February 12th, 2016 by Elma Jane

If there’s an e-commerce trend there’s also a delivery trend.

Will drone be the future of delivery?

Drone delivery is the next big key to e-commerce.

Place an order, payment is collected from a mobile payment system. Drone goes out to deliver the order.

Drone delivery is a great concept to combine for any retail merchants or company that deals with the public. It represents a new system to connect buyers with merchandise, and quickly. The trend for e-commerce delivery.

Posted in Best Practices for Merchants, e-commerce & m-commerce Tagged with: e-commerce, merchants, mobile, mobile payment, payment, Retail Merchants

February 9th, 2016 by Elma Jane

Since the implementation of the EMV liability shift last year, consumers are still unsure whether to dip or swipe their payment cards at the checkout register, and transaction process itself is slower than a card swipe.

As the EMV process continues, can contactless register only help to make checkout process faster? With contactless register checkout only, consumers can just tap and pay with either card or mobile wallet.

Contactless like NFC is now a standard feature in most high-end smartphones, and most EMV-enabled point-of-sale terminals contain the necessary technology to accept contactless payments. So the idea of contactless register checkout only is something to test for some merchants in a certain retail sector.

Posted in Best Practices for Merchants, EMV EuroPay MasterCard Visa, Near Field Communication, Point of Sale Tagged with: cards, consumers, contactless, EMV, merchants, mobile, mobile wallet, nfc, payment, payment cards, point of sale, Smartphones, terminals, transaction

February 8th, 2016 by Elma Jane

The U.S. House of Representatives voted to end the Obama administration’s Operation Choke Point.

The vote was 250-169, which represented a group of all Republicans and 10 Democrats voting to revoke the law.

Operation Choke Point, which began in 2013, leveraged the government’s regulatory power over merchant banks, acquirers and payment processors, forcing them to drop clients engaged in industries like payday lending, firearms and other high-risk sectors especially online like gambling and adult entertainment.

In a statement by U.S. House Rep. Luetkemeyer, the first step has been taken to ensure that federal banking agencies can no longer compel financial or payment institutions from offering financial services to licensed, legally-operating businesses that has been a target not because of potential wrongdoing, but purely on personal and political motivations and without due process.

Posted in Best Practices for Merchants Tagged with: acquirers, banks, financial services, merchant, payment, payment institutions, processors

February 2nd, 2016 by Elma Jane

Businesses continue to struggle with the prohibited storage of unencrypted customer payment data. The Payment Card Industry Data Security Standard (PCI DSS), merchants are instructed that, Protection methods are critical components of cardholder data protection in PCI DSS Requirement.

PCI DSS applies to every company that stores, processes or transmits cardholder information. Regardless of the size or type of business you operate, the number of credit card transactions you process annually or the method you use to do so, you must be PCI compliant.

Data breach is not a limited, one-time occurrence. This is why PCI compliance is required across all systems used by merchants.

Encryption and Tokenization is a strong combination to protect cardholder at all points in the transaction lifecycle; in use, in transit and at rest.

National Transaction’s security solutions provide layers of protection, when used in combination with EMV and PCI-DSS compliance.

Encryption is ideally suited for any businesses that processes card transactions in a face to face or card present environment. From the moment a payment card is swiped or inserted at a terminal featuring a hardware-based, tamper resistant security module, encryption protects the card data from fraudsters as it travels across various systems and networks until it is decrypted at secure data center.

Tokenization can be used in card not present environments (travel merchants) such as e-commerce or mail order/telephone order (MOTO), or in conjunction with encryption in card present environments. Tokens can reside on your POS/PMS or within your e-commerce infrastructure at rest and can be used to make adjustments, add new charges, make reservations, perform recurring transactions, or perform other transactions in use. Tokenization protects card data when it’s in use and at rest. It converts or replaces cardholder data with a unique token ID to be used for subsequent transactions.

The sooner businesses implement encryption and tokenization the sooner stored unencrypted data will become a thing of the past.

