April 6th, 2017 by Elma Jane

Payment types and it’s categories

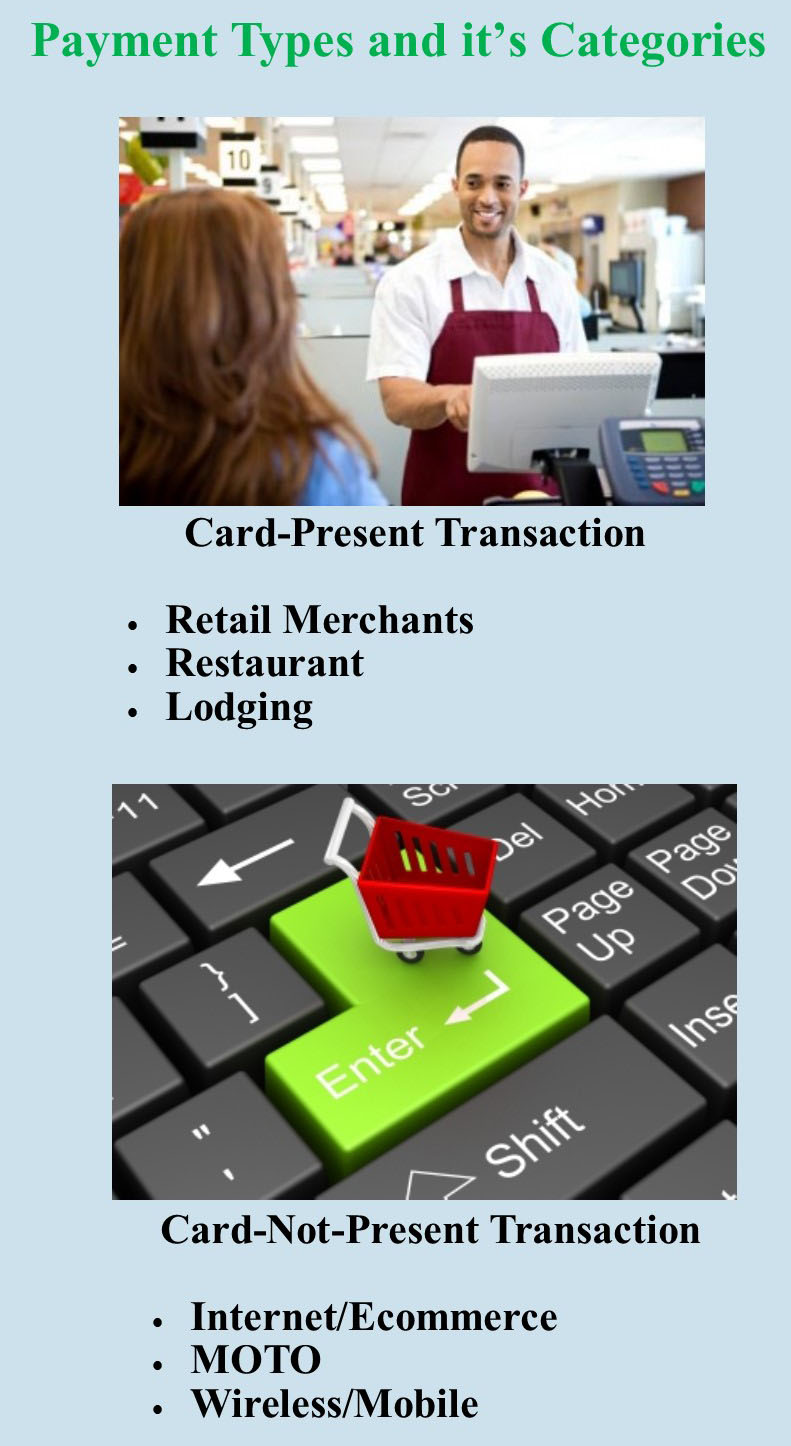

The two main category types when it comes to credit card processing are swiped and keyed. Card present or card-not-present.

Swiped or card present transaction – merchants do a face-to-face transaction. A merchant can capture card information by dipping the chip or swiping the card in the terminal or POS. Merchants directly interact with a customer so the risk is low.

Card-Present Sub Categories:

Retail Merchants – conduct transactions face to face in a retail environment.

Face to Face (mobile) – this type of merchant is typically on the go, such as a vendor at a trade show. You can use a service like converge mobile that allows you to take the information in person.

Restaurant – the same as retail merchants, the difference is they may require the ability to add tips to their charges.

Lodging – processes their transactions like retail merchants except they may adjust the settlement amount depending on the customer’s length of stay.

Keyed or card-not-present are high risk, because merchants indirectly collect customers card information, and can process transactions in various ways.

Card-Not-Present Sub categories:

Internet/Ecommerce – conducts business through a web site by utilizing a shopping cart and an Internet payment gateway service. The payment gateway then collects the credit card information and processes it in real time.

Mail & Telephone Order (MOTO) – typically take the customer’s credit card information over the phone, by mail or through the Internet. They then manually process the transaction by keying it into either a credit card machine or through a virtual terminal such as Converge.

Talk to our payment consultant to know the best solution for your business.

NationalTransaction.Com 888-996-2273

Posted in Best Practices for Merchants Tagged with: card present, card-not-present, credit card, customer, ecommerce, merchants, payment, payment gateway, POS, swiped and keyed, terminal, virtual terminal

April 14th, 2016 by Elma Jane

Accepting credit card payments is a must if you’re planning to start a business. It’s good to know what is out there and how it applies to your situation. So you need to learn about credit card processing machines, depending on your business.

Here are some of the different types of credit card processing machines:

Dial-Up Terminal – the grandfather of credit card processing machines. Dial-up terminals use a phone line to connect with a credit card processing company. The advantage is that they are normally inexpensive than some higher-end options. The disadvantage is slower processor speed.

IP Terminal – connect the merchant over a high-speed internet connection. The advantage of IP terminal over dial-up terminal is speed. IP machines can process transactions as fast as 3 seconds as opposed the 10 to 25 seconds that a dedicated dial-up machine might take. IP terminals now cost about the same as dial-up units and that a single DSL link can accommodate more than one credit card terminal.

Wireless Terminals – the priciest yet most convenient type is a wireless machine that runs on a wireless network, much like your mobile phone.

Virtual Terminal – virtual terminals are computers running credit card processing software connected to a credit card reader. Virtual terminals are a great addition to an office because they don’t require a standalone credit card processing terminal.

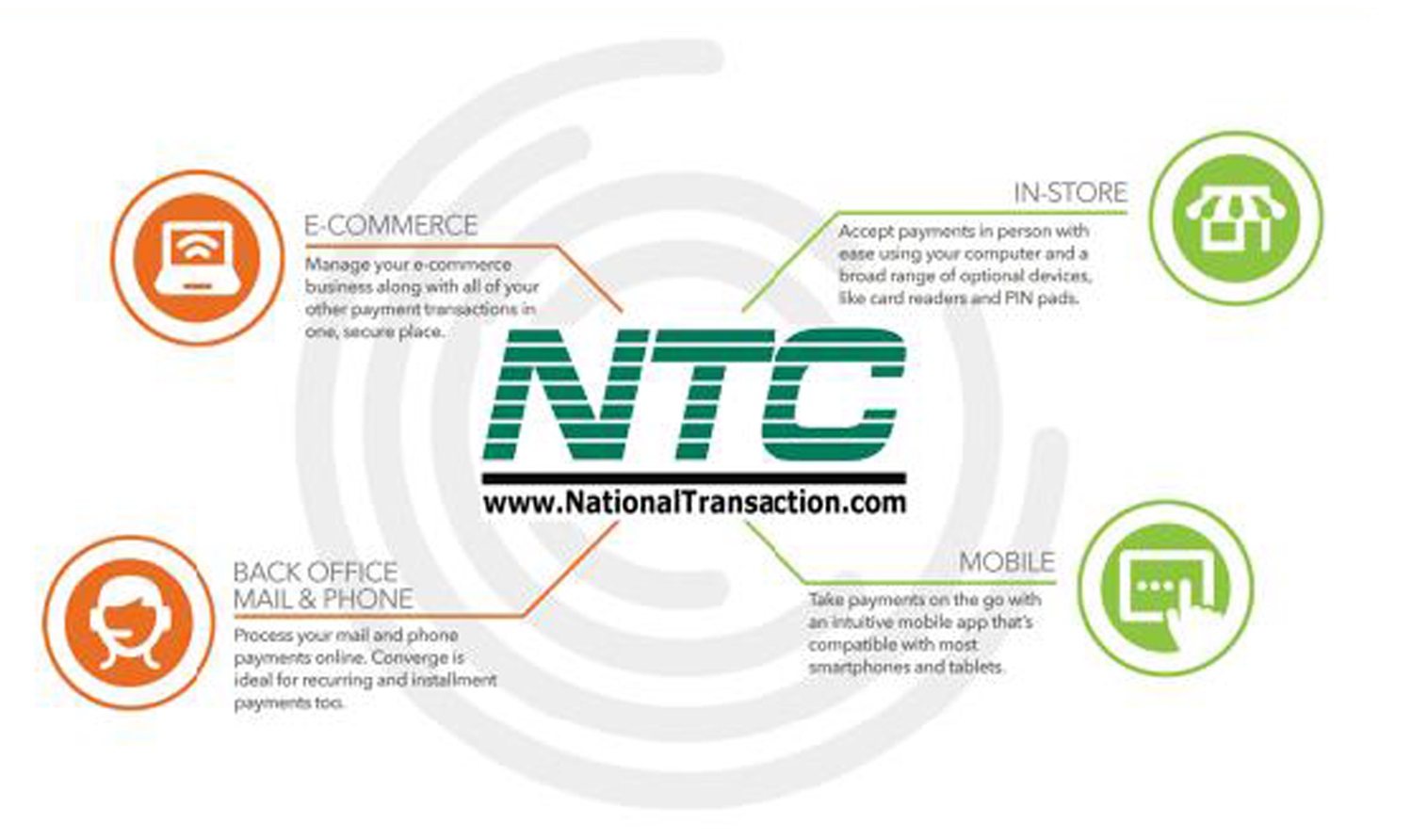

There are many options available for your business, whether you’re e-Commerce, MOTO, In-Store or Mobile there’s a credit card processing machine and platform out there that will fit your business.

Give us a call to know more at 888-996-2273 or visit us at www.nationaltransaction.com

Posted in Best Practices for Merchants, Credit Card Reader Terminal, e-commerce & m-commerce Tagged with: card reader, credit card, credit card processing, e-commerce, merchant, mobile, moto, payments, terminal, virtual terminal

November 13th, 2015 by Elma Jane

It’s important for merchants to understand the basic of how a credit card terminal works. It is the channel through which the process flows and the merchants can choose the right one for their processing needs, whether they use a point-of-sale (POS) countertop model, a cardreader that attaches to a smartphone or mobile device, a sleek handheld version for wireless processing or a virtual terminal for e-commerce transactions.

A credit card terminal’s function is to retrieve the account data stored on the payment card’s EMV microchip or a magnetic stripe and pass it along to the payment processing company (also known as merchant account provider).

For card-not-present (CNP) – mail order, telephone order and online transactions – the merchant enters the information manually using a keypad on the terminal, or the e-commerce shopper enters it on the website’s payment page. The back half of the process remains the same.

The actual data transmission goes from the terminal through a phoneline or Internet connection to a Payment Processing Company, which routes it to the bank that issued the credit card for authorization.

In card-present transactions where the card and cardholder are physically present, the card is connected to the reader housed in the POS terminal. The data is captured and transmitted electronically to the merchant account provider, who handles the authorization process with the issuing bank and credit card networks.

A POS retail terminal with a phone or Internet connection works best in a traditional retail setting that deals exclusively in card present transactions. For a business with a mobile sales, a mobile credit card processing option like Virtual Merchant Converge Mobile relies on a downloadable app to transform a smartphone or tablet into a credit card terminal equipped with a USB cardreader.

