, with 29% of businesses doing so in 2013 compared to only 9% in 2009. Trustwave compiled that data from 691 post-breach forensics investigations conducted in 2013. The report also indicated e-commerce breaches are increasing, with 54% of all breaches targeting e-commerce sites in 2013, compared to only 9% in 2010. More regions, including the U.S., being in various stages of converting to EMV chip-based cards for card-present transactions fuels the criminals’ shift to e-commerce fraud. Additionally, the company is working with law enforcement officials after discovering a control center of eight servers behind what is being called Magnitude, an exploit kit of Russian origin that has led to thousands of attacks and millions of attempted malware attacks globally.

Posted in Best Practices for Merchants, Payment Card Industry PCI Security, Point of Sale Tagged with: breaches, card, card-present transactions, company, credit cards, data, e-commerce, EMV chip-based cards, financial, fraud, Global Security, hardware, industry, Malware, Merchant's, online, passwords, payment, Payment Card Industry security, payments, payments industries, POS, Security, servers, software

May 19th, 2014 by Elma Jane

Keeping your business’s finances in order doesn’t have to take all day. Bookkeeping is a necessary for small business owners, but it’s a time-consuming chore.

If you use QuickBooks for payroll, inventory or keeping track of sales, there are several timesaving shortcuts you can utilize to make bookkeeping easier.

Time-saving tips for getting the most out of QuickBooks in the least amount of time. Help you spend more time building your business and less time using QuickBooks.

Download data whenever possible. Even after factoring in initial setup time, downloading banking and credit card activity directly into QuickBooks is a huge time saver. Doing this will minimize the chance of human error and enable you to record activity faster than if you did it manually.

Make the Find feature your friend. Using the Find feature is the most efficient way to locate a particular invoice in QuickBooks. Those who usually open the form and click Previous until the form appears on the screen know how tedious this process can be. The Find tool will search for almost any transaction-level data, depending on your filters.

Memorize transactions. QuickBooks has the capability to memorize recurring transactions (invoices, bills, checks, etc.) and set them for automatic posts daily, weekly, monthly, quarterly and annually, eliminating the need to enter the same transaction into the software every month.

Use accounts payable aging. Use this feature for a snapshot on who you owe money to and manage your cash flow more efficiently.

Use accounts-receivable aging. Use this feature for a snapshot of information on who owes you money, how much you are owed and how long the individual has owed you.

Use classes. Classes can be very helpful to track income and expenses by department, location, separate properties or other meaningful breakdowns of your business.

Use QuickBooks on the go with remote access. Remote-access methods include QuickBooks Online, desktop sharing and QuickBooks hosting on the cloud, which allows you to take the program on the go and make changes no matter where you are.

Posted in Best Practices for Merchants Tagged with: accounts, accounts payable, banking, banking and credit card, bills, Bookkeeping, card, cash flow, checks, cloud, credit, data, desktop, desktop sharing, finances, hosting, income and expenses, invoices, online, program, QuickBooks, Remote-access, software, transaction

May 9th, 2014 by Elma Jane

Facebook is apparently ready to become a person-to-person (P2P) money transfer network. The clear decision to launch a money transfer service in the region can be seen as a test bed for Facebook’s larger ambitions of becoming a payments hub for its 1 billion user base. Facebook was only weeks away from gaining regulatory approval in Ireland for its remittance platform FT quoted unnamed sources. Facebook’s P2P platform will be geared to facilitating migrant remittances, with the goal of expanding its payment presence in emerging markets such as India. Facebook makes the bulk of its revenue from advertising, but 10 percent of its profits reportedly come from in-game payments for online and mobile games, such as Zynga’s popular FarmVille.

From WhatsApp to what’s next

Facebook’s February 2014 acquisition of mobile messaging service WhatsApp for $19 billion clarified the social network’s strategy. The WhatsApp acquisition and the expected P2P network launch as part of the first phase of Facebook’s deeper immersion into payments.

Tech giants face up to payments

When comparing the payment strategies of tech giants Google Inc., Apple Inc. and Facebook, the latter two competitors as having bigger potential upsides than Google. Facebook and Apple (via iTunes) already have established financial relationships with millions of users who have attached funding mechanisms – debit and credit cards – to their social media accounts. As primarily a search engine, Google is playing catch up to persuade its users to set up Google Wallet accounts.