Posted in Best Practices for Merchants, Travel Agency Agents Tagged with: card, card data, card present, cardholder, compliance, credit card, customer, data, data breach, data security, e-commerce, EMV, encryption, Mail Order/Telephone Order, merchants, moto, payment, Payment Card Industry, PCI-DSS, POS, secure data, Security, terminal, tokenization, tokens, travel, travel merchants

January 25th, 2016 by Elma Jane

New Timeframes for Electronic Gift Card Orders

Please be aware that NTC’s Electronic Gift Card (EGC) Design & Artwork team has upgraded their printers. The new timeframes for both FanFare and EGC (Givex) gift card shipments during non-peak times are the following:

- Standard Card Orders: 8 Business days, plus 2 Day Delivery

- Custom Card Orders: 12 Business days, plus 2 Day Delivery

Converge Mobile: Frequently Asked Questions

Will there be more EMV chip card readers in the future? Yes! Additional devices ranging in price points and feature/functionality will be introduced throughout 2016.

Do VirtualMerchant Mobile login credentials work with Converge Mobile?Yes! The mobile login credentials that customers use today for VirtualMerchant Mobile are the same for Converge Mobile.

Is the talech iCMP the same as the one sold for Converge and Converge Mobile? No! Please use item code CICMP for devices that will be used with Converge and/or Converge Mobile. Otherwise, there is device reconfiguration work that has to take place resulting in a negative customer experience.

UPCOMING EVENTS

April 19-21 May 2-4

TRANSACT 16 (ETA) Southeast Acquirers Association (SEAA)

INDUSTRY LINKS

|

|

Posted in Best Practices for Merchants, nationaltransaction.com Tagged with: card, chip card, Electronic gift card, EMV, gift Card, merchant, mobile, payment, payment technology, processor, travel, travel industry

January 21st, 2016 by Elma Jane

Merchant accounts are as varied as the merchants themselves and the goods being sold.

What kind of account would you fall under:

High Risk Merchant Accounts – Finding a processor who is willing to take your account can be more challenging. High risk merchants range from travel agencies to multi-level marketing companies, credit restoration merchants, casinos, online pharmaceutical companies, adult/dating merchants and many other.

Internet based merchant account (Ecommerce/Website order processing) – E-Commerce is a booming market, with so many people buying and selling goods online due to the wide reach and easy access to the internet.

Mobile or Wireless merchant account – This merchant is specifically designed for small businesses, solo professionals, and mobile services (including lawyers, landscapers, contractors, consultants, repair tradesmen, etc), who are constantly on the move and require a payment to processed on the spot.

MOTO (Mail or Telephone order) – This enables phone based or direct mail orders processing for customers who can buy your product or service from the comfort of their home. Since there is no card present there is no need for traditional equipment.

Multiple Merchant Accounts – Some businesses can have merchant accounts of a couple or all different types. Merchants who fall into this category are called multi-channel merchants as they sell their goods through a number of different channels. Most commonly this is related to retail stores who also have an online presence to sell their goods. This is very common in today’s competitive market where constant contact with customers is critical to success.

Traditional Account with Equipment – Most commonly used for retail businesses (grocery, departmental stores etc) where the transactions are processed in a face to face interaction also known as Point of Sale (PoS).

Interested to setup an account give us a call at 888-9962273

Posted in Best Practices for Merchants, e-commerce & m-commerce, Mail Order Telephone Order, Mobile Payments, Mobile Point of Sale, Point of Sale, Travel Agency Agents Tagged with: account, card, card present, credit, customers, e-commerce, high risk merchant, internet, merchant accounts, merchants, mobile, mobile services, moto, multi-channel merchants, payment, point of sale, POS, processor, transactions, travel, travel agencies

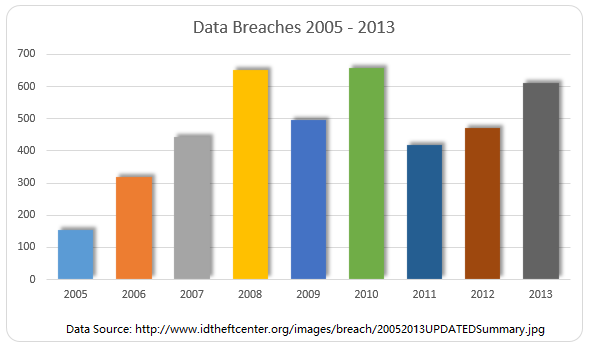

January 21st, 2016 by Elma Jane

HYATT DATA BREACH HITS 250 HOTELS WORLDWIDE

Hyatt hotel company noted that the breach that occurred over the course of almost four months hit 250 different hotels over the span of about 50 countries.

