Category: Electronic Payments

September 22nd, 2015 by Elma Jane

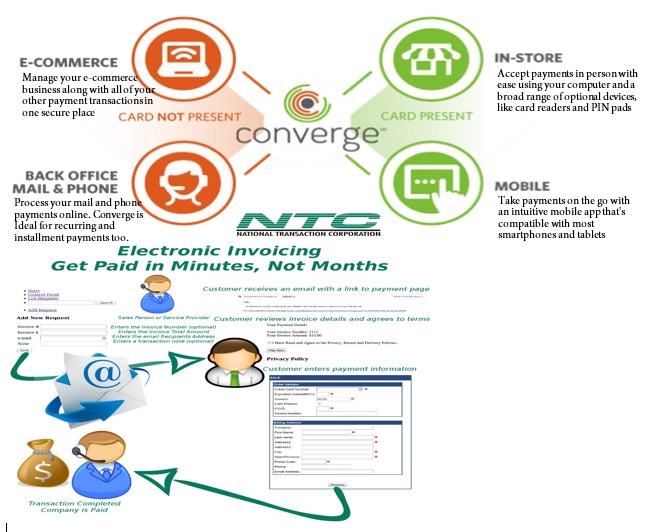

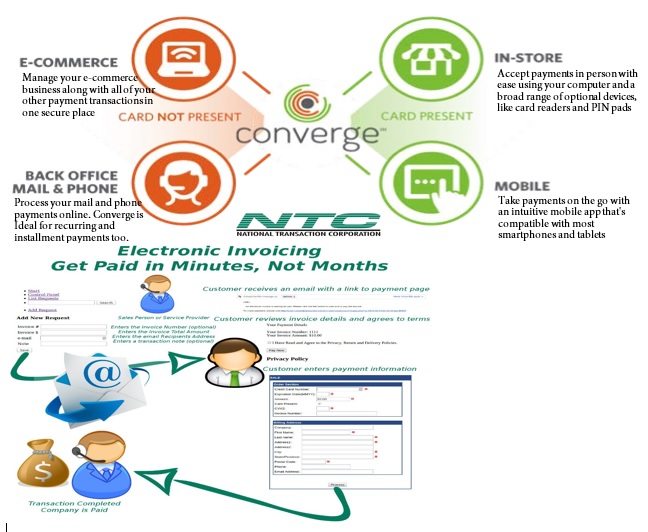

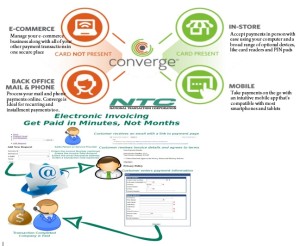

Virtual Merchant/Virtual Merchant Mobile now called Converge, is a popular product offering solutions for retail stores, Non Face to Face businesses along with E-commerce/Internet sites. Converege can be access anywhere with internet. Users can download the application on their smartphone or tablet. Converge also gives users the convenience of sending an invoice to customers electronically with NTC e-Pay!

For Retail store National Transaction offers the latest in EMV and NFC technologies. NTC customers can accept contactless payment with the same NFC technology used by Apple Pay, Google Wallet and SoftCard. NTC offers different solutions that cater to your business needs. For those already using a POS system, NTC integrates with most systems. NTC has you covered.

Posted in Best Practices for Merchants, e-commerce & m-commerce, Electronic Payments, Mobile Payments, Mobile Point of Sale Tagged with: Apple Pay, contactless payment, Converge, e-commerce, EMV, Google Wallet, nfc, POS system, smartphone, tablet, virtual merchant

January 26th, 2015 by Elma Jane

Accept Electronic Payments in Their Currency,

Convert it to Yours

DCC or Dynamic Currency Conversion is a system where the Visa or MasterCard holder in a foreign country can shop on an American based web site that displays prices in their own local currency. The web site can offer multiple choices as to which country the shopper is based in and the shopper can be immediately familiar with the pricing of goods and services.

Exchange rates are in constant flux. Dynamic Currency Conversion utilizes a Bank Reference Table (BRT) otherwise known as a Card Recognition Table (CRT). This table is updated on a daily basis so that transactions have the most up to date conversion rate for transactions. Your web site holds pricing information in $USD, and based on the selection of the shopper, prices are converted to their native currency. Even if the shopper does not choose the correct currency, at the time the card information is presented, the system automatically recognizes that the card is foreign and applies the appropriate currency and exchange rate.

