A surcharge is a fee that is added to a card transaction, either as a set amount or a percentage of a transaction. Typically, used to cover the cost of the merchant account charges.

There are rules, exceptions and state laws to observe to ensure you are compliant.

At present there are surcharge bans in the following states:

California, Colorado, Connecticut, Florida, Kansas, Maine, Massachusetts, New York, Oklahoma and Texas. (Appeals are pending for California and Florida)

Surcharge Rules:

Applicable only to credit card transactions, not debit or prepaid card transactions.

The surcharge cannot be greater than the merchant’s average discount rate for that brand’s credit card transactions.

Maximum surcharge allowed is 4%.

Cardholder must be notified of the surcharge.

Surcharge must be listed on the receipt as a line item and the primary payment amount must be processed together as one transaction.

A convenience feeis a fee charged for the “convenience”of being able to pay using an alternative payment channel outside the merchant’s customary payment channel.

Any merchant can charge a convenience fee IF the fee charged is for the legitimate convenience of being able to pay using a different payment channel than the merchant’s usual payment channel.

Example: Your business customary payment channel is face-to-face or card present and you provide an alternative payment channel, such as the option to pay by phone using a credit card, that could then charge a convenience fee along with the payment.

Mail Order/Telephone Order (MOTO) merchants and ecommerce merchants, whose customary payment channel is exclusively non face-to-face or card-not-present, are NOT permitted to charge convenience fees.

Convenience Fee Rules:

Customer must be notified of the convenience fee prior to finalizing payment and given the opportunity to cancel.

Payment must take place through an alternative payment channel.

The fee can only be added to a non face-to-face transaction. Must be flat or fixed, regardless of the value of the payment due.

The fee must be applied to all means of payment accepted through the alternative payment channel. Must be included in the total transaction amount.

The travel industry, with its high-value transactions and international clientele, faces unique challenges when it comes to credit card processing. While accepting plastic is crucial for smooth booking and customer convenience, travel agencies must be aware of the inherent risks and implement strategies to mitigate them. Here’s a breakdown of the key credit card processing risks and how to minimize them:

1. Chargebacks:

The Problem: Travel plans change, flights get delayed, and unforeseen circumstances arise. This can lead to a higher rate of chargebacks, where customers dispute charges with their credit card company. Chargebacks can be costly, involving fees, lost revenue, and potential damage to your merchant account reputation.

Mitigation:

Clear Cancellation Policies: Crystal-clear terms and conditions regarding cancellations, refunds, and travel changes are essential. Ensure these are easily accessible during booking.

Thorough Documentation: Maintain detailed records of all transactions, customer communications, and travel itineraries. This provides evidence in case of a dispute.

Proactive Communication: Keep customers informed about any changes to their travel plans and address concerns promptly.

Secure Payment Processing: Utilize 3D Secure (like Verified by Visa or Mastercard SecureCode) for added authentication and fraud prevention.

2. Fraud:

The Problem: The travel industry is an attractive target for fraudsters due to high transaction values and the potential for anonymity. Fraudulent activities can include using stolen credit card details, booking fictitious trips, or exploiting vulnerabilities in online booking systems.

Mitigation:

Address Verification System (AVS): Verify the billing address provided by the customer against the address on file with the credit card company.

Card Security Code (CVV): Always require the CVV code for card-not-present transactions.

Fraud Detection Tools: Implement fraud screening tools that analyze transactions for suspicious patterns and flag potentially fraudulent activity.

PCI DSS Compliance: Adhere to the Payment Card Industry Data Security Standard (PCI DSS) to ensure secure handling of sensitive cardholder data.

3. Currency Fluctuations:

The Problem: International travel often involves transactions in multiple currencies. Fluctuating exchange rates can impact your profit margins and create uncertainty in pricing.

Mitigation:

Dynamic Currency Conversion: Offer customers the option to pay in their home currency, providing transparency and potentially reducing chargebacks related to exchange rate discrepancies.

Hedging Strategies: Explore financial instruments to mitigate currency risk, such as forward contracts or currency options.

4. High Processing Fees:

The Problem: Travel agencies often face higher processing fees due to the perceived risk associated with the industry.

Mitigation:

Negotiate with Processors: Shop around and compare rates from different credit card processors. Don’t hesitate to negotiate for better terms, especially if you have a high volume of transactions.

Consider Interchange-Plus Pricing: Opt for transparent pricing models like interchange-plus, which separates the interchange fee (charged by card networks) from the processor’s markup.

5. Technological Challenges:

The Problem: Keeping up with evolving payment technologies and security standards can be challenging. Outdated systems can increase your vulnerability to fraud and data breaches.

Mitigation:

Invest in Secure Technology: Use a robust and secure online booking system that integrates with reputable payment gateways.

Regular System Updates: Ensure your software and security protocols are regularly updated to address emerging threats.

Partner with Reliable Providers: Choose payment processors and technology vendors with a strong track record of security and reliability.

By understanding and proactively addressing these credit card processing risks, travel agencies can protect their business, enhance customer trust, and navigate the exciting world of travel with greater financial security.

According to a poll by OnePoll on behalf of I Love Velvet titled “Consumer Mobile Point-of-Sale (MPOS) Attitudes Report” over half of retail customers think cash registers are outdated. The poll found that 51% of Americans think the cash register could soon be gone altogether as retailers opt for mobile point of sale systems. Consumers seem to favor MPOS systems allowing the shoppers to check out from anywhere in the store and that they return more often to stores with modern electronic payment technologies. Thirty five percent cited they would shop more often at stores with mobile point of sale payment systems. An additional 17% said they would share their shopping experience via social networking sites and 35% report they likely would tell a friend or recommend stores with these technologies. Forty six percent say that stores that have mobile payment systems seem to be more tech savvy and even more (56%) praise the store for making the experience more convenient and secure. Retailers are struggling to modernize their payment platforms to cut down long lines at registers, and place staff on the floor for better customer access. “It’s a great opportunity for retail store owners to dip into the mobile point of sale arena” said Richard Delos Santos of National Transaction Corporation.

Mobile point-of-sale equipment and software manufacturers are stepping up to the security plate as they seek to pass PCI DSS and other security related issues. As new mobile kiosks and point of sale hardware and software evolve so do the security challenges used to thwart credit card fraud and identity theft. The challenge for point of sale system providers is to create an increasingly secure and convenient way for customers to make electronic payments in-store or on their mobile devices. iPads, iPhones and Android tablets are often used by curious shoppers to compare and contrast features, prices and availability, why not let digital wallets be used to close the transaction? The use and connectivity of these new devices mean more complex security measures are needed to thwart attackers, crackers, and hackers.

In the coming years everything from NFC, to fingerprint readers in smartphones and tablets and even QR codes will change the landscape of mobile payment transaction processing and things are beginning to heat up. An estimated $17 Trillion of mobile transactions are predicted by 2020 and security and adoption will reign king on the streets. It might be time to look into the security and features that a mobile point-of-sale system can add over any existing point of sale systems and cash registers. Mobility is a great tool for a sales force, but security and convenience for the customer is a necessity that will only grow in the future.

In today’s fast-paced digital world, customers expect businesses to offer a variety of payment options. Electronic payment processing has become essential for businesses of all sizes, from small startups to large corporations. This article will provide you with all the information you need to know about electronic payment processing and why National Transaction Corporation is the best choice for your business.

What is Electronic Payment Processing?

Electronic payment processing refers to the electronic transfer of funds from a customer’s account to a business’s account. This can be done through various methods, including credit cards, debit cards, e-checks, and mobile payments. Electronic payment processing is faster, more secure, and more convenient than traditional paper-based methods.

Benefits of Electronic Payment Processing

Faster Processing Times: Electronic payments are processed much faster than paper checks, which can take several days to clear.

Improved Security: Electronic payment processing is more secure than traditional methods, as it uses encryption and other security measures to protect sensitive data.

Increased Convenience: Customers can make payments from anywhere at any time, using their computer, smartphone, or tablet.

Reduced Costs: Electronic payment processing can save businesses money on processing fees and other costs associated with traditional methods.

Improved Cash Flow: Businesses can receive payments more quickly, which can improve their cash flow.

Why Choose National Transaction Corporation?

National Transaction Corporation is a leading provider of electronic payment processing solutions. We offer a wide range of services to businesses of all sizes, including:

Credit and Debit Card Processing: We accept all major credit and debit cards, including Visa, Mastercard, American Express, and Discover.

