Credit card transaction types are categorized based on the level of risk and processing cost associated with them. Here’s a breakdown of the common types:

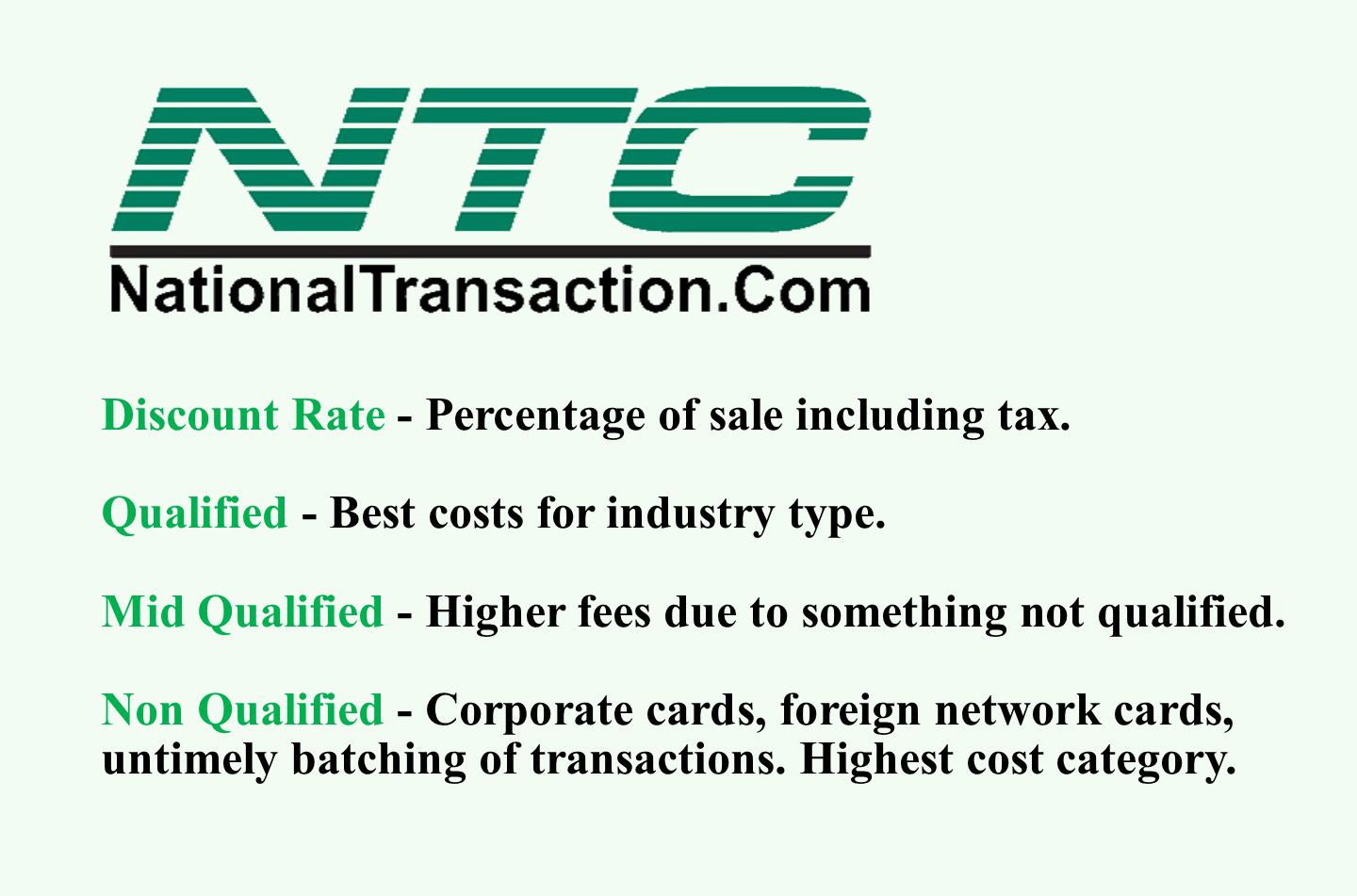

1. Qualified

Definition: These are considered the “safest” and least expensive transactions for processors to handle.They typically involve traditional credit or debit cards processed in person with a physical card swipe or chip insertion.

Characteristics:

Card is present during the transaction

Cardholder’s signature is captured (if required)

AVS (Address Verification Service) matches the billing address on file

CVV (Card Verification Value) is provided and matches

Transaction meets all security protocols and risk assessment criteria set by the card issuer and processor.