At the close of the transaction an invoice or receipt can present the total to the customer in their currency, along with the merchants local currency along with the exchange rate that was applied. In today’s global business environment, this level of convenience to the customer insures they are comfortable with the transaction from shopping cart to the door. Your business reaches foreign nations expanding your market while presenting new opportunities, increasing your businesses bottom line.

On the merchant end, all transactions are settled in $USD. Reporting mechanisms can display the consumers pricing and the exchange rate they paid for analysis and cost reduction.

Currency Conversion

- Accept currencies from other nations.

- Convert funds to US Dollars.

- Set prices in local currency to avoid confusion or calculation.

- Works with e-commerce as well as Mail Order / Phone Order.

- Ease the sales process for your customers.

- Increase customer familiarity.

- Immediately convert currency to avoid value gaps.

Posted in Best Practices for Merchants, Electronic Payments Tagged with: Bank Reference Table, Card Recognition Table, consumer, conversion rate, currency, customer, Dynamic Currency Conversion, e-commerce, electronic payments, exchange rate, invoice, MasterCard, Merchant's, receipt, shopping cart, transactions, visa

May 6th, 2014 by Elma Jane

Boston-based Loop has released its LoopWallet app for storing magnetic-stripe cards on smartphones and using them in contactless payments at regular POS terminals.

Loop is a Level One PCI certified payment provider. Its technology has applications for turning loyalty cards into contactless cards and can also be used to generate dynamic card data every time a payment is made, preventing the creation of cloned cards.

The Loop Fob contains a microprocessor and magnetic induction loop and can be used without a phone, in which case payment would be taken from a designated card.

Mag-stripe cards for payment, gift, loyalty, ID or membership are read by the Loop Fob, a small audio jack magnetic-stripe reader, and then card data is encrypted and stored on the user’s smartphone. The LoopWallet app allows users to view their cards and select the one they wish to use.

To make a payment at the point of sale, the phone sends a signal, using Loop’s Magnetic Secure Transmission technology. MST emulates the signal generated when a mag-stripe card is swiped across a POS terminal’s read head. The signal is received by any mag-stripe card reader without requiring modifications to the POS terminal or processing system.

The free LoopWallet App for iOS 7 is available in the Apple App Store, with an Android version planned for release in April 2014. The app is only available to U.S. consumers.

.

Posted in Best Practices for Merchants, Credit card Processing, Digital Wallet Privacy, Electronic Payments, EMV EuroPay MasterCard Visa Tagged with: contactless, mag-stripe readers, magnetic stripe, mobile wallet, PCI

May 5th, 2014 by Elma Jane

The Payment Card Industry (PCI) Data Security Standard (DSS) has come under criticism as high profile data breaches continue to expose flaws in retailers’ data security systems. But telecommunications firm Verizon Wireless concluded that the PCI DSS is working.

Some Responses to Criticisms

Nilson Report research from August 2013 that said card fraud cost the global payments market over $11 billion in 2012. Verizon added that the frequency of fraud schemes that the PCI DSS was designed to avoid is in fact growing. And yet most businesses are not fully compliant at the time of assessment. Only 51.1 percent of the companies it had audited had passed seven of the 12 requirements of the PCI DSS and only 11.1 percent of said companies had passed all 12.

Verizon addressed some of the criticisms leveled at the PCI DSS. One concern is that the standard promotes compliance as a test to be passed and forgotten, which distracts companies from focusing on improving security. Verizon responded by stating that breached businesses were less likely to be PCI DSS compliant than unaffected companies. It also said businesses improve their chances of not being breached by having the standard in place, and of minimizing the damage of a breach should one occur.

Another common complaint leveled at the standard is that it is too cumbersome and slow moving in relation to the quickly evolving threat landscape and nimble fraudsters ready to try new tactics. Verizon countered that the PCI DSS is meant to be a set of baseline security protocols. Achieving compliance with any standard is simply not enough, organizations must take responsibility for protecting both their reputation and their customers. Most attacks on networks are of the simple variety, with 78 percent of hacking techniques considered low or very low in sophistication. Data Breach Investigations Report (DBIR) research shows that while perpetrators are upping the ante, trying new techniques and leveraging far greater resources, less than 1 percent of the breaches use tactics rated as high on the VERIS (Verizon’s Data breach Analysis Database) difficulty scale for initial compromise.