In May 2013, Google launched its own P2P network by integrating Google Wallet with Gmail accounts, so that wallet users can facilitate money transfers via email. More recently, reports have surfaced indicating Google plans to extend Google Wallet to its wearable technology solution Google Glass. But the success of such ventures rests on users’ confidence with Google as a financial service provider.

Facebook as having a brighter financial services future than Apple. Apple’s reach is limited to consumers who have iPhones and iPads, whereas Facebook is not tied to any branded mobile devices, it is a very ubiquitous offering. It could apply to anybody with any type of phone or tablet.

Eventually, tech companies like Facebook will need to partner with payment businesses in order to expand into the merchant-centric brick-and-mortar world. The mobile POS solution provider, a business unit of global POS terminal manufacturer Ingenico SA, would be an ideal partner for Facebook. If they extend what they do from P2P payments to more of a wallet purchasing capability for their users, then the next step could very easily be an extension of that into servicing the merchant side.

Posted in Financial Services, Mobile Payments, Smartphone Tagged with: Apple Inc.Facebook, consumers, credit cards, debit, device, financial service, financial service provider, Gmail accounts, Google Glass, Google Inc., Google Wallet accounts, ingenico, iPads, iPhones, iTunes, merchant-centric brick-and-mortar, migrant remittances, mobile, Mobile Devices, mobile games, mobile messaging service, mobile pos, mobile POS solution, mobile POS solution provider, money transfer, money transfer network, money transfer service, network, online, p2p, P2P network, P2P payments, P2P platform, payment businesses, payments, payments hub, phone, POS terminal, remittance, remittance platform, search engine, service provider, social media, social media accounts, social networks, tablet, wearable technology

April 7th, 2014 by Elma Jane

Business-to-business ecommerce describes Internet-enabled transactions between businesses, such as a manufacturer and a wholesaler, a wholesaler and a retailers, or a wholesaler and a business user. The B-to-B ecommerce market was expected to exceed $550 billion in the U.S. last year, offering great opportunities for distributors and manufacturers to streamline sales, boost profits, and engage with new customers.

Since the late 1990s, businesses have been using the Electronic Data Interchange (EDI) system to transfer purchase orders and similar structured information electronically, representing, if you will, a form of B-to-B ecommerce.

Separately, some B-to-B sellers have created websites on which business customers can make purchases as if they were shopping on a business-to-consumer site. This category of B-to-B ecommerce may enjoy the most growth and offer the most opportunity.

Important points to consider of running a B-to-B ecommerce site.

B-to-B Customers Are also B-to-C Customers

B-to-B sites often trail consumer sites in technology, function, capabilities, and design. Typically not good enough.

As an example, the U.S. B-to-B site for a major multinational manufacturer, which includes information for dealers in the U.S., can only be viewed on Internet Explorer, and won’t work in any other browser, including Firefox, Chrome, Opera, or Safari. And don’t even think about visiting this site on a mobile device. It just won’t work.

This is a ridiculous business decision. It forgets a fundamental fact about B-to-B ecommerce customers. They are also B-to-C ecommerce customers.

It is extremely likely that the professional shopper on an ecommerce-enabled B-to-B website has had at least some experience shopping on consumer ecommerce sites, which all have compelling product photography, good navigation, good search capabilities, and good content.

A B-to-B ecommerce site must provide the same visual and functional experience as the best B-to-C ecommerce sites.

Personalization Is Vital

B-to-B shoppers may require a greater level of personalization than B-to-C customers, since businesses may have contract prices, special payment terms, or negotiated shipping rates.

Business relationships may be very deep and complicated. It is not unusual for B-to-B ecommerce sites to require registration before showing prices or shipping rates or offering a quote. This login requirement allows the B-to-B ecommerce site to personalize almost every aspect of the transaction.

A good B-to-B ecommerce site may take a little longer to launch since the system for handling relatively complex business relationships can take some time. But once it is in place, this personalization will mean that the relationship could be longer lasting.

Sales people Are the Primary Marketing Vehicle

While it is both possible and likely that B-to-B ecommerce sites will be able to acquire new customers simply by making products easy to order online, salespeople who contact customers are probably the B-to-B ecommerce seller’s primary and best marketing channel.

Salespeople can attract new customers or deepen relationships with existing shoppers. Sometimes, it can be enough to follow up after a B-to-B sale with a call to make certain that the transaction went as expected.

Shopping Is Part of Your Customer’s Profession

One of the most significant differences between B-to-B and B-to-C ecommerce is that shopping is part of the B-to-B ecommerce customer’s daytime job.

This means that the stakes can be higher for the B-to-B seller. If the shopper has a good experience, that shopper is likely to return and reorder repeatedly – even suggesting the seller to co-workers or other divisions. But if something goes wrong, particularly something that would cause the shopper to miss deadlines at work or appear in some way to have done a poor job, that shopper will likely blame the B-to-B seller. Depending on the unhappy shopper’s influence, the B-to-B seller might lose the entire account, including many individual buyers or divisions.

This means that order handling and transactional communications must be top notch. Some B-to-B ecommerce sellers will call customers to confirm orders or shipments when the customer has ordered a large quantity, very expensive items, or requested express shipping, since these orders may represent important transactions to the customer.

What Ecommerce Can Do for your B-to-B Business

If you sell to other businesses, ecommerce should have three potential benefits for your business.

First, it may help new customers find you. Having an easy-to-find and use ecommerce site means that new customers – customers with a need – will be able to locate your business regardless of geography or prior relationships.

Second, B-to-B ecommerce may streamline sales for existing customers. Some of your current customers will appreciate the ability to order online, 24 hours a day 7 days a week. The process may also be faster than sending emails or, even worse, faxed orders.

Finally, B-to-B ecommerce may improve margins and boost profits. It may be possible to provide customers with a better ordering experience and better customer service using ecommerce while spending less on labor and order processing. Any cost savings that B-to-B ecommerce brings may drop straight to your business’s bottom line.

Posted in Credit card Processing, e-commerce & m-commerce, Electronic Payments, Internet Payment Gateway, Mobile Payments, Mobile Point of Sale, Small Business Improvement Tagged with: account, b-to-b, b-to-c, better ordering experience, boost profits, business-to-business, business-to-consumer, business's bottom line, communication, consumer, cost savings, customer service, e-commerce, ecommerce, ecommerce sites, electronic data interchange, faxed orders, growth, improve margins, new customers, online, order handling, order processing, personalization, profits, purchase orders, salespeople, seller, sending emails, shopper, special payment terms, transaction, wholesaler

March 14th, 2014 by Elma Jane

Merchant and Consumer Groups Seek Senate Support To Forego EMV Chip and Signature As Breach Concerns Rise

There’s no shortage of answers in trying to put a stop to hackers set on throwing chaos into the way consumers transact at the point of sale, or online for that matter. Yesterday, the Banking, Housing and Urban Affairs subcommittee on national security and international trade and finance got its chance to hear some of them.

During the hearing, William Noonan, deputy special agent in charge, U.S. Secret Service, noted the advances in computer technology and greater access to personally identifiable information online, which have created a virtual marketplace for transnational cyber criminals to share stolen information and criminal methodologies. As a result, the Secret Service has observed a marked increase in the quality, quantity, and complexity of cyber crimes targeting private industry and critical infrastructure. These crimes include network intrusions, hacking attacks, malicious software, and account takeovers leading to significant data breaches affecting every sector of the world economy.

The recently reported data breaches of Target and Neiman Marcus represent only the most recent, well-publicized examples of this decade-long trend of major data breaches perpetrated by cyber criminals intent on targeting the nation’s retailers and financial payment systems. The increasing level of collaboration among cyber-criminals allows them to compartmentalize their operations, greatly increasing the sophistication of their criminal endeavors and allowing for development of expert specialization. These specialties raise both the complexity of investigating these cases, as well as the level of potential harm to companies and individuals.

So how should the industry react to prevent further breaches? Those opinions provided during testimony at the hearing varied widely, though both consumer and merchant groups would like the card networks to give up requiring only signatures for smart card purchases at the point of sale.

Consumer program director at the U.S. Public Interest Research Group, called for myriad of changes, citing that the greater risk from the recent breaches is less related to identity theft than it is to fraud on existing accounts, and he said it’s time for players on both sides of the transaction to focus more on protecting consumers than on managing their own risk.

Until now, both banks and merchants have looked at fraud and identity theft as a modest cost of doing business and have not protected the payment system well enough. They have failed to look seriously at harms to their customers from fraud and identity theft -including not just monetary losses and the hassles of restoring their good names, but also the emotional harm that they must face as they wonder whether future credit applications will be rejected due to the fraudulent accounts.

As a first step, Congress should institute the same fraud cap, $50, on debit/ATM cards that exists on credit cards, or eliminate the $50 cap entirely, since it is never imposed because of the zero-liability policies issuers have voluntarily have imposed. Congress also should provide debit and prepaid card customers with the stronger billing-dispute rights and rights to dispute payment for products that do not arrive or do not work as promised, just as many credit card users enjoy.

Congress should endorse a specific technology, such as EMV smart cards and if it does, require the use of PINs when initiating smart card transactions. The current pending U.S. rollout of chip cards will allow use of the less-secure chip-and-signature cards rather than the more-secure chip-and-PIN cards. Why not go to the higher-and-PIN authentication standard immediately and skip past chip and signature? There is still time to make this improvement.”

Retailers have spent billions of dollars on card-security measures and upgrades to comply with PCI card security requirements, but it hasn’t made them immune to data breaches and fraud. The card networks have made those decisions for merchants, and the increases in fraud demonstrate that their decisions have not been as effective as they should have been.

The card networks should forego chip and signature and go straight to chip and PIN. To do otherwise would mean that merchants would spend billions to install new card readers without they or their customers obtaining PINs’ fraud-reducing benefits. We would essentially be spending billions to combine a 1990’s technology chips with a 1960’s relic signature in the face of 21st century threats.

Posted in Best Practices for Merchants, Credit card Processing, Credit Card Reader Terminal, Credit Card Security, Digital Wallet Privacy, Electronic Payments, EMV EuroPay MasterCard Visa, Financial Services, Merchant Services Account, Payment Card Industry PCI Security, Point of Sale, Small Business Improvement, Visa MasterCard American Express Tagged with: banking, Breach, card networks, card-security, chip and signature, chip cards, chip-and-PIN cards, computer technology, credit applications, credit cards, critical infrastructure, cyber crimes, cyber-criminals, data breaches, debit atm cards, EMV, hackers, hacking attacks, international trade and finance, malicious software, managing risk, merchant, national security, netwrok intrusions, new card readers, online, payment system, pci card security requirements, PIN, point of sale, prepaid card customers, smart card transactions, technology chips, the secret service, transnational cyber criminals, virtual marketplace, world economy

February 3rd, 2014 by Elma Jane

The migration to cards that use chips instead of magnetic strips, known as EMV technology, is well underway in the U.S. No government regulation is needed to make it happen. But the EMV migration and the Target breach are different things. It’s true that EMV chip cards can prevent criminals from producing counterfeit cards using stolen account numbers. But EMV doesn’t stop criminals using stolen cards online. So innovators are deploying new technologies to deter other forms of fraud.

Headline-grabbing events inevitably lead to calls for new laws. But in the case of our nation’s electronic payments systems, new government mandates would stifle marketplace innovations that hold great promise for providing consumer benefits and reducing criminal activities.

Financial institutions compete for customers by providing consumer protections even beyond requirements of current law. Many retailers also offer customers speedy transactions, such as “sign and go” and “swipe and go” for small transactions, while the payments industry ensures consumers still have zero liability. These protections and flexibility are why U.S. consumers are going cashless and carry more than one billion debit and credit cards. More than 70% of retail purchases are made with electronic payments, and our member companies process more than $4 trillion in electronic payments each year.

Fraud accounts for fewer than six cents of every $100 spent on payments systems – a fraction of a tenth of a percent. U.S. companies have made significant financial and technological investments, building sophisticated fraud tools that insulate consumers from liability. To build on this, Congress should foster greater international law enforcement cooperation to fight cybercrime, particularly in countries that harbor crime rings, and replace 46 divergent state breach notification laws with a uniform national standard.

The private sector is best positioned to address the constantly shifting tactics of criminals, and it is doing so without government mandates. Do Americans really want the government in charge of the security and monitoring of our payments?

Posted in Best Practices for Merchants, Credit card Processing, Credit Card Security, Electronic Payments, EMV EuroPay MasterCard Visa, Financial Services, Visa MasterCard American Express Tagged with: counterfeit cards, cybercrime, data breach, debit and credit cards, electronic payment systems, electronic payments, emv chip cards, emv technology, fraud, liability, magnetic strips, migration, online, security and monitoring of our payments, small transactions