Merchants are constantly trying to find ways to improve their customer experience, like customer service and loyalty programs, but the one that is often overlooked is offering a variety of payment options.

Offering a variety of payment options can lead to your customer experience success. With more and more customers using alternative forms of payment and staying away from the traditional way which is cash and credit card.

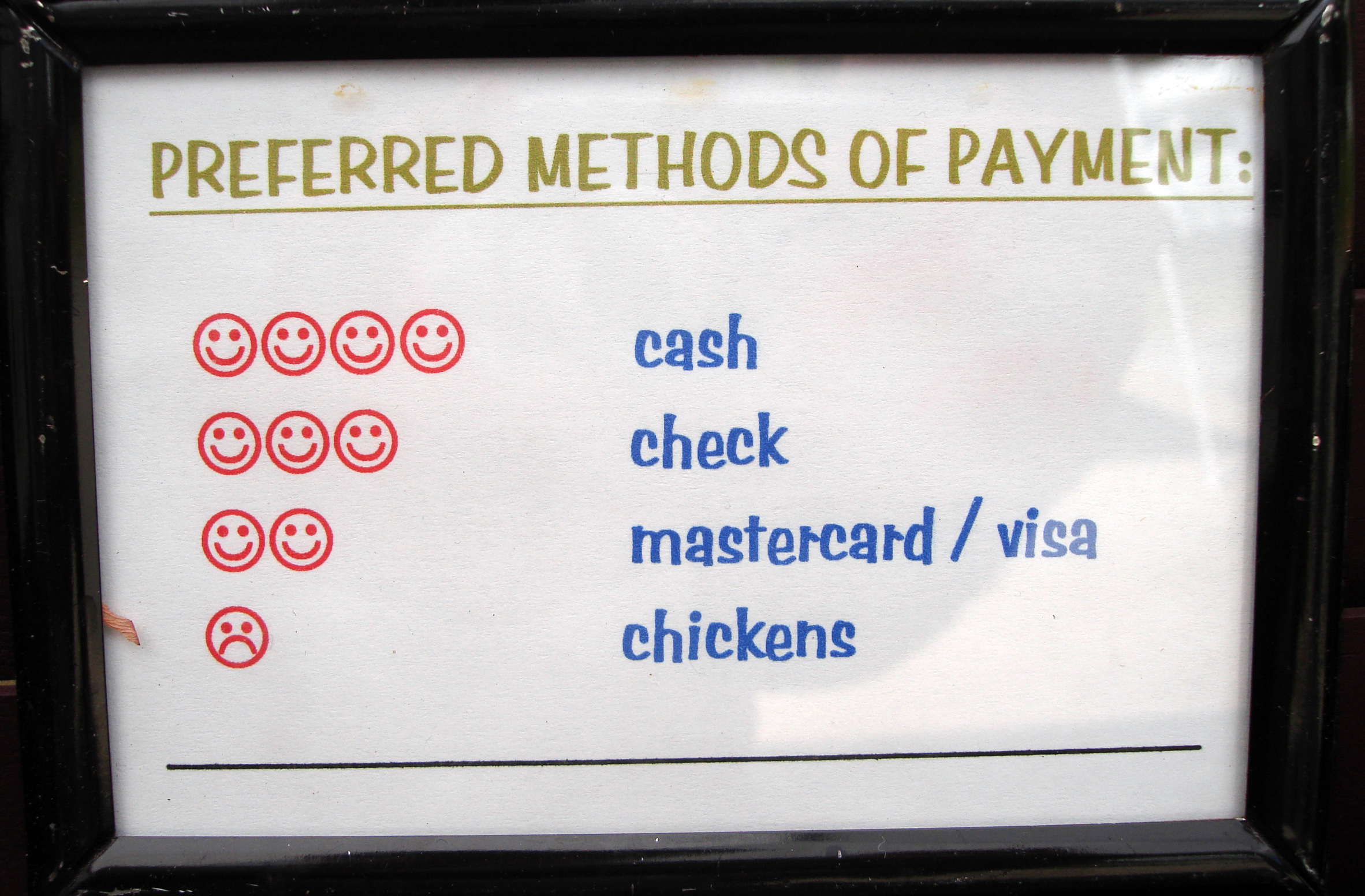

Types of Payment Options:

E-Commerce – Online shopping is growing, your business should be adopting this trend. Merchants who do not currently offer an online store should consider taking their sales online. This will gain more exposure and will also enhance the overall customer experience.

Mobile Wallets – Consumers are becoming more comfortable doing transactions on their smartphone, by accommodating mobile wallets, your business can attract more customers and more sales for your business. Upgrading your point-of-sale (POS) to be a Near field communication (NFC)-enabled will allow you to accept any mobile wallet payment.

Offering a variety of payment options will help your business stay up to date. More payment options mean more customers. If you would like to expand your current payment processing options for your business, visit www.nationaltransaction.com or talk to our Payments Expert today at 888-996-2273 Extension 1.

Cardless ATM’s Could Help Push Mobile Wallet Adoption

The mobile wallet will be the payment method in five to 10 years.

Cardless ATM transactions is a great way to introduce smartphones as payments devices. It could help with the adoption of mobile payments and wallets. Mobile Smart Phones will become the piece of plastic and cards will be a thing of the past…

A multinational banking corporation intends to use (NFC) near-field communication for its service. It will let customers leverage NFC technology on their smartphones to authenticate at the bank’s ATM without a debit card.

An NFC cardless ATM transactions could be compatible with Apple Pay which uses NFC technology.

Benefits:

Speedier ATM cash withdrawal takes about 15 seconds without the debit card compared with 60 to 90 seconds with a debit card, whether it’s a chip or magnetic-stripe transaction.

Safer ATM transaction. No physical connection between the phone and ATM, skimming device to intercept the transaction is gone.

The barcode represents the time of day and what terminal the transaction is taking place at. Everything is tokenized.

Cardless ATM transactions are interesting and an appropriate evolution.

NTC ePayis an easy and effective way to process transactions for any Merchants.

National Transaction creates a custom link for your business, which you will use to send your customers an Electronic Invoice. Once your customer received the invoice, they will click on the link and pay the amountonthe invoice.

The customer is required to agree to your Refund Policy, Privacy Policy, Timing and Delivery Policy before they can pay the invoice, this will protect you in a caseof a Chargeback.

With this system in place, Credit Card information is processed securely. The customer is entering their credit card information without faxing or emailing credit card numbers.

Electronic Invoicingsaves time and unnecessary costs. Documents don’t need to be scanned or email, all transactions are processed through the electronic invoice making it easy to keep track of.

Most of our Merchants usingNTC ePayare in the Travel Industry, some are into boat Repair Business and Church Ministries. If you want to process securely, save time and unnecessary costs like our existing merchants, check out NTC ePay, The No Shopping Cart e-Commerce Solution!

E-Pay Security improves – but merchants remain cautious.

U.S. merchants are still reluctant to embrace 3D Secure technology in card-not-present transactions, even though it has vastly improved from the initial version.

3D secure technologies – namely Verified by Visa and SecureCode for MasterCard which offer an extra layer of protection for merchants and its customers. Merchant participation is mandatory to process certain cards in some countries.

The shift to EMV is helping to address vulnerabilities in the United States payments ecosystem. It has been shown that EMV can deliver benefits as a part of industry efforts to combat fraud.

EMV migration is a critical focus for enhancing payments security, which is why the current efforts around chip card deployment are greatly beneficial for consumers and merchants alike. EMV technology helps to reduce counterfeit card fraud, as it generates dynamic data with each payment to authenticate the card, after which the cardholder is prompted to sign or enter a PIN to confirm their identity.

The EMV rollout represents a dynamic time for card payments that promises great advances, among them is enhanced security for cardholders. It also presents an opportunity to consider other innovations such as mobile wallets and mobile POS to further engage your customers and drive customer loyalty. When merchants continue to invest in EMV and NFC (near field communications, used for tap-and-pay transactions), the purchases made at their EMV-enabled terminals are made more secure than magnetic stripe.

New mobile payment options such as mobile wallets support EMV and therefore offer this added layer of security. Ultimately, by enabling contactless payments, merchants can also enable more flexibility in addition to increasing security for their customers.

Additionally, industry players are backing major mobile wallets, such as Android Pay, Apple Pay, and Samsung Pay.

Fighting chargebacks is important to business. Whether you process transactions at a point of sale location or operate an e-Commerce business making sure you have implemented a process to dispute your chargebacks is critical.

Basic concepts that can be used to begin learning how to dispute chargebacks for Visa and MasterCard transactions:

Keep accurate records of data that is easily accessible. Keeping track of your sales and products have a much easier time in collecting the information necessary to combat a chargeback.

Act quickly. Don’t wait until you only have a few days left to respond to a chargeback or retrieval request. Responding in a timely fashion shows your processor that this is of concern to you and that you’re taking matters seriously.

Create chargeback packets or templates. These allow you to quickly input specific relevant transaction information to support your view of the transaction being valid. Packets should include documents that support your case against the chargeback.

Compile and submit your packet to your processor in the form that is most convenient for both you and them. Make sure the packet has the original chargeback documents attached as well as your packet with supporting documents.

Monitor your chargebacks to see which ones you’re successful on and which you’re not. This will help you understand what processes are work for each specific chargeback type.

The convenience, simplicity and security of Apple Pay are now available to customers who use U.S. Bank FlexPerks American Express Cards.

U.S. Bank which is the fifth-largest bank in the nation will add TouchID biometric capabilities to its mobile app in March.

The company made the disclosure as part of a notable iOS app update released last Friday. Release appears to include, among other enhancements, improvements such as easier navigation, quicker accessibility to account information, and the ability to search transactions from previous months.

U.S. Bank Minneapolis did not give many details about how TouchID will be used within its iOS app, other than to say for fingerprint authentication for enabled devices.

Many major banks already have TouchID implemented in their mobile apps, including Citibank, Wells Fargo and Bank of America. Citibank, for example, implemented TouchID last July. Apple introduced TouchID in mid-2013.

Last week, U.S. Bank enabled for Apple Pay use the last of its debit and credit cards that had not been Apple Pay-capable. Apple Pay relies on TouchID for security and authentication.

Apple Pay is now available with the:

U.S. Bank FlexPerks Reserve American Express Card.

U.S. Bank FlexPerks Travel Rewards American Express Card.

U.S. Bank FlexPerks Select+ American Express Card.

Merchant accounts are as varied as the merchants themselves and the goods being sold.

What kind of account would you fall under:

High Risk Merchant Accounts – Finding a processor who is willing to take your account can be more challenging. High risk merchants range from travel agencies to multi-level marketing companies, credit restoration merchants, casinos, online pharmaceutical companies, adult/dating merchants and many other.

Internet based merchant account (Ecommerce/Website order processing) – E-Commerce is a booming market, with so many people buying and selling goods online due to the wide reach and easy access to the internet.

Mobile or Wireless merchant account – This merchant is specifically designed for small businesses, solo professionals, and mobile services (including lawyers, landscapers, contractors, consultants, repair tradesmen, etc), who are constantly on the move and require a payment to processed on the spot.

MOTO (Mail or Telephone order) – This enables phone based or direct mail orders processing for customers who can buy your product or service from the comfort of their home. Since there is no card present there is no need for traditional equipment.

Multiple Merchant Accounts – Some businesses can have merchant accounts of a couple or all different types. Merchants who fall into this category are called multi-channel merchants as they sell their goods through a number of different channels. Most commonly this is related to retail stores who also have an online presence to sell their goods. This is very common in today’s competitive market where constant contact with customers is critical to success.

Traditional Account with Equipment – Most commonly used for retail businesses (grocery, departmental stores etc) where the transactions are processed in a face to face interaction also known as Point of Sale (PoS).

Interested to setup an account give us a call at 888-9962273

The business is already making upgrades, so If you’re a merchant, business owner who’s still on the fence about upgrading your payment processing equipment to accept EMV cards why not take that upgrade a step further and add NFC while adding EMV systems?

Not only will the upgrade help prevent potential financial responsibility for fraudulent transactions, but you can also realize the added benefit of being able to process NFC transactions at the same time.

Customers want the ability to pay with a mobile device, and NFC will allow for such transactions to go on.

Having NFC tools in place will help provide a valuable note of future-proofing to systems in place, being ready for it will be to the business’ benefit.

EMV and NFC technology is just good business sense for three important reasons Added Security, Economic Sense and Staying Current.

For more information about terminal upgrade and features that suits best for your business give us a call at 888-996-2273.

Can we securely store card data for recurring billing?

PCI DSS discourages businesses from storing credit card data, Merchants feel the practice is necessary in order to facilitate recurring payments.

The Payment Card Industry Data Security Standard (PCI DSS) is a proprietary information security standard for organizations that handle branded credit cards from the major card schemes including Visa, MasterCard, American Express, Discover, and JCB.

In order for the electronic storage of cardholder data to be PCI Compliant, appropriate encryption must be applied to the primary account number (PAN). In this situation, the numbers in the electronic file should be encrypted.

All PCI controls would apply to the environment in which the cardholder data is transmitted and stored. Tokenization can be implemented for recurring and/or delayed transactions. Travel Merchants and or Storage Facility could use this feature to help reduce the need for electronically stored cardholder data while still maintaining current business processes.

The best thing you can do for your business is to not store any cardholder data or personally identifiable information.

Tomorrow let’s tackle Encryption and Tokenization a strong combination to protect card data while reducing the cost of compliance!