May 22nd, 2017 by Elma Jane

Discount Rate: Qualified Mid or Non-Qualified Transactions

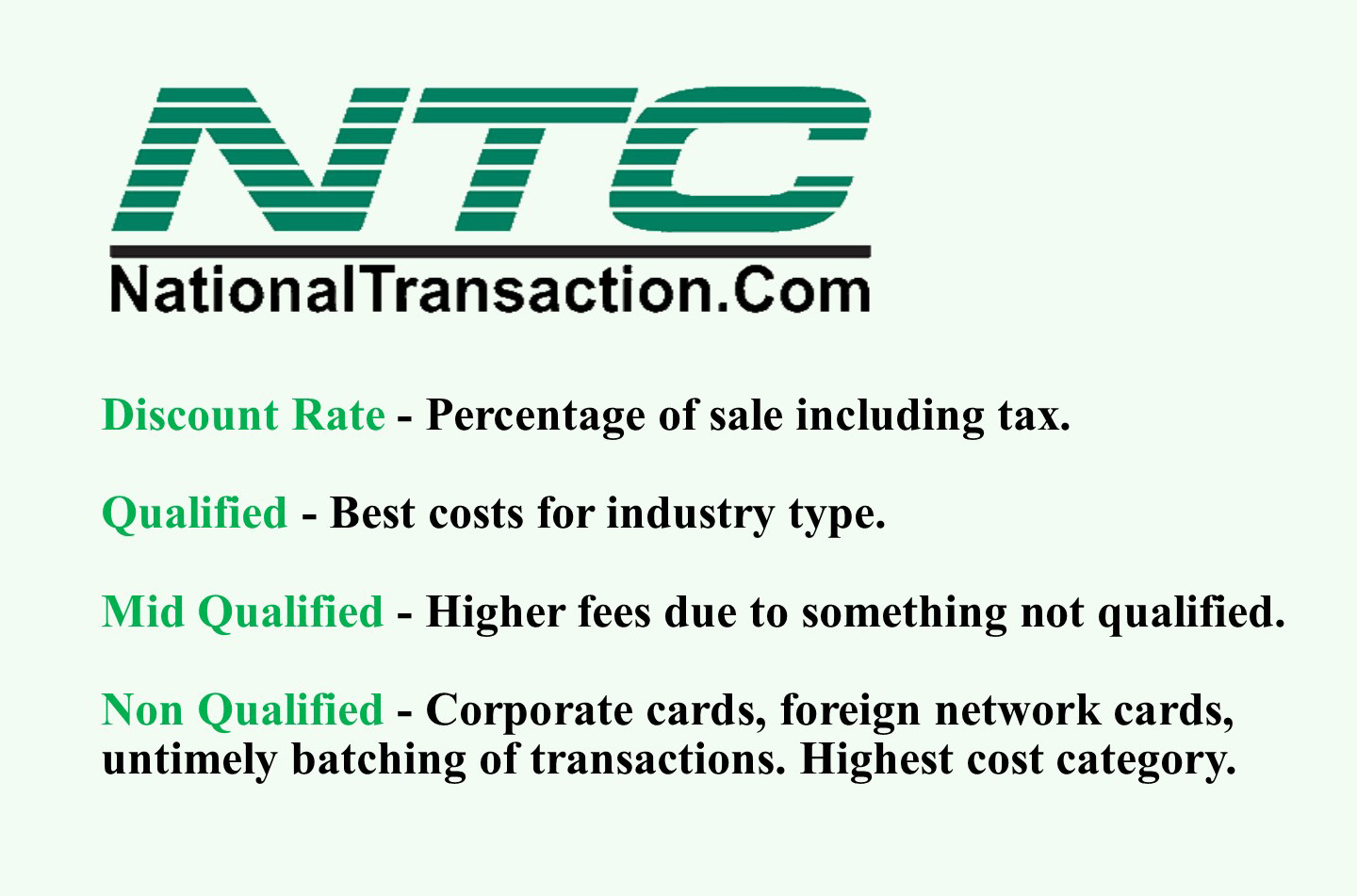

Discount Rate – is a percentage of the total sales submitted to the Bank for processing.

Qualified Transactions – are those in which an authorization was obtained electronically, the transaction was settled within the appropriate time frame, and the transaction meets all other requirements imposed by the bank. With qualified transactions you can get the lowest possible discount rate which is the Qualified Rates. The processor determines what transactions are qualified.

Mid-Qualified Transactions – include but are not limited to those transactions where the card is affiliated with a special issuer program or did not meet requirements imposed by the bank processor.

Non-Qualified Transactions – include but are not limited to those transactions where the authorization was obtained by calling a voice or Voice Recognition Unit (VRU) authorization number, the card is affiliated with a special issuer program, the transaction was not settled in the appropriate time frame, or the transaction did not meet the requirements imposed by the bank.

Mid or Non-Qualified transactions may be subject to increased fees and or Discount Rate as determined by the Bank.

If you are a mail order telephone order or e-commerce Merchant, the bank card brands/organizations require additional data elements to be submitted as part of the transaction record in order for the transactions to qualify for the lowest possible discount rate.

For Electronic Payment Set up call now 888-996-2273 or click here NationalTransaction.Com

Posted in Best Practices for Merchants Tagged with: bank, data, e-commerce, electronic payment, merchant, processor, transaction

May 11th, 2017 by Elma Jane

Three Domain Secure (3-D Secure)

Visa is announcing a global plan to support 3-D Secure 2.0 to help protect e-commerce transactions.

3-D Secure (3DS) – stands for Three-Domain Secure. A messaging protocol to enable consumers to authenticate themselves with their card issuer when making card-not-present (CNP) e-commerce purchases. 3DS is an additional security layer that will help prevent unauthorized CNP transactions and protects the merchant from CNP exposure to fraud.

The three domains consist of:

The merchant/acquirer domain

Issuer domain

the interoperability domain (payment systems)

The purpose of the 3DS protocol within the payments community is to facilitate the exchange of data between the merchant, cardholder and card issuer. The objective is to benefit each of these parties by providing the ability to authenticate cardholders during a CNP e-commerce purchase, reducing fraud.

Visa currently offers its 3-D Secure service through the Verified by Visa program, which supports the existing 3-D Secure 1.0 specifications for consumer authentication.

Visa anticipates that early adoption of 3-D Secure 2.0 will begin in the second half of 2017.

Merchants that authenticate transactions using 3-D Secure are generally protected from issuer card-not-present fraud-related chargeback claims,1 and this rule will extend to merchant-attempted 3-D Secure 2.0 transactions after 12 April 2019, the global program activation date.

For Electronic Payment Set Up go to NationalTransaction.Com or call now 888-996-2273!

Posted in Best Practices for Merchants Tagged with: card, card-not-present, cnp, data, e-commerce, electronic payment, merchant, payment, Security, transactions

May 1st, 2017 by Elma Jane

3D Secure Authentication

One of the biggest frustration for e-Commerce businesses has been the risk of chargebacks. If a shopper were to tell their issuers that they did not authorize an Internet purchase with their credit card, the merchant can lose the chargeback and the product.

By using 3D Secure capabilities, merchants get detailed evidence of authorized purchases “authentication data”.

The authentication data, together with an authorization approval gives you a transaction that is guaranteed against the most common types of chargebacks: Cardholder not authorized and cardholder not recognized chargebacks.

3D Secure is a security tool that enables cardholders to authenticate their identity to their card issuer through the use of Visa’s Verified by Visa and MasterCard’s SecureCode services.

3D Secure adds another layer of security to cardholders by preventing fraudulent purchases in an e-Commerce environment and reducing the number of unauthorized transactions.

NTC’s Virtual Merchant users processing transactions in an integrated e-Commerce environment are able to take advantage of this functionality.

3D Secure processing is supported with MasterCard and Visa transactions only. Other card types will process as normal and will not trigger 3D secure processing.

For e-Commerce Electronic Payments set up with 3D Secure

call now 888-996-2273! or click here NationalTransaction.Com

Posted in Best Practices for Merchants, Credit Card Security, e-commerce & m-commerce, Electronic Payments, Visa MasterCard American Express Tagged with: chargebacks, credit card, data, e-commerce, electronic payments, MasterCard, merchant, Security, transaction, visa

April 27th, 2017 by Elma Jane

Adding Tokenization Service

Important notes when adding tokenization:

– Tokens replace credit or gift card numbers.

– The terminal must be enabled to accept tokenization.

– Tokens are unique for each merchant, for example:

The same card will produce a different token for each merchant.

– Merchants with multiple terminals sharing tokenization domains will receive the same token for a unique card and the token can be used across their stores if they wish to do so.

– Merchants may supply the token in place of card information in any subsequent transaction.

– Tokenization is supported for both credit cards and gift cards.

Tokenization protects card data when it’s in use and at rest. It converts or replaces cardholder data with a unique token ID to be used for subsequent transactions. This eliminates the possibility of having card data stolen because it no longer exists within your environment.

Tokens can be used in card not present environments such as e-commerce or mail order/telephone order (MOTO), or in conjunction with encryption in card present environments.

Tokens can reside on your POS/PMS or within your e-commerce infrastructure “at rest” and can be used to make adjustments, add new charges, make reservations, perform recurring transactions, or perform other transactions “in use”.