Examples:Swiping a standard Visa or Mastercard credit card at a retail store.

2. Mid-Qualified

Definition: These transactions fall in between qualified and non-qualified in terms of risk and processing cost. They often involve card-not-present transactions or cards with higher reward structures.

Characteristics:

Manually keyed-in transactions (online, over the phone, or mail order)

Rewards cards with higher cashback or points benefits

Business or corporate cards

Transactions where AVS or CVV information is not provided or doesn’t match

Examples: Entering your credit card details online to purchase something, using a rewards card with travel benefits.

3. Non-Qualified

Definition: These transactions are considered the riskiest and most expensive to process.They often involve international cards, manually keyed transactions without proper security measures, or cards with very high reward programs.

Characteristics:

International credit cards

Manually keyed transactions without AVS or CVV verification

High-risk businesses like online gambling or adult entertainment

Keyed transactions for business or corporate cards

Examples: Using a foreign-issued credit card, manually processing a transaction without verifying the cardholder’s address.

Why does this matter?

Processing Fees: Merchants are charged different fees for each transaction type.Qualified transactions have the lowest fees, while non-qualified transactions have the highest.

Tiered Pricing: Many payment processors use tiered pricing models, categorizing transactions into these types and charging accordingly. This can sometimes be confusing or lead to unexpected costs for merchants.

Interchange Fees: The card networks (Visa, Mastercard, etc.) also charge interchange fees for each transaction, which vary based on factors similar to those used for transaction type categorization.

Understanding these transaction types is crucial for merchants to:

Negotiate better processing rates: By understanding the factors that influence transaction categorization, merchants can negotiate better fees with their processors.

Optimize payment processing: Merchants can take steps to minimize the number of mid-qualified and non-qualified transactions, such as encouraging in-person payments or using address verification systems.

Control costs: By being aware of the different transaction types and their associated costs, merchants can better manage their payment processing expenses.

Remember: The specific criteria for each transaction type can vary depending on the payment processor, card network, and individual merchant account. It’s always best to clarify with your payment processor to understand their specific categorization rules and fee structures.

To establish a merchant account for your business call now 888-996-2273 or click here NationalTransaction.Com

Fighting chargebacks is important to a business. Whether you process transactions at a point of sale location or operate an e-Commerce business making sure you have implemented a process to dispute your chargebacks is critical.

Basic concepts that can be used to begin learning how to dispute chargebacks:

Keep accurate records of data that is easily accessible. Keeping track of your sales and products have a much easier time in collecting the information necessary to combat a chargeback.

Act quickly, don’t wait! You only have 10 days to respond to a chargeback or retrieval request. If you do not respond in 10 days you lose to a chargeback, and It gets worse; as you will not be able to re-present your case.

Compile and submit the documents to your processor. Make sure the documents have the original chargeback documents attached as well as the other supporting documents.

Follow up to make sure they have been received. Your processor may have an online system that allows you to submit documents directly into the processor chargeback system and some even allow you to view submitted documents in REAL TIME.

Monitor your chargebacks, this will help you understand what processes work for each specific chargeback type.

If you’re running an unusual transaction and know of it beforehand, let your merchant provider know; sending an invoice in advance can cut processing time.

Make sure to give your most up to date information. Keeping provider in the loop on the fluctuations in your processing volumes will help tremendously, especially as your business grows.

Funding delays are an inconvenience, but being prepared can keep the delay to a minimum. If you keep these tips in mind, you’ll be processing without ever having to worry about delays again.

Flagged, Security and Review Process

Why some merchant accounts hold funds and others do not?

There are a number of reasons:

Underwriting merchant account is ongoing. Imagine a small business convenience store was set up and accidentally enters $1,000.000 should we transfer that or hold it?

One reason is something has gone with that particular business account.

Another reason could be that particular institution’s practices are more efficient than others.

Financial institutions use different payment processing systems, and they are not uniform in their practices. For this reason, some transactions are significantly faster than others.

Though there are other reasons funds get held, the main reason for this occurrence is when a payment is out of the ordinary patterns.

Unusual transactions are any transaction that vary from your typical processing patterns.

If It’s for security, an account will be flag as a way to reduce fraud as well as ensuring no one is using your account.

How do I know if I’m flagged?

Security checks are carried out by processing banks or processor. You’ll be contacted by a loss prevention officer. They’ll provide all details of the hold, including the review process as well as the next steps.

What’s the review process?

The review is simply to verify your transaction before delivering your funds. A typical review is confirming the transaction with yourself as well as your customer’s credit card company. You’ll speak briefly with a loss prevention officer to discuss the transaction. If further review is required, the loss prevention officer may ask you for a copy of the transaction’s invoice.

How can I speed up the process?

For an easy review, make sure to provide detailed documents. When an invoice is asked for, make sure it clearly shows the following:

Factors to Consider When Buying a Credit Card Terminal:

NFC – check out the payment wave of the future. NFC technology features, where you can accept Apple Pay and Android Pay for payments.

Security and Stability – do I have a computer tablet or other device that will accommodate the future technology? Newer credit card machine work faster, they also protect sensitive card data and have the ability to accept EMV and PIN. Older terminals may not comply with today’s PCI security standards.

Mobile/Wireless Connectivity – credit card terminal should be able to quickly and easily accept credit card payments and work with your payment processor anywhere.

Connectivity – do you use mobile, Wi-Fi, dial, or (IP) Internet connection? Most current credit card terminals use both technologies, but when connected to dial-up your transactions can be quite slow, unlike IP connection which can speed up your transactions.

Programmable or Proprietary – if they will not let you program it why NOT?

There are many options when searching for the right credit card terminal for your business but there are also a number of factors to consider before making an investment.

Interchange – Goes to the bank that issued the card, and is typically made up of a flat rate plus a percentage of the sale.

Assessments – Go to card network like Visa, MasterCard, Amex, Discover etc.

Processor fees – Fees involved with providing the service, risk assessments, the type of transaction, and the size of the transaction. This portion includes the margin between the total rate and the two previous parts, along with any incidental fees, like chargeback or statement fees.

There are a lot more intricacies of what makes up a credit card rate, but this information gets you off to a good start. If you’re interested in learning more about electronic payments, check our website www.nationaltransaction.com or call now 888-996-2273 and talk to our Payment Consultant.

The most common forms of rate structures for credit card rates are:

2-Tiered: Qualified and Non-Qualified

3-Tiered: Qualified, Mid-qualified, or Non-qualified

Each and every transaction you accept is classified into one of the above and is the basis for the credit card rate you see on your statement.

As a general rule, qualified transactions are going to be “standard” cards; without any consumer or corporate rewards associated with them. Accepted in the “standard” method expressed in your merchant processing agreement, this is where Card-Not-Present (CNP) setup comes into play.

Mid and Non-Qualified transactions include:

Rewards cards, keyed-in payments (for swipe accounts), AVS (Address Verification Service) does not match or is not performed, not all required fields are entered, or the payment was entered in a late batch. Ex. the payment was sent to the processor 48 hours or more past the time of the authorization.

Interchange is where transactions are submitted for payment from the Acquirer or Merchant Processor to the Card Issuer or Debit Network. It also represents the fees paid by the merchant acquirer to the Card Issuer.

At the time the transaction is exchanged fees are paid and vary based on processing method utilized. It is more expensive to process a hand-keyed transaction than a card-swiped transaction.

Several rates may apply to your transactions, depending on your method of processing each transaction and the interchange qualification that is assigned to each transaction by the Card associations for processing transactions.

Rate qualification criteria: The card associations consider the card product used in the transaction, how the transaction data is entered, the time of settlement versus time of authorization.

Interchange Category Based on Card Type: Credit, Debit, and Rewards purchasing.

Industry Type: Retail or E-commerce.

Qualification Elements: Swiped card or Key entered.

When you settle your transactions each day, Acquirer or Merchant Processor like NTC routes them to the Card Associations (Visa, MasterCard, Discover) and debit networks through Interchange.

Visa, MasterCard, Discover (Card Associations and Debit Networks) establish the rules and manage the Interchange of all transactions.

Batch – is a collection of credit card transactions, usually a single day’s worth.

Batch Processing – refers to a one-time closing or settling the entire batch of transactions.

The point-of-sale terminal or credit card processing software can be set on:

Manual Batch close – merchant will need to batch out at the end of each day. The processor will receive a command to settle all transactions that have been entered. There will be a printed report showing the transaction totals in the batch once a batch is settled.

Changes can be made to existing transactions in the batch before a batch is settled. Example: If you want to change an amount of one of the transactions or you want to void a transaction.

Automatic Batch close – The terminal or software will automatically close the batch, (settle the transactions) at a certain time each day, no manual intervention is needed by the merchant or in some case the processor will settle the batch (called host batch close at the processor level). Automatic batch close set-up is advisable for most businesses unless a tip edit function is required, manual batch close would be the better option.