Recommendations

There’s an initial dip in compliance whenever a major update to the standard is released, so organizations will have to put in additional effort to prepare for achieving compliance with DSS 3.0.

The newest version of the standard, PCI DSS 3.0, went into effect Jan. 1, 2014. Businesses have until Jan. 1, 2015, to implement it. The updated standard has new requirements and clarifications to version 2.0 that will take time for businesses to understand and implement, and this will result in more organizations being out of compliance.

To help businesses deal with their PCI DSS compliance obligations the firm offered five approaches:

Don’t leave compliance to information technology security teams, but enlist application developers, system administrators, executives and other staff in helping further along the process.

Embed compliance in everyday business practices so that it is sustainable.

Integrate compliance programs into enterprise-wide governance, risk and compliance strategies.

Learn how to reduce the scope of organizations’ compliance responsibilities, chiefly by figuring out how to store less data on fewer systems.

Think of compliance as an opportunity to improve overall business processes, rather than as a burden.

Posted in Best Practices for Merchants, Credit card Processing, Credit Card Security, Electronic Payments, Payment Card Industry PCI Security, Visa MasterCard American Express Tagged with: attacks on networks, Breach, breached, business processes, compliance, compliant, data breach investigators, data breaches, data security systems, database, DSS, fraud schemes, global payments, hacking, information technology, Payment Card Industry, PCI, retailers, Security, security protocols, standard, system administrators, wireless

April 18th, 2014 by Elma Jane

Capital One joins existing stakeholders equally owned by Bank of America, JPMorgan Chase, and Wells Fargo. Member-owner of the ClearXchange network.

Capital One has taken a stake in ClearXchange, the US bank-backed clearing house for person-to-person online payments transfer.

ClearXchange is the first network in the U.S. created by banks that lets customers send and receive (P2P) person-to-person payments easily and securely using an email address or mobile number.

With only the recipient’s mobile number or email address, the ClearXchange network enables customers to send funds directly from their bank account to the recipient’s bank account without the need to pass on more sensitive account information.

EVP of digital at Capital One, says partnering with clearXchange is another way of bringing safe and secure payments through convenient, digital channels to their customers.

With membership open to banks and credit unions of all sizes, ClearXchange has so far signed up only FirstBank as its sole non-owner participant, although it nonetheless claims to represent more than 50 percent of the consumer online banking market.

Posted in Credit card Processing, Electronic Payments, Merchant Services Account, Mobile Payments, Payment Card Industry PCI Security, Small Business Improvement, Smartphone, Visa MasterCard American Express Tagged with: account, bank account, Bank of America, Capital One, consumer online banking, digital channels, JP Morgan, market, mobile, online payments transfer, p2p, payments, person-to-person, secure payments, securely, U.S. Bank, US Bank, Wells Fargo

April 15th, 2014 by Elma Jane

Amsterdam, Netherlands-based Cardis has been piloting its technology in Europe with Raiffeisen Bank in Austria and Sberbank in Russia. They are now focused on the U.S., as this is the fastest growing mobile payments market in the world, where there’s a huge opportunity. Integration of technology with a large U.S. processor and with a major U.S. retail brand, which will be launching a mobile site and mobile app using Cardis solution.

Cardis International is planning an April launch in the U.S. for its technology, which enables merchants to accept low-value contactless or mobile payments without incurring high processing charges. Cardis is able to bring down the processing cost of low-value payments, the company said, by aggregating multiple transactions into a single payment.

The problem

Contactless card and NFC-based mobile payments are typically for low amounts, and yet still use a card processing infrastructure that was designed 40 years ago when the average credit card transaction was $100.

Traditional card processing systems require each transaction to be individually processed through the payment system, including authorization, clearing and settlement. The resulting variable costs of processing each transaction are independent of the transaction amount and too high for low-value payments, particularly in low-margin industries such as quick-service restaurants. QSR restaurants often have a 3 percent profit margin, yet, for low-value contactless payments, the processing cost could be as high as 6-7 percent of the transaction value.

Mobile and contactless cards offer consumers a convenient form factor. But they don’t solve the problem that low-value card payments are very expensive for merchants.