E-Check Processing: We offer e-check processing services, which allow customers to make payments directly from their bank account.

Mobile Payment Processing: We offer mobile payment processing solutions, which allow customers to make payments using their smartphone or tablet.

Online Payment Processing: We offer online payment processing solutions, which allow businesses to accept payments through their website.

At National Transaction Corporation, we are committed to providing our clients with the best possible service. We offer:

Competitive Rates: We offer competitive rates on all of our services.

Reliable Service: We provide reliable service that you can count on.

Excellent Customer Support: We offer excellent customer support, available 24/7.

Secure and Compliant Solutions: We are PCI DSS compliant, ensuring the security of your customers’ data.

Make the Switch to Electronic Payment Processing Today

If you’re not already accepting electronic payments, now is the time to make the switch. National Transaction Corporation can help you get started with our easy-to-use and affordable solutions. Contact us today to learn more about how we can help your business grow.

Travel agencies are viewed as high-risk merchants. As such, you need a merchant solution that best suits a travel merchant needs.

You want an account that eliminates the complexities of a typical shopping cart. Ideally, it allows you to request payment from clients without the need of setting up booking engines and carts.

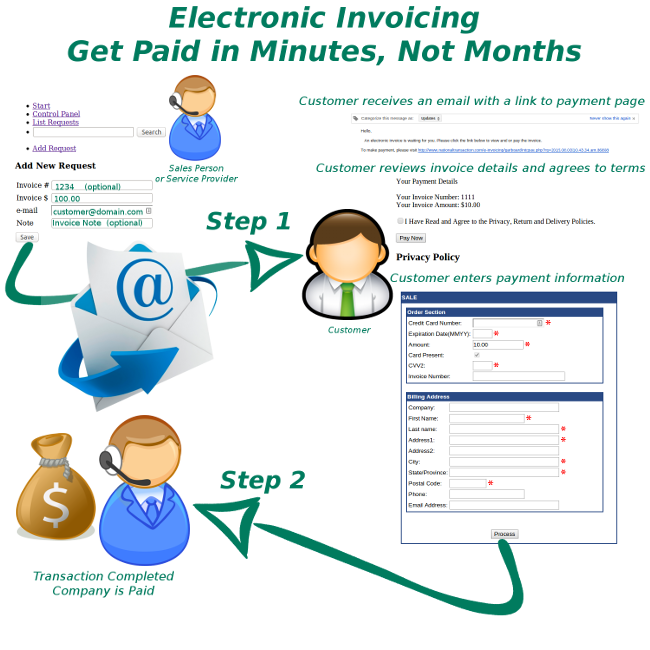

This post is going to guide you on how to use a payment solution NTCePay and other merchant solutions to ensure a seamless operation of your business.

Payment solution e-Pay allows you to eliminate the complexities of integrating payment processing into your point-of-sale or an accounting system.

With this payment method, you only need to send a payment request to your customers via email. You don’t need to send invoices via snail mail or fax any forms to your customers. Plus, NTC ePay doesn’t need you to take orders over the phone.

With this service, you can create a “BUY” button for any transaction amount in seconds. You also don’t need a website to you use this service. NTCePay allows you to generate a digital link that you can email to clients.

The service allows you to customize the process to make everything simple for your customers. After the customer pays the specified amount, a receipt is generated, and the amount is sent to your account.

Tomorrow we are going to discuss on how to understand your Travel Merchant Account….So standby to learn more.