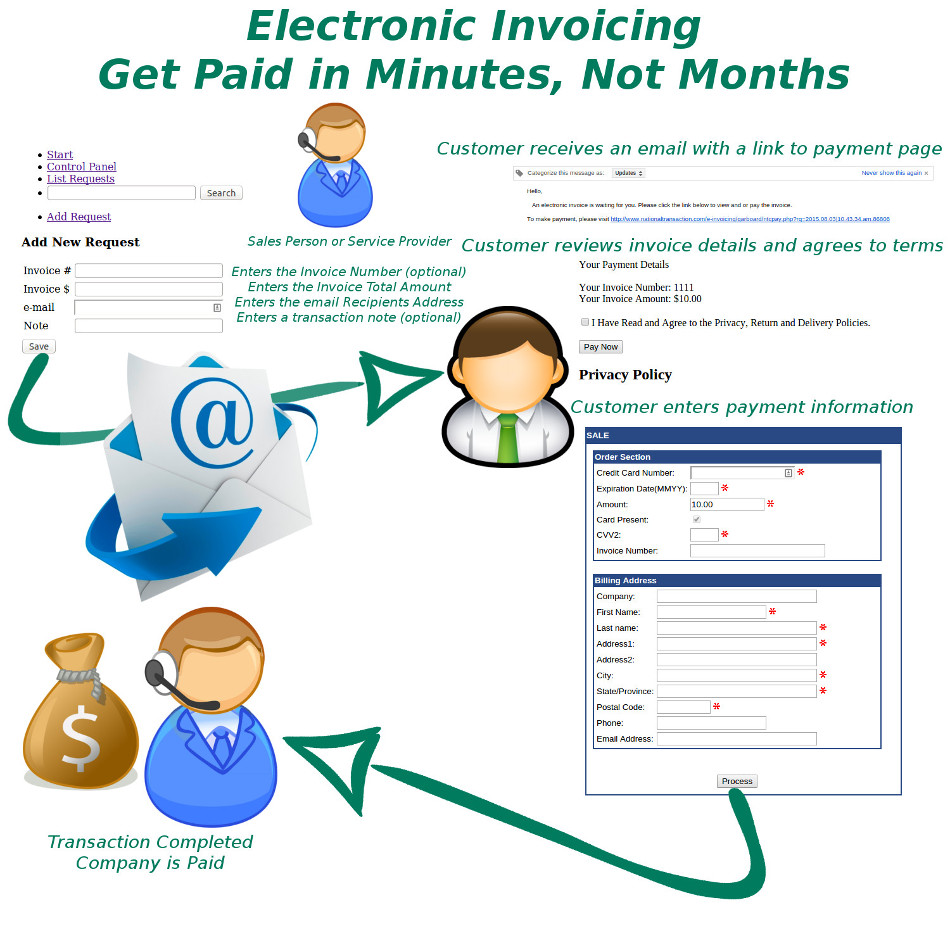

Lisa an independent Travel agent started her business in October 2006. She has been using her bank as their credit card processor and use to do a manual type-in process. When she learned about NTC while trying to shop online because she thinks it’s time for her to upgrade her system, Lisa found that NTC is not only a payment expert when it comes to travel, but a technology expert as well that met her business’s needs.

Lisa is using NTC e-Pay an electronic invoicing that has streamlined their credit card processing. The process not only has it saved money with competitive rates but most importantly it saves time. The level of assistance provided went above and beyond what she expected.

NTC e-Pay is for all types of merchants in a Card-Not-Present Transaction.

Consumer Acess – consumer will have access to their transaction details on their device. For travel merchants, the consumer can have access to their itinerary while on the go!

Customizable Pricing – when custom pricing becomes an issue, shopping carts, POS systems and booking engines tend to get really complicated.

Fast – saves time and unnecessary cost. Moves money efficiently and effectively. Simply email payment request that can be paid in 2 simple steps.

The customer receives an email with a link to the payment page. Customer reviews invoice details and agrees to terms. The customer enters payment information.

Process, transaction is completed company is paid. You get paid in minutes, not months.

Protects you from Chargeback – the customer is required to agree to your Refund Policy, Privacy Policy, Timing and Delivery Policy.

Secured – credit card information is processed securely. The customer is entering their credit card information without faxing or emailing credit card numbers.

The no shopping cart e-Commerce solution! – avoids the complexities of a shopping cart or integration into an accounting or POS.

Thinking of upgrading your system give us a call at 888-996-2273 and know more of our NTC e-Pay platform.