As an ever-increasing percentage of transactions have become cashless, card processing fees have become a significant cost. Costs that are based on the number of transactions, rather than their value. With average per person expenditures of $5 or under, feels each swipe fee much more than a business where customers spend $50 or more. But not accepting credit/debit cards for low-value transactions isn’t an option as many of customers don’t carry cash anymore.

Aggregation

Cardis’ solution is to act as an aggregator of low-value payments, sending a single batched transaction through to a processor instead of multiple low-value transactions. As there is no per transaction processing of individual low-value purchases, the cost-per-transaction is significantly reduced.

Cardis provides its technology as a software plug-in to payment service providers for contact-based and contactless card payments, mobile wallet transactions and NFC payments.

There are two models. For card payments, it will aggregate multiple purchases by an individual cardholder at a single merchant on a post-paid basis up to a specific amount, for example $20. To guarantee payment to the merchant, since the aggregated transaction is processed at a later date, it will pre-authorize an amount, for example $15, the first time the customer makes a purchase at that merchant.

Alternatively, merchants can opt for Cardis’ prepaid system. This involves the consumer setting up a prepaid account hosted by Cardis’ sponsoring bank that is topped up via ACH (automated clearing house) transfers. Using the Cardis prepaid account on a smartphone provides the digital equivalent to cash.

With its post-paid solution, merchants will save 30-50 percent per transaction compared to conventional card processing fees, while its prepaid solution saves merchants 80 percent per transaction. With the post-paid solution, it will only aggregate a customer’s purchases at a single specific merchant. But, as the prepaid solution aggregates the customer’s purchases across multiple merchants, this enables to offer a much lower processing fee to the merchant.

Cardis provides an audit trail enabling consumers to track individual transactions that are aggregated using its technology. Consumers don’t lose any of their card protection rights and guarantees by agreeing to let a merchant aggregate their payments through Cardis. They can always charge back any disputed transactions.

Cardis sees opportunities for digital content providers such as online music stores and games providers to use its aggregation technology. It can integrate solution with existing digital wallets.

Raiffeisen

In 2012, Austria’s Raiffeisen Bank launched a pilot of Cardis technology for NFC-based Visa V Pay debit card payments in partnership with Visa Europe. Raiffeisen’s MobileCard mobile payment product uses a secure element stored on an NFC-enabled MicroSD card inserted in a mobile phone. Although Cardis supports secure elements stored on SIM cards as well as on MicroSD cards and on the cloud, Raiffeisen opted for MicroSD cards, as this is an easier solution to implement.

Raiffeisen cardholders participating in the pilot use MobileCard on average three times a week, with an average transaction value of ($5.70). Merchants accepting MobileCard are seeing 40 percent to 70 percent lower merchant processing fees for an average transaction value of ($5.43) to ($13.60).

Spindle

In October 2013, Spindle, a U.S. mobile commerce company, signed an agreement with Multi-max, a manufacturer of vending machines for mid-size and small offices throughout North America, Europe and Asia. Spindle will integrate its MeNetwork mobile commerce technology into Multi-max’s line of K-Cup vending machines for rollout across the U.S.

The MeNetwork solution will incorporate all card-based payment acceptance services, as well as mobile marketing services. Spindle’s partner Cardis will provide low-value payment processing services for purchases at K-Cup vending machines.

Posted in Credit card Processing, Credit Card Security, Digital Wallet Privacy, e-commerce & m-commerce, Electronic Payments, Gift & Loyalty Card Processing, Internet Payment Gateway, Mobile Payments, Mobile Point of Sale, Near Field Communication, Payment Card Industry PCI Security, Smartphone, smartSD Cards, Visa MasterCard American Express Tagged with: accept, ach, aggregated, aggregation, aggregator, authorization, automated clearing house, average transaction, batched, card payments, card processing infrastructure, card processing systems, card-based payment acceptance, cardholders, clearing, contactless, contactless payments, cost-per-transaction, credit card transaction, debit card payments, Digital wallets, high processing charges, low-value payments, merchant aggregate, Merchant's, microSD, mobile app, mobile commerce, mobile payment, Mobile Payments, mobile site, mobile wallet transactions, nfc-based, payment service providers, pre-authorize, prepaid, processed, Processing, processing cost, processing fees, processor, settlement, smartphone, transactions, transfers

April 11th, 2014 by Elma Jane

Of the 17 percent of consumers who reported having had their credit card declined during a card-not-present (CNP) transactions. As many as one-third of those declines were unnecessary. The result is consumer aggravation, increased operational costs for banks and credit card companies and as much as $40 billion in lost revenue for online retailers.