For Electronic Payment Set up with Tokenization call now 888-996-2273

or click here NationalTransaction.Com

Posted in Best Practices for Merchants Tagged with: card present, card-not-present, credit, e-commerce, electronic payment, encryption, gift Card, merchant, moto, POS, terminals, tokenization, tokens, transaction

April 5th, 2017 by Elma Jane

Fighting chargebacks is important to a business. Whether you process transactions at a point of sale location or operate an e-Commerce business making sure you have implemented a process to dispute your chargebacks is critical.

Basic concepts that can be used to begin learning how to dispute chargebacks:

Keep accurate records of data that is easily accessible. Keeping track of your sales and products have a much easier time in collecting the information necessary to combat a chargeback.

Act quickly, don’t wait! You only have 10 days to respond to a chargeback or retrieval request. If you do not respond in 10 days you lose to a chargeback, and It gets worse; as you will not be able to re-present your case.

Compile and submit the documents to your processor. Make sure the documents have the original chargeback documents attached as well as the other supporting documents.

Follow up to make sure they have been received. Your processor may have an online system that allows you to submit documents directly into the processor chargeback system and some even allow you to view submitted documents in REAL TIME.

Monitor your chargebacks, this will help you understand what processes work for each specific chargeback type.

KEEP YOUR CUSTOMERS HAPPY

NationalTransaction.com 888-996-2273

Posted in Best Practices for Merchants Tagged with: chargebacks, data, e-commerce, point of sale, processor, transactions

January 31st, 2017 by Elma Jane

Selecting a Payment Provider

Selecting electronic payments provider for your business is critical. NTC believes that the process starts with an honest assessment of your business and the types of credit card processing options it requires. (Retail or e-commerce, Card Present or Card-Not-Present)

Card present transaction is the most common type of account. Card-Not-Present (CNP) is a different type of account if you run a MOTO (mail order telephone order) or Internet operation.

Here are some points to keep in mind in selecting your electronic payments provider:

Referrals from fellow business owners and checking out payment providers online.

Evaluate products and services as well as cost to determine which electronic payments provider offers the biggest savings for your business.

Make sure the deals you’re considering include all the features and services you need and none that you won’t use.

Keep upgrade options in mind.

Look for 24/365 support and discuss customer service support.

Read the fine print in your contract.

The merchant account provider’s reputation is important, so find out how long they’ve been in business and their reputation in the industry.

NTC has over 20 years’ of Bankcard History. Helping businesses of all sizes for over 25 years in the industry. Call us now 888-996-2273 and tell us all about your business needs and requirements and we’ll put together a package of products and services that will best serve your credit card processing needs. There are a variety of solutions, so it’s important to focus in on those that directly address your needs.

Posted in Best Practices for Merchants Tagged with: cnp, credit card, customer, e-commerce, electronic payments, internet, merchant account, online, payment provider, payments, retail, transaction

January 24th, 2017 by Elma Jane

How to set up a travel merchant account?

First, you need to find a Merchant Service Provider.

Put together your business profile so you can start applying for a merchant account.

There are questions that you’ll need to answer, that way merchant account providers have an idea of how they should set up your account.

Some of the questions are:

Is your business seasonal?

For Travel Agencies or Tour Operators, it is seasonal, there will be high and low volume. NTC works with seasonal downtime.

How do you intend to accept payments?

Different business models require different methods of accepting payments.

If you’re doing face to face transaction and have a physical location then you need a credit card terminal.

If you process checks, then you need Electronic Check and ACH Transfers.

For e-Commerce shopping carts, wireless/mobile, you can check out our Converge Virtual Merchant and NTC e-Pay.

How much volume do you plan on processing?

Merchant account providers are going to want to know how much sales volume you plan on processing per month.

If you’re new in the business – give just an estimate average of how much you’ll be processing (per month), within the first 6-months of operation.

if you’ve been in the business – you’ll already have this number ready.

What will be your average ticket price?

Example:

Total Sales Revenue = $150,000

Total Number of Sales = 500 150,000/500 = $300 (Average Ticket Price)

If you need to setup an account give us a call at 888-996-2273 or use our contact form.

Posted in Best Practices for Merchants Tagged with: ach, credit card, e-commerce, E-Pay, Electronic Check, merchant account, merchant service provider, mobile, payments, shopping carts, terminal, transaction, travel, virtual merchant

January 12th, 2017 by Elma Jane

Accepting non-cash payments from your customers are valuable. If you don’t, you will miss out on sales; because of the growing numbers of customers who only carry plastic or wish to pay online. Today, you have many payment solution options.

Credit Card Terminals – you might remember the beginning of the credit card era and i’ts evolution with today’s countertop terminals. From the traditional swipe of their credit, debit or even gift card to make a purchase to today’s modern terminals. Like accepting EMV chip cards (to be in compliance with a PCI mandate) and NFC payments like Apple Pay.

Beyond the basics; these systems are generally supported by reporting sites that can help you monitor sales, and assist you with maintaining customer loyalty programs.