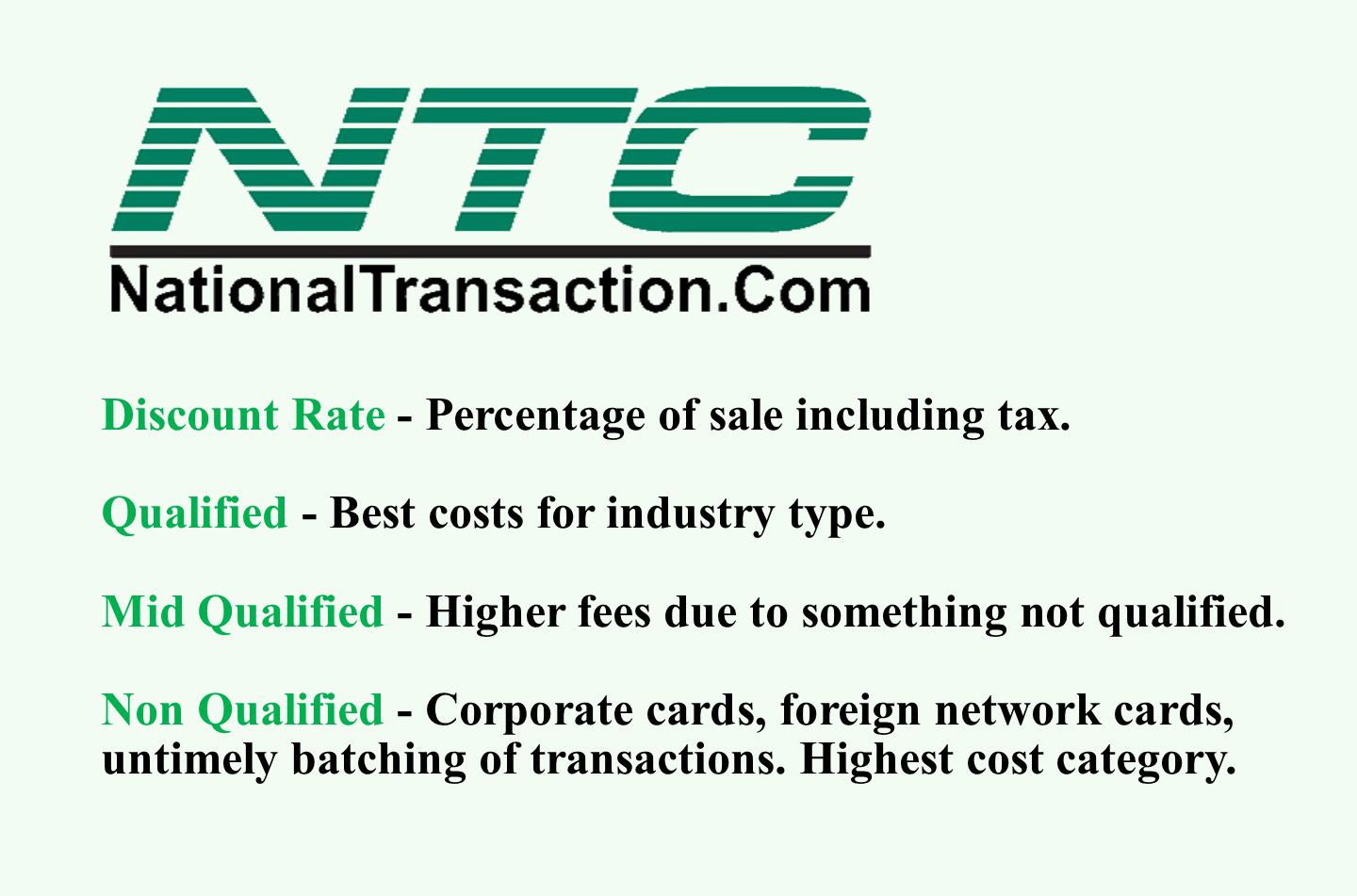

Credit card transaction types are categorized based on the level of risk and processing cost associated with them. Here’s a breakdown of the common types:

1. Qualified

Definition: These are considered the “safest” and least expensive transactions for processors to handle.They typically involve traditional credit or debit cards processed in person with a physical card swipe or chip insertion.

Characteristics:

Card is present during the transaction

Cardholder’s signature is captured (if required)

AVS (Address Verification Service) matches the billing address on file

CVV (Card Verification Value) is provided and matches

Transaction meets all security protocols and risk assessment criteria set by the card issuer and processor.

Examples:Swiping a standard Visa or Mastercard credit card at a retail store.

2. Mid-Qualified

Definition: These transactions fall in between qualified and non-qualified in terms of risk and processing cost. They often involve card-not-present transactions or cards with higher reward structures.

Characteristics:

Manually keyed-in transactions (online, over the phone, or mail order)

Rewards cards with higher cashback or points benefits

Business or corporate cards

Transactions where AVS or CVV information is not provided or doesn’t match

Examples: Entering your credit card details online to purchase something, using a rewards card with travel benefits.

3. Non-Qualified

Definition: These transactions are considered the riskiest and most expensive to process.They often involve international cards, manually keyed transactions without proper security measures, or cards with very high reward programs.

Characteristics:

International credit cards

Manually keyed transactions without AVS or CVV verification

High-risk businesses like online gambling or adult entertainment

Keyed transactions for business or corporate cards

Examples: Using a foreign-issued credit card, manually processing a transaction without verifying the cardholder’s address.

Why does this matter?

Processing Fees: Merchants are charged different fees for each transaction type.Qualified transactions have the lowest fees, while non-qualified transactions have the highest.

Tiered Pricing: Many payment processors use tiered pricing models, categorizing transactions into these types and charging accordingly. This can sometimes be confusing or lead to unexpected costs for merchants.

Interchange Fees: The card networks (Visa, Mastercard, etc.) also charge interchange fees for each transaction, which vary based on factors similar to those used for transaction type categorization.

Understanding these transaction types is crucial for merchants to:

Negotiate better processing rates: By understanding the factors that influence transaction categorization, merchants can negotiate better fees with their processors.

Optimize payment processing: Merchants can take steps to minimize the number of mid-qualified and non-qualified transactions, such as encouraging in-person payments or using address verification systems.

Control costs: By being aware of the different transaction types and their associated costs, merchants can better manage their payment processing expenses.

Remember: The specific criteria for each transaction type can vary depending on the payment processor, card network, and individual merchant account. It’s always best to clarify with your payment processor to understand their specific categorization rules and fee structures.

To establish a merchant account for your business call now 888-996-2273 or click here NationalTransaction.Com

Over the next three weeks we will explore on this blog some of the reasons why National Transaction Corporation is the preferred choice for travel agents.

The Travel industry is one of the world’s largest industries with a global economic contribution of over 7.6 trillion U.S. dollars in 2016. (Statista)

At NTC we recognize that travel agency payment processing has some unique hurdles to overcome, but we are leveraging our innovation because we want our travel agency partners to explore how our solutions transcend the challenges that travel agents face.

Secure processing is one of the reasons why National Transaction is the preferred choice for travel agents

National Transaction Corporation has Secure Merchant Payment Processing – Because when your customers know their data is safe, they keep coming back!

You’ve heard of the many data breaches within major corporations that have occurred in just the last few years, when customers’ confidential credit card information is stolen and businesses lose a small fortune in repairing the problem. The cost of such a security breach goes far beyond that, however; once a business has lost the trust of its customers, 60% of those cardholders will go elsewhere for their purchases and services, according to studies on the problem.

Imagine if this happened to your travel agency merchant account? It could be disastrous, especially because agencies tend to deal with high-dollar sales from a moderately-sized pool of customers – so every client counts.

NTC knows that you, like us, care about your customers, and we want your travel agency to be seen as a trustworthy place to book a dream vacation. The first step is for your business to be PCI-DSS compliant.

PCI-DSS (Payment Card Industry-Digital Security Standards) requirements were put in place by the credit card associations to deal with the increasing problem of identity theft and data loss. The requirements vary according to the types and the number of payment transactions your agency goes through, but you can be sure that NTC will help you stay compliant with the latest security standards.

In the event of a data breach, we are here to eliminate the negative impact it can have on your company. NTC may be able to help you with the fines, assessments, and other costs from the networks, and we will consult with you on how to proceed to protect your agency and your reputation.

As you know, data security is as much a concern for the business owner as it is for the cardholder – your customer. When your clients know that their data is safe with you, they will keep coming back to your agency to book their next great trip!

If you cannot wait to read blog number two out of this three part series, feel free to call NTC now at 888-996-2273 to find out the best options for your travel agency!

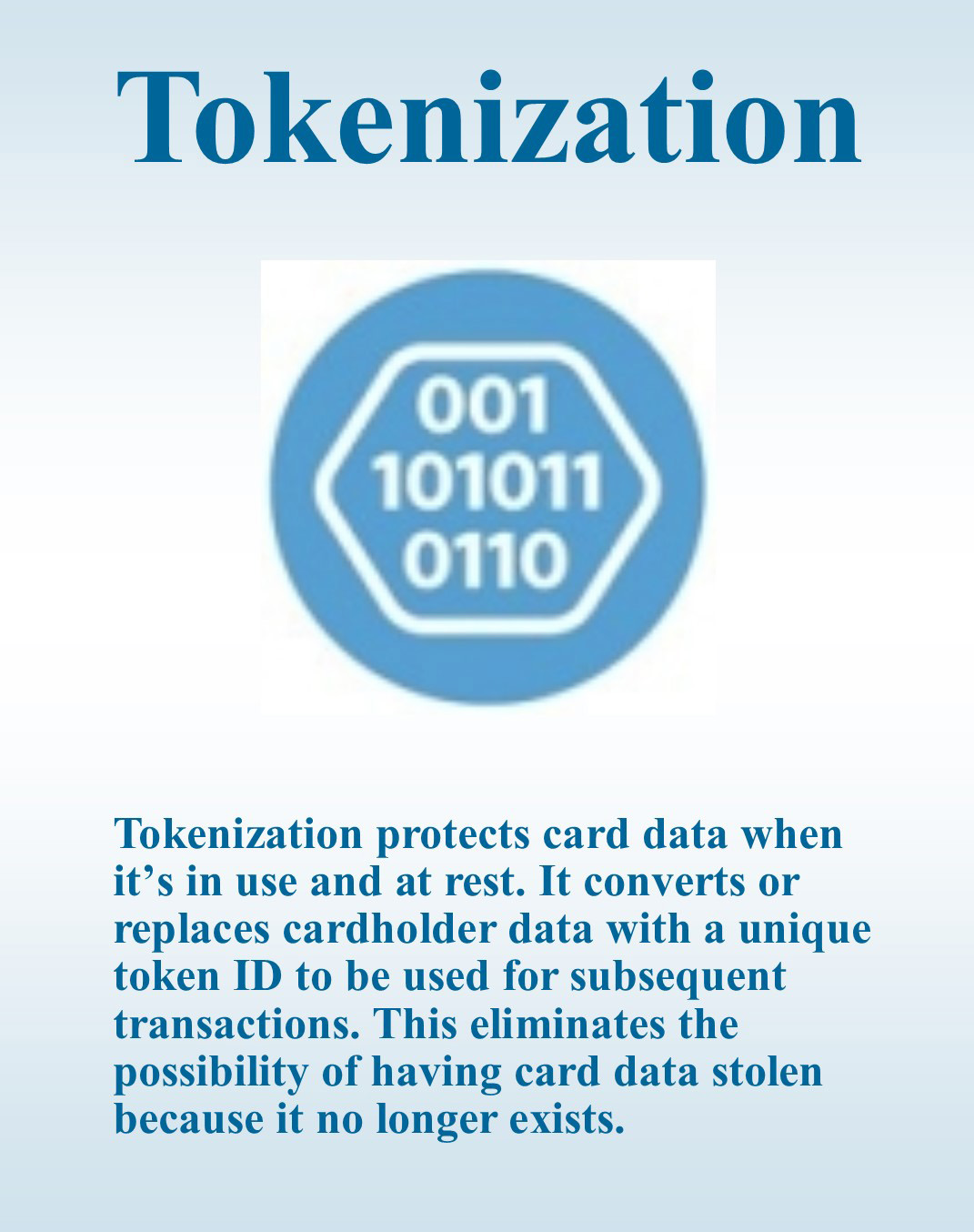

Tokenization is a powerful security feature that allows a merchant to support all of their existing business processes that require card data without the risk of holding card data and without any security implications, because tokens are useless to criminals, they can be saved by the merchant as they do not represent any threat.

The liability and costs associated with PCI compliance is substantially reduced and the risk of storing sensitive data is eliminated.

Tokenization applies to credit card and gift card transactions.

Imagine a world where you could accept credit card payments without actually storing any sensitive cardholder data. No more worrying about data breaches, PCI compliance headaches, or the crippling costs of a security breach. That’s the power of tokenization.

Here’s how it works:

Instead of storing sensitive credit card information on your systems, each card number is replaced with a unique, randomly generated “token.” This token is useless to hackers, but it can be used to process payments securely on the merchant account that created the token.

Think of it like a valet ticket:

You hand over your car (the sensitive data) to the valet (the tokenization provider), who gives you a unique ticket (the token). The valet keeps your car safe, and you can use the ticket to retrieve it when needed.

The benefits are immense:

Ironclad Security: Reduce your PCI DSS scope and minimize the risk of costly data breaches. With tokenization, even if your system is compromised, the actual card data remains safe.