The breach covered payment card data from the cards used at various Hyatt hotels in that range of dates, reports note, and most of the breaches seem to have hit at hotel restaurants. Those who also hit the spas at Hyatt, along with front desks, gold shops, and even parking structures may also have been impacted by the breach.

The company couldn’t confirm how long the network was vulnerable nor if any payment card data had actually been stolen.

Perimeter Defense where data is protected with passwords and firewalls and the like is fine and well, but more needs to be put into protecting the data in the event someone clears security.

Encrypting Data is a great step to take, assuming someone manages to clear the perimeter, the encryption makes the data itself much more difficult to access and use. So while perimeter defense keeps unauthorized users away from data, encryption keeps those who reach the data from being able to readily read it.

Data Security is something none of us can take for granted, so doing what we can to protect that data being vigilant about statements, putting up proper security, encrypting data all of these contribute to better protected data and a safer time online.

Posted in Best Practices for Merchants, Travel Agency Agents Tagged with: card data, cards, data, online, payment, Security

January 19th, 2016 by Elma Jane

2015 was a major period of growth for the online and mobile payment industry. Close to 60 million Americans used mobile payments on a consistent basis, representing close to 18 percent of the population. However, around 52 percent of Americans are aware of mobile payments and how to use them.

Because of both the wide awareness and accessibility of mobile payments, analysts expect consistent mobile payment use to double this year. Millennials and high-income spenders tended to adopt the technology more quickly, at 23 percent and 38 percent consistent usage respectively.

Even more intriguing than the wide-spread use of mobile payments is how large the market grew. In 2015, $8.71 billion passed through online payment services providers. Even more intriguing is the prediction that this market will more than triple to $27.05 billion by the end of this year.

Posted in Best Practices for Merchants Tagged with: mobile payment, online, online payment, payment, payment industry, payment services, provider's, services providers

January 7th, 2016 by Elma Jane

National Transaction is now offering Apple Pay to Canadian Merchants.

Apple Pay works with NTC’s EMV-contactless point of sale terminals in Canada.

Security and privacy is at the core of Apple Pay, and when a consumer adds a credit card to Apple’s mobile wallet, the actual card numbers are not stored on the device, or on Apple servers.

Apple Pay will create a unique Device Account Number that is assigned, encrypted and securely stored in the secure element on the device, the same way it operates in the U.S. Each transaction is authorized with a one-time unique dynamic security code.

To pay, consumers simply hold their mobile device near the contactless reader, exactly as they would a contactless card today. The payment information is then passed to the POS system once the consumer confirms the transaction using Touch ID on their device.

Bringing Apple Pay to NTC terminals addresses an increasing consumer demand for contactless payments, while also allowing Canadian businesses to offer customers the convenience of paying through an iPhone, iPad or Apple Watch.

American Express is Apple’s issuing partner in Canada.

Posted in Best Practices for Merchants Tagged with: Contactless card, contactless point of sale, contactless reader, credit card, EMV, merchants, mobile device, mobile wallet, payment, POS system, security code, terminals

December 28th, 2015 by Elma Jane

Major data breaches were acknowledged by another hotel chain and another brand popular with kids.

Hyatt discovered the intrusion on Nov. 30, which targeted Hyatt-managed properties (not those owned by franchisees), but did not disclose exactly how many properties were affected or how many records may have been exposed. The malware used in the attack targeted payment-card information including cardholder names, PANs, expiration date and CVV/CVC information.

Separately, a security researcher discovered a leaked database from Sanrio, the Japanese company that designs, licenses and produces the popular hello Kitty character. The database reportedly contains account data for 3.3 million users of Sanriotown.com and other Sanrio-owned Websites including hellokitty.com. The company has not yet acknowledged the extent of the breach publicly but said it is investigating.

If so, it is the second network intrusion made public putting the personal information of young people at risk after the Vtech Toy Company Data Breached. Almost 5 million parents and more than 200,000 kids was exposed. The hacked data includes names, email addresses, passwords, and home addresses of 4,833,678 parents who have bought products sold by VTech.

Posted in Best Practices for Merchants Tagged with: card, card information, data, data breaches, payment