November 19th, 2015 by Elma Jane

The Ingenico iCMP PIN pad is now available with Converge in the US! This EMV-enabled device is flexible to use with a USB connection and Converge or with a Bluetooth connection and Converge Mobile (launching soon!).

Key features of the Ingenico iCMP include:

Chip, Contactless and Mag Stripe

Accept EMV chip cards, including Chip & Pin and Chip & Signature as well as mag stripe cards and contactless payments – mobile wallets like Apple Pay and contactless cards. The EMV-capabilities of the PIN pad help protect our customers from counterfeit card fraud.

Debit and Credit PIN Based Transactions

Accept debit and credit cards using PIN capabilities on the device. This is important to help further protect our customers from lost, stolen and NRI (not received/issued) fraud.

Encryption

Encrypted to keep card data separate and away from the mobile app/device and safe as it travels through the payment network.

Bluetooth or USB

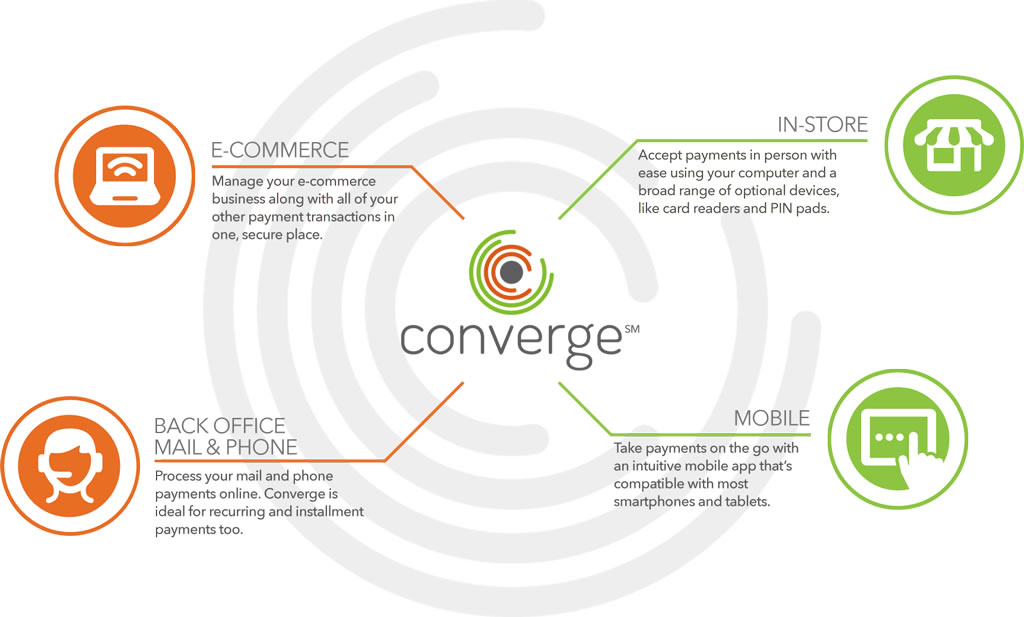

Connect with a USB connection when using a computer and Converge www.convergepay.com or Bluetooth when using with the upcoming Converge Mobile app.

Pocket size

Takes up little space on a countertop, and it’s easy to carry when on the go.

Give us a call now at 888-996-2273.

Posted in Best Practices for Merchants Tagged with: Apple Pay, card data, Chip & PIN, Chip & Signature, chip cards, contactless cards, contactless payments, Converge, Converge Mobile, credit cards, Debit and Credit, EMV, encryption, ingenico, mag stripe, mobile wallets, payment network, transactions

October 16th, 2015 by Elma Jane

U.S. customers with the Ingenico iSC250 may now process EMV chip card transactions for Visa, MasterCard, American Express and Discover, (as well as mag stripe and contactless, including mobile wallet payments). For customers using the Ingenico iSC250, please make sure you have downloaded the latest version of ConvergeConnect and enabled EMV chip cards in Converge. Go to the Converge login page to download the software update or start the update process from their Windows system tray. If you do not have the Ingenico iSC250 but want to upgrade to process chip card transactions, give us a call at 888-996-2273 for more information.

Posted in Best Practices for Merchants, EMV EuroPay MasterCard Visa Tagged with: chip card, EMV, mag stripe

January 21st, 2015 by Elma Jane

With a crucial deadline, the payments industry is starting to look at just what kind of fraud liability and how much fraud merchant acquirers will have to assume if their merchants aren’t ready to accept Europay-MasterCard-Visa (EMV) chip cards by October.

While issuers currently absorb losses under card-network rules, that burden will shift to acquirers this fall in cases where the fraud occurs at merchants unprepared for EMV.

As a result, acquirers will have to reckon with a whole new category of risk exposure.

In card-not-present transactions, acquirers have faced this, but in the overwhelming majority of cases they’ll be confronting it for the first time.

Surprisingly, for all the talk in the industry about the imminent arrival of EMV, it appears few acquiring executives have fully accounted for what the shift really means for them.

Some 24% of U.S. point-of-sale terminals are “EMV-capable,” while 9% of debit/prepaid cards issued, and 2% of credit cards have EMV chips so far. But while terminals may be technically capable, it isn’t known just how many of these merchants have the software and trained personnel to accept EMV.

Foreign issuers, especially, may be licking their chops at the prospect of offloading their consumer-fraud risk onto U.S. acquirers. For years and years, these non-U.S. issuers have invested in EMV, but the U.S. is still using the mag stripe. So non-U.S. issuers appear to be very aware of the liability shift.

To be sure, acquirers’ increased risk exposure may be relatively short-lived. Under the network rules, liability rests with the issuer in cases where both the merchant and the issuer are EMV-compliant. That could be nearly universally the case within a few years. By 2018, nearly all cards and terminals will be compliant.

But that still leaves open the question of how many of these terminals will really be running chip card transactions.

The issue isn’t so much about terminals as about software. Many mid-size merchants are using so-called integrated solutions that run payments as part of a larger business-management system. That means acquirers must work with a number of other parties to reconfigure software, and that presents a challenge when it comes to getting masses of merchants EMV-compliant.

The bigger problem is the integrated point-of-sale market.

While the liability shift may impact acquirers, not all them are convinced their exposure will rise all that much. Some argue the risk of loss from lost/stolen/counterfeit cards at the point of sale is low and not likely to rise, especially for small-ticket merchants.

Fraudsters, are much more inclined to practice their trade online, where the risk of being caught is lower, compared to face-to-face transactions.

Posted in Best Practices for Merchants, Credit card Processing, Credit Card Reader Terminal, Credit Card Security, EMV EuroPay MasterCard Visa, Visa MasterCard American Express Tagged with: card network, card-not-present, chip cards, credit cards, debit/prepaid cards, EMV, EuroPay, fraud, integrated solutions, mag stripe, MasterCard, merchant acquirers, Merchant's, payments, payments industry, point of sale, terminals, transactions, visa