Effortless Compliance: Simplify PCI compliance and avoid hefty fines. Tokenization helps you meet the stringent security requirements for handling sensitive cardholder data.

Recurring Billing Made Easy: Securely store tokens for recurring billing or future transactions. This allows you to charge customers later without having to store their sensitive information.

Improved Customer Trust: Demonstrate your commitment to data security and build customer trust. Knowing their information is protected encourages repeat business and loyalty.

Streamlined Checkout: Offer a frictionless checkout experience with saved payment information. Tokenization enables faster and more convenient payments for your customers.

Tokenization is not just a security measure, it’s a strategic advantage:

Reduce costs: Minimize the expenses associated with data breaches and PCI compliance audits.

Boost efficiency: Streamline your payment processes and reduce administrative overhead.

Enhance your reputation: Position your business as a leader in data security and customer trust.

In conclusion:

Tokenization is a game-changer for businesses that accept credit cards. It offers unparalleled security, simplifies compliance, and unlocks new opportunities for growth. Embrace the future of secure payments with tokenization and watch your business thrive.

For Electronic Payments with Tokenization call now 888-996-2273 or click here NationalTransaction.Com

Visa 3-D Secure (3DS) is a security protocol designed to add an extra layer of protection to online credit card transactions.It aims to reduce fraud by verifying the cardholder’s identity before the transaction is authorized.Visa’s implementation of 3DS is called “Visa Secure.”

Here’s how it works:

Transaction Initiation: When a customer makes an online purchase with their Visa card, the merchant’s website communicates with the Visa network to initiate the 3DS process.

Risk Assessment: The issuer (the cardholder’s bank) performs a risk assessment based on various factors, such as the cardholder’s history, the transaction amount, and the merchant’s risk profile.

Authentication: If deemed necessary, the issuer challenges the cardholder to authenticate their identity. This usually involves a step-up authentication method, such as:

One-time password (OTP): Sent to the cardholder’s registered mobile phone or email.

Biometric authentication: Fingerprint scan or facial recognition.

Knowledge-based authentication: Security questions or personal information.

Verification: Once the cardholder successfully authenticates, the issuer confirms their identity to the merchant.

Transaction Completion: The merchant can then proceed to process the transaction with increased confidence that the cardholder is legitimate.

Integration and Implementation:

Merchants need to integrate 3DS into their online payment systems.This typically involves working with their payment gateway provider or acquiring bank to implement the necessary APIs and protocols.Visa provides detailed documentation and support for merchants to integrate Visa Secure.

Benefits and Features of 3DS:

Reduced Fraud: By verifying the cardholder’s identity, 3DS significantly reduces the risk of unauthorized transactions and chargebacks.

Improved Security: Adds an extra layer of security to online payments, protecting both merchants and customers from fraud.

Shift in Liability: In many cases, if a fraudulent transaction occurs after successful 3DS authentication, the liability shifts from the merchant to the issuer.This can save merchants significant costs associated with chargebacks and fraud disputes.

Increased Customer Confidence: Demonstrates a commitment to security and builds trust with customers, encouraging them to complete their purchases.

Enhanced User Experience: The latest version of 3DS (EMV 3DS 2.0) offers a smoother and more user-friendly authentication experience, minimizing friction during checkout.

Support for Mobile and Digital Wallets: 3DS is compatible with various payment channels, including mobile devices and digital wallets, providing a consistent and secure experience across all platforms.

In conclusion: Visa 3-D Secure is a powerful tool for merchants to enhance the security of their online transactions, reduce fraud, and improve customer confidence.

By implementing Visa Secure, merchants can protect themselves from financial losses and provide a safer and more trustworthy shopping experience for their customers.

For e-Commerce Electronic Payments set up with 3D Secure

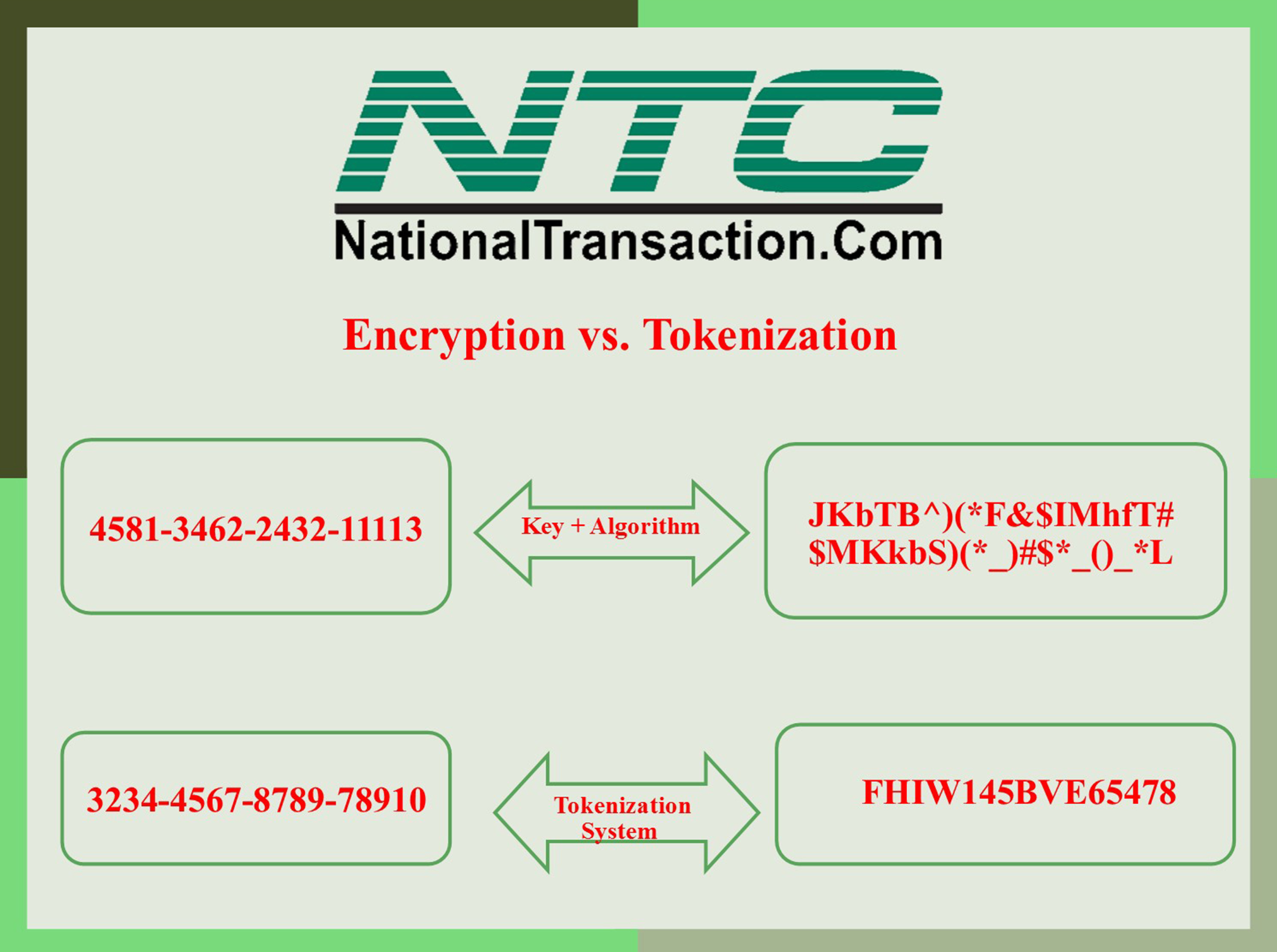

Encryption is reversible. Encrypted data can be returned back to its original, unencrypted form. The encryption strength is based on the algorithm it uses. A more complex algorithm will create stronger encryption to secure the data. Encryption is most often “end-to-end.”

PCI Security Standards Council and other governing compliance entities still view encrypted data as sensitive data.

Tokenization system replaces sensitive data and the token cannot be reversed into true data, it has no value. The real, sensitive information is stored in a secured offsite platform. An entirely different location. That means sensitive customer data does not enter or reside within your environment.

Unlike encryption, tokenization isn’t subject to issues with PCI/DSS compliance or other data security organizations, because tokens do not contain any real data.

If a hacker managed to steal your tokens they cannot be used for a fraudulent transaction.

Using tokens doesn’t change a merchant’s payment processing experience as it protects their valuable credit card information.