TrustInsight which helps establish trusted relationships between financial institutions, merchants and online consumers conducted study. A report and infographic detailing the findings of the study found that avoidable online credit card declines lead to loss of trust for consumers, sales for merchants and increased operational costs for credit card companies and issuing banks.

Study also revealed that consumers handle credit card declines in a variety of ways all of which carried negative economic impact to at least one party in the transaction, resulting in unnecessary operating costs for banks, decreased loyalty for the credit card company and lost revenue for all. Almost half call their issuer immediately when their card is unexpectedly declined. This is a natural response. 34 percent of consumers try again another credit card, other use a different payment method and 24 percent will skip the purchase altogether or shop at a different online retailer.

No one wants to turn away business, and no one wants their business declined. The frustration and impact of wrongful declines is a real problem especially as more and more transactions occur in non-face-to-face situations.

Impact of consumer action in the face of a decline can have real and measurable effects on all parties, including credit card companies, banks and merchants manifesting itself in lost customer loyalty, lost fees and lost revenues. Creating a standard for online trust that enables credit card companies, merchants and issuing banks to better recognize trusted digital consumers and reduce the number of wrongly declined consumers avoiding unnecessary losses.

In a world where people are increasingly reliant on a variety of Internet-connected devices for everything from banking to shopping to entertainment and media, creating friction-free customer experiences and preventing online fraud are constant business challenges.

Posted in Best Practices for Merchants, Credit card Processing, Credit Card Security, Electronic Payments, Financial Services, Gift & Loyalty Card Processing, Merchant Services Account, Small Business Improvement, Visa MasterCard American Express Tagged with: banking, consumers, credit-card, decline, declined, declines, different payment method, digital, digital consumers, financial, frustrate, internet-connected devices, issuing banks, loyalty, Merchant's, online credit card declines, online fraud, online retailers, shopping, transactions, wrongful declines, wrongly declined

April 11th, 2014 by Elma Jane

A new standard that uses Host Card Emulation (HCE) was introduced by VISA to enable financial institutions to securely host Visa accounts in the cloud. Visa’s move to support HCE includes tools and services as well as the standard. It is available now and will include support for QR codes and in-app payments in the future.

With this new service and platform that Visa is developing, it will enable clients and partners to issue Visa accounts digitally in the cloud, on secure elements in smartphones, or linked to a digital wallet. The solution will also enable the issuance of payment tokens that will replace the 16-digit payment account number and can be limited for use with a specific device, merchant or payment channel.

Layers of security will deploy by Visa to protect payment accounts in the cloud, including at the Visa network, application and hardware levels. Device fingerprinting technology, one-time use data, payment tokens and real-time transaction analysis will make up a multi-layered defense against unauthorized account access for their services.

Visa has intensified its Visa PayWave contactless payment application and is introducing a new implementation guidelines, program approval process standard and requirements for their standards.

Visa is also developing a tool, its software development kit (SDK) to support clients who wish to develop their own cloud-based payment applications or want to enhance their existing mobile banking applications with Visa PayWave functionality.

HCE is introduced to make it easier for developers to create NFC applications like mobile payments, loyalty programs, transit passes, and other custom services. Visa’s move to enable NFC payments with Android devices is welcome news and will guide the way for the payments industry.

Clients and partners around the globe are continuously looking for cost efficient, flexible and secure ways to enable mobile payments. The Android HCE feature provides with a platform to evolve the Visa PayWave standard, support the development of secure, cloud-based mobile applications, while at the same time offer greater choice.

Posted in Best Practices for Merchants, Credit card Processing, Credit Card Security, Electronic Payments, Financial Services, Merchant Services Account, Mobile Payments, Mobile Point of Sale, Near Field Communication, Smartphone Tagged with: accounts, android devices, approval, cloud, cloud-based mobile applications, contactless payment, device fingerprinting, Digital Wallet, digitally, financial institutions, HCE, host card emulation, in-app, mobile banking, nfc, payment account number, payment channel, payment tokens, payments, qr codes, real-time transaction, secure elements, securely, Smartphones, unauthorized, visa, visa network

April 11th, 2014 by Elma Jane

PCI DSS 3.0 standard, which took effect January 1st, introduces changes that extend across all 12 requirements, aimed to improve security of payment card data and reducing fraud. There will be some shakeups for many organizations when it comes to their day-to-day culture and operations. Transitioning to meet the new requirements will help e-business build a stronger, safer, lower-risk environment for their customers.