Wireless Terminals are compact, allowing you to accept credit cards in the field without relying on a phone connection. If you process debit cards, you’ll need a PIN pad in addition to your terminal so cardholders can enter their personal identification number to complete the sale.

Selecting the right terminal for your credit card processing needs depends largely on the type of business you run and the sorts of transactions you process. Terminals are highly specialized and provide different services. At National Transaction we offer a broad range of terminals with NFC (near field communication) Capability to accept Apple Pay, Android Pay and other NFC/Contactless payment transactions at your business. An informed business decision benefits your bottom line. Start accepting credit cards today with National Transaction.

Posted in Best Practices for Merchants, Credit card Processing, e-commerce & m-commerce, EMV EuroPay MasterCard Visa, Mobile Point of Sale, Point of Sale Tagged with: Android Pay, Apple Pay, card-not-present, card-present transactions, cardholder, cardreader, cnp, contactless payment, Converge Mobile, credit card, credit card networks, credit card terminal, debit cards, e-commerce, EMV, magnetic stripe, mail order, merchant account provider, merchants, microchip, mobile credit card processing, mobile device, Near Field Communication, nfc, online transactions, payment processing company, PIN pad, point of sale, POS, POS terminal, smartphone, telephone order, virtual merchant, virtual terminal, wireless processing

October 11th, 2013 by Elma Jane

(Moto) Mail Order/Telephone Order Merchant – In the realm of credit card processing is defined as a merchant who manually keys in over 50% of their transactions and an Internet Merchant is one who accepts transactions over the Internet via an E-Commerce store with an online gateway or who submits transactions manually through a Virtual Terminal.

Qualified Transaction Conditions (For MOTO/Internet merchants the Mid-Qualified Rate is essentially the Qualified rate as these merchants never swipe a credit card through a terminal.)

One electronic authorization request is made per transaction and the transaction date is equal to the shipping date. The authorization response data must also be included in the settled transaction.

Additional data (sales tax and customer code) is required in the settled transaction on all commercial (business) cards at non-Travel & Entertainment (T&E) locations.

The authorization request message must include Address Verification Service (AVS), which verifies the street address and the zip code of the card holder. NOTE: The only way this happens is if your software is set up to do this, or, if you are using a terminal, then if you capture the AVS information at the time of keying in your transaction.

The settled transaction amount must equal the authorized amount.

The settled transaction must include the business’s customer service telephone number, order number, and total authorized amount.

The transaction is electronically deposited (batch transmitted) on or 1 day after authorization date.

The transaction/shipping date must be within 7 calendar days of authorization date.

Non-Qualified Transaction Conditions

One or more of the Qualified or Partially Qualified conditions were not met.

Commercial Card without the additional data.

The transaction was not electronically authorized or the authorization response data was not included in the settled transaction.

The transaction was electronically deposited (batch transmitted) greater than 1 day from transaction/shipping/authorization date, or:

The VISA Infinite card was accepted.

Commercial Card Additional Data

MasterCard

Corporate Data Rate II (Purchasing cards): Sales Tax and customer Code (supplied by cardholder at point of sale) Corporate Data Rate II (Business and Corporate cards): Sales Tax International Corporate Purchasing Data Rate II: Sales Tax and Customer Code (supplied by cardholder at point of sale)

The following information must also be provided: Merchant’s Federal Tax ID; Merchant Incorporation Status; and Owner’s full name if the merchant is a sole proprietor.

Visa

Purchasing cards: Sales Tax and Customer Code (supplied by cardholder at point of sale) Corporate and Business cards: Sales Tax

Posted in Credit card Processing, e-commerce & m-commerce, Electronic Payments, Internet Payment Gateway, Mail Order Telephone Order Tagged with: address verification service, authorization, avs, batch, business, corporate, credit card processing, data, e-commerce, electronically, entertainment, fax order, gateway, internet, internet merchant, keying, mail order, moto, phone order, qualified, settle, store, telephone order, transactions, transmit, travel, virtual terminal