E-Commerce Solutions – online sales are growing every year. If you are considering an expansion of your business online; you need a complete hosted payment solution for transactions in all payment environments. Including in-store, back office mail/telephone order (MO/TO), mobile and e-commerce, that make your customers’ experience as intuitive and efficient as possible.

Point of Sale Systems – smart registers have evolved into high-tech point-of-sale (POS) systems due to technology advances. Not only taking customer payments; but it can transform your business with an advanced marketing programs, inventory management and sales and profitability tracking and reporting. Over the past years these advanced systems have become cost-effective and easy to use.

Wireless Terminals – in today’s hardware you have the option of accepting payments wirelessly, through a full-service terminal that is smaller than a countertop model, or through a mobile card reader plugin for a smartphone or tablet.

The advantage of a full-service wireless terminal is that it allows for receipt printing on the spot through the device and most modern full-service wireless terminals are EMV compliant and accept both EMV (chip card) and NFC payment types.

Call now 888-996-2273 and speak to our payment consultant to know which solution is best for you.

Posted in Best Practices for Merchants, Credit Card Reader Terminal, e-commerce & m-commerce, EMV EuroPay MasterCard Visa, Mail Order Telephone Order, Near Field Communication, Payment Card Industry PCI Security, Point of Sale Tagged with: card reader, chip cards, credit card, debit, e-commerce, EMV, gift Card, mobile, moto, nfc, online, payment solution, payments, PCI, point of sale, smartphone, terminals, transactions

January 6th, 2017 by Elma Jane

Online fraud is not going away; hackers are becoming more sophisticated. While technology offer more avenues for consumers to pay, they also offer new ways for hackers to steal data.

There are several factors that increases the growth of online fraud:

EMV migration: because of EMV migration, fraud in face to face transactions becomes more difficult and moves to card-not-present transaction. This has been observed after EMV is implemented in other country.

Banking activity: it is moving online not only via online-only banks, but also mobile and online bank services.

An increase of online marketplaces: financial services pros are more proficient in identifying fraud compare to individual consumers who become sellers that can be victims of online fraud.

How can e-commerce and financial services companies reduce online fraud?

Merchants: Ensure that you have payment security. Fraudsters use sophisticated technologies, ask your payment provider for encryption and tokenization. You can also use BIN LookUp as an added security and number of benefits. Bin LookUp allows merchant or institution to check more about the transaction.

Online marketplaces: Marketplaces can protect their reputation by validating new sellers using sophisticated device and applying advanced models and machine learning to detect unusual patterns of activity that indicate misuse.

Banks: Fraudsters continue to innovate. Bank technology needs to be flexible and stay one step ahead.

For account set up or terminal upgrade call now 888-996-2273 or visit www.nationaltransaction.com

Posted in Best Practices for Merchants, e-commerce & m-commerce, EMV EuroPay MasterCard Visa, Mobile Payments, Mobile Point of Sale Tagged with: banks, card-not-present, data, e-commerce, EMV, encryption, financial services, fraud, merchants, online, payment, provider, Security, terminal, tokenization, transactions

November 22nd, 2016 by Elma Jane

Be with NTC and enjoy the full benefits of our Electronic Payment Services with high levels of service and security.

Be with NTC and enjoy the full benefits of our Electronic Payment Services with high levels of service and security.

In addition, you can enjoy from e-commerce payment gateways to retail and restaurant solutions, business-to-business processing capabilities to electronic invoicing (NTC ePay).

NTC is offering a cost-effective credit card payment processing services that are very fast, secure and easy to integrate.

Get your Secure MerchantConnect Reporting Tool:

Get your Secure MerchantConnect Reporting Tool:

- Review and reconcile all of your transactions settle or batch settle and also much more.

- Create and save your custom reports that also can be imported or exported easily.

- Use our solution to turn any computer, laptop, smartphone or tablet into a processing center.

- Run & enjoy this on one or more devices to process credit card transactions with your merchant account.

- Peripherals allow swiping transactions and printing out receipts.

Our Merchant Cash Advance feature will help you very much to enjoy cash advance service. If your business accepts credit cards, getting cash for your business can be fast, simple and very easy.

Our Merchant Cash Advance feature will help you very much to enjoy cash advance service. If your business accepts credit cards, getting cash for your business can be fast, simple and very easy.

Receive up to $150,000 per location in less than 10 business days—sometimes in as few as 72 hours.

National Transaction Merchant Cash Advance eliminates many hassles and delays common with bank loans.

Our Merchant Cash Advance builds on the strength of your business’ future credit and debit card sales, so a damaged personal credit history is not an immediate disqualifier.

Posted in Best Practices for Merchants Tagged with: bank, cash advance, credit card, debit card, e-commerce, Electronic invoicing, electronic payment, gateways, loans, merchant account, payment, payment services, Security, smartphone, transactions