While the growing number of digital payment avenues offers convenience to customers, it also offers a larger attack surface for criminals.

As cloud technologies and e-commerce environments continue to grow, creating multiple points of access to cardholder data and online retailers will only become more appealing targets for hackers. Cybercriminals are cunning and determined. They understand payment card infrastructures as well as the engineers who designed them.

A scary proposition and it’s exactly why the payment card industry is so determined to help keep e-commerce organizations protected. Meeting the new standard, businesses will be better armed to fight evolving threats. Changes will also drive more consistency among assessors, help business reduce risk of compromise and create more transparent provider-customer relationships.

Transitioning to PCI DSS 3.0 will involve some work, but doing that work on the front end is going to save much work down the line. Adopting the new standard ultimately will drive your e-commerce business into a secure and efficient era.

Cultural Changes – One of the main themes of 3.0 is shifting from an annual compliance approach to embedding security in daily processes. Threats don’t change just once a year. They’re constantly evolving and that means e-commerce organizations must adopt a culture of vigilance. Only through a proactive business-as-usual approach to security can you achieve true DSS compliance. Realistically, this could mean the need to provide more education and build awareness with staff, partners and providers, so that everyone understands why and how new processes are in place.

Operational Changes – The 3.0 standard addresses common vulnerabilities that probably will ring a bell with many of you. These include weak passwords and authentication procedures, as well as insufficient malware detection systems and vulnerability assessments, just to name a few. Depending on your current security controls program, this could mean you’ll need to step up in these areas by strengthening credential requirements, resolving self-detection challenges, testing and documenting your cardholder data environment and making other corrections.

Overview Changes – How much work lands on your plate will depend on your current security program. Examining your current security strategies and program is a good idea. Below are the areas requiring your attention, which this series will explore in more detail in future installments.

Service Provider Changes – Some organizations made unsafe assumptions in the past when it comes to third-party providers. Some have paid the price, from failed audits to breaches. One reason that the new standard is designed to eliminate any confusion over compliance responsibilities. Responsibilities, specifically for management, operations, security and reporting all will need to be spelled out in detailed contracts. In addition to improved communication, an intensified focus on transparency means that you should have a clear view of your provider’s infrastructure, data storage and security controls, along with subcontractors that can impact your environment. So if your organization isn’t exactly clear on which PCI DSS requirements you manage and which ones your providers handle, prepare to get all of that hammered out.

The Compliance Rewards – The path to preparing for the 3.0 deadline in January 2015 sounds like it’s a lot of work. So to get started request your QSA’s opinion on how the changes will impact your organization, by doing the gap assessment and you’ll be able to address any shortcomings.

Meeting the new 3.0 requirements isn’t just about passing audits. In fast paced payment IT landscape, staying smart and protected is part of our commitment to our customers. Beefing up security game not only reduce audit headaches, but also enjoy stronger brand reputation as a safe and reliable e-commerce business.

Posted in Best Practices for Merchants, Credit card Processing, Credit Card Security, e-commerce & m-commerce, Electronic Payments, Financial Services, Payment Card Industry PCI Security, Small Business Improvement, Visa MasterCard American Express Tagged with: 3.0, attack surface, authentication, breaches, businesses, cardholder data, complance, compliant, credential, cybercriminals, digital payment, DSS, e-business, e-commerce, embedding, hackers, lower-risk, online retailers, passing audits, payment card infrastructures, PCI, processes, reducing fraud, requirements, risk of compromise, security controls, security of payment card data, security program, standards

April 7th, 2014 by Elma Jane

Business-to-business ecommerce describes Internet-enabled transactions between businesses, such as a manufacturer and a wholesaler, a wholesaler and a retailers, or a wholesaler and a business user. The B-to-B ecommerce market was expected to exceed $550 billion in the U.S. last year, offering great opportunities for distributors and manufacturers to streamline sales, boost profits, and engage with new customers.

Since the late 1990s, businesses have been using the Electronic Data Interchange (EDI) system to transfer purchase orders and similar structured information electronically, representing, if you will, a form of B-to-B ecommerce.

Separately, some B-to-B sellers have created websites on which business customers can make purchases as if they were shopping on a business-to-consumer site. This category of B-to-B ecommerce may enjoy the most growth and offer the most opportunity.

Important points to consider of running a B-to-B ecommerce site.

B-to-B Customers Are also B-to-C Customers

B-to-B sites often trail consumer sites in technology, function, capabilities, and design. Typically not good enough.

As an example, the U.S. B-to-B site for a major multinational manufacturer, which includes information for dealers in the U.S., can only be viewed on Internet Explorer, and won’t work in any other browser, including Firefox, Chrome, Opera, or Safari. And don’t even think about visiting this site on a mobile device. It just won’t work.

This is a ridiculous business decision. It forgets a fundamental fact about B-to-B ecommerce customers. They are also B-to-C ecommerce customers.

It is extremely likely that the professional shopper on an ecommerce-enabled B-to-B website has had at least some experience shopping on consumer ecommerce sites, which all have compelling product photography, good navigation, good search capabilities, and good content.

A B-to-B ecommerce site must provide the same visual and functional experience as the best B-to-C ecommerce sites.

Personalization Is Vital

B-to-B shoppers may require a greater level of personalization than B-to-C customers, since businesses may have contract prices, special payment terms, or negotiated shipping rates.

Business relationships may be very deep and complicated. It is not unusual for B-to-B ecommerce sites to require registration before showing prices or shipping rates or offering a quote. This login requirement allows the B-to-B ecommerce site to personalize almost every aspect of the transaction.

A good B-to-B ecommerce site may take a little longer to launch since the system for handling relatively complex business relationships can take some time. But once it is in place, this personalization will mean that the relationship could be longer lasting.

Sales people Are the Primary Marketing Vehicle

While it is both possible and likely that B-to-B ecommerce sites will be able to acquire new customers simply by making products easy to order online, salespeople who contact customers are probably the B-to-B ecommerce seller’s primary and best marketing channel.

Salespeople can attract new customers or deepen relationships with existing shoppers. Sometimes, it can be enough to follow up after a B-to-B sale with a call to make certain that the transaction went as expected.

Shopping Is Part of Your Customer’s Profession

One of the most significant differences between B-to-B and B-to-C ecommerce is that shopping is part of the B-to-B ecommerce customer’s daytime job.

This means that the stakes can be higher for the B-to-B seller. If the shopper has a good experience, that shopper is likely to return and reorder repeatedly – even suggesting the seller to co-workers or other divisions. But if something goes wrong, particularly something that would cause the shopper to miss deadlines at work or appear in some way to have done a poor job, that shopper will likely blame the B-to-B seller. Depending on the unhappy shopper’s influence, the B-to-B seller might lose the entire account, including many individual buyers or divisions.

This means that order handling and transactional communications must be top notch. Some B-to-B ecommerce sellers will call customers to confirm orders or shipments when the customer has ordered a large quantity, very expensive items, or requested express shipping, since these orders may represent important transactions to the customer.

What Ecommerce Can Do for your B-to-B Business

If you sell to other businesses, ecommerce should have three potential benefits for your business.

First, it may help new customers find you. Having an easy-to-find and use ecommerce site means that new customers – customers with a need – will be able to locate your business regardless of geography or prior relationships.

Second, B-to-B ecommerce may streamline sales for existing customers. Some of your current customers will appreciate the ability to order online, 24 hours a day 7 days a week. The process may also be faster than sending emails or, even worse, faxed orders.

Finally, B-to-B ecommerce may improve margins and boost profits. It may be possible to provide customers with a better ordering experience and better customer service using ecommerce while spending less on labor and order processing. Any cost savings that B-to-B ecommerce brings may drop straight to your business’s bottom line.

Posted in Credit card Processing, e-commerce & m-commerce, Electronic Payments, Internet Payment Gateway, Mobile Payments, Mobile Point of Sale, Small Business Improvement Tagged with: account, b-to-b, b-to-c, better ordering experience, boost profits, business-to-business, business-to-consumer, business's bottom line, communication, consumer, cost savings, customer service, e-commerce, ecommerce, ecommerce sites, electronic data interchange, faxed orders, growth, improve margins, new customers, online, order handling, order processing, personalization, profits, purchase orders, salespeople, seller, sending emails, shopper, special payment terms, transaction, wholesaler