September 21st, 2016 by Elma Jane

PCI compliance applies to any company, organization or merchant of any size or transaction volume that either accepts, stores or transmits cardholder data.

Any merchant accepting payments directly from the customer via credit or debit card must be Compliant. The merchant themselves are therefore responsible for becoming Compliant, as the deadline for the merchant becomes overdue.

Understanding and knowing the details of Payment Card Industry Compliance can help you better prepare your business. Because failing and waiting to become compliant or ignoring them, could end up being an expensive mistake.

The VISA regulations have to adhere to the PCI standard forms as part of the operating regulations. The regulations signed when you open an account at the bank. The rules under which merchants are allowed to operate merchant accounts.

The Payment Card Industry Data Security Standard (PCI DSS) is a proprietary information security standard for organizations that handle branded credit cards from the major card schemes including Visa, MasterCard, American Express, Discover, and JCB.

Posted in Best Practices for Merchants, Credit Card Security, Payment Card Industry PCI Security, Visa MasterCard American Express Tagged with: American Express, cardholder, compliance, credit, customer, data, debit card, Discover, jcb, MasterCard, merchant, Payment Card Industry, payments, PCI, transaction, visa

February 2nd, 2016 by Elma Jane

Businesses continue to struggle with the prohibited storage of unencrypted customer payment data. The Payment Card Industry Data Security Standard (PCI DSS), merchants are instructed that, Protection methods are critical components of cardholder data protection in PCI DSS Requirement.

PCI DSS applies to every company that stores, processes or transmits cardholder information. Regardless of the size or type of business you operate, the number of credit card transactions you process annually or the method you use to do so, you must be PCI compliant.

Data breach is not a limited, one-time occurrence. This is why PCI compliance is required across all systems used by merchants.

Encryption and Tokenization is a strong combination to protect cardholder at all points in the transaction lifecycle; in use, in transit and at rest.

National Transaction’s security solutions provide layers of protection, when used in combination with EMV and PCI-DSS compliance.

Encryption is ideally suited for any businesses that processes card transactions in a face to face or card present environment. From the moment a payment card is swiped or inserted at a terminal featuring a hardware-based, tamper resistant security module, encryption protects the card data from fraudsters as it travels across various systems and networks until it is decrypted at secure data center.

Tokenization can be used in card not present environments (travel merchants) such as e-commerce or mail order/telephone order (MOTO), or in conjunction with encryption in card present environments. Tokens can reside on your POS/PMS or within your e-commerce infrastructure at rest and can be used to make adjustments, add new charges, make reservations, perform recurring transactions, or perform other transactions in use. Tokenization protects card data when it’s in use and at rest. It converts or replaces cardholder data with a unique token ID to be used for subsequent transactions.

The sooner businesses implement encryption and tokenization the sooner stored unencrypted data will become a thing of the past.

Posted in Best Practices for Merchants, Travel Agency Agents Tagged with: card, card data, card present, cardholder, compliance, credit card, customer, data, data breach, data security, e-commerce, EMV, encryption, Mail Order/Telephone Order, merchants, moto, payment, Payment Card Industry, PCI-DSS, POS, secure data, Security, terminal, tokenization, tokens, travel, travel merchants

June 19th, 2015 by Elma Jane

ASTA’s Regulatory Compliance Course

The Travel Agency Regulatory Compliance Course is an easy cost effective way to ensure your staff is up to speed on the latest federal regulations. Course cost: $225

ASTA members can save $200. Use code: ASTAfirst

Non-members can save $75. Use code: MustKnow

Sign-up Today! Click ASTA LOGO to Login.

Posted in Travel Agency Agents Tagged with: compliance, travel, travel agency

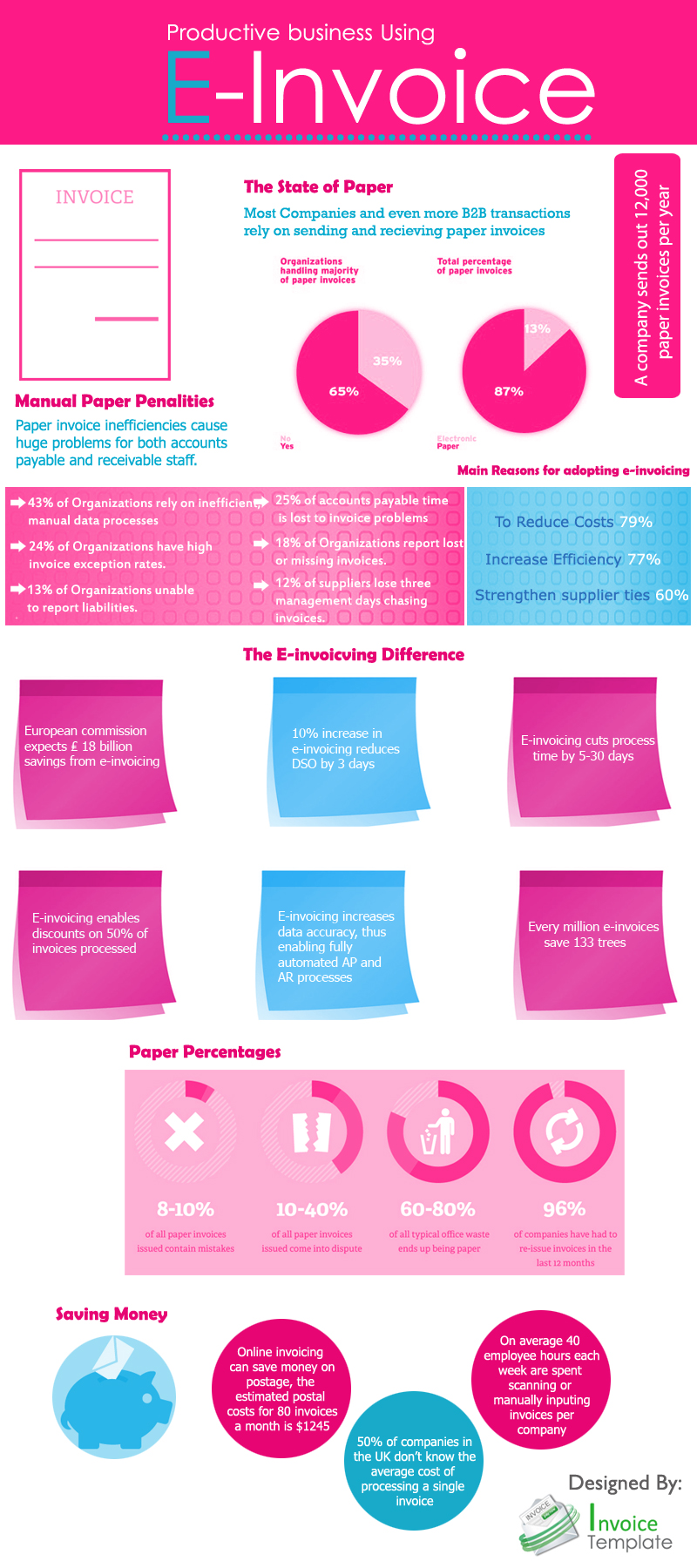

September 18th, 2014 by Elma Jane

Electronic invoicing is the exchange of the invoice document between a supplier and a buyer in an integrated electronic format. Traditionally, invoicing, like any heavily paper-based process, is manually intensive and is prone to human error resulting in increased costs and processing lifecycles for companies.

The issue of compliance seems to have separated E-Invoicing from B2B. Surprisingly many Finance leaders are unaware that their company is already sending/receiving EDI electronic invoices.

E-Invoicing is a common B2B practice and National Transaction is ready to launch its E-Invoicing system.

True definition of an electronic invoice is that it should contain data from the supplier in a format that can be entered integrated into the buyer’s Account Payable (AP) system without requiring any data input from the buyer’s AP administrator.

There are number of formats to be employed, it is useful to Apply below guidelines:

An E-Invoice:

1) Structured invoice data issued in Electronic Data Interchange (EDI) or XML formats.

2) Structured invoice data issued using standard Internet-based web forms.

Not a true E-Invoice:

1) Paper invoices sent via fax machines.

2) Scanned paper invoices.

3) Unstructured invoice data issued in PDF or Word formats.

Although significant cost and time savings can be achieved by removing paper and manual processing from your invoicing, the real benefits of E-Invoicing come with the level of security that comes with E-invoicing. Integration between your trading partners and your invoicing software and other business systems are optional. National Transaction can offer a customized Electronic Invoice Structure .

Posted in Best Practices for Merchants Tagged with: (AP), Account Payable, AP administrator, b2b, buyer, compliance, data, E-Invoice, E-Invoicing, E-Invoicing system, EDI, EDI electronic invoices, electronic data interchange, electronic format, electronic invoices, Electronic invoicing, Finance leaders, Internet-based web, invoice document, invoicing, National Transaction, Paper invoices, Security, supplier, web

June 24th, 2014 by Elma Jane

Compliance with a single set of regulations is often taxing enough, without other regulations causing a conflict, but this is exactly the situation that the insurance industry finds itself in with its contact centres.

PCI-DSS compliance insists that sensitive information in particular credit card numbers, must be protected and cannot be stored. However, the Financial Conduct Authority (FCA), the UK regulator for the financial services industry, demands that insurers keep sufficient detail of their transactions.

In insurance contact centres, FCA recommendations are met by recording calls. So in order to comply with PCI-DSS regulations, some contact centres simply pause recordings while the card information is read out, and resume recording once the payment process is complete. There’s a very big problem with this method, it undermines the very reason calls are recorded. The call recording is there to provide an unequivocal record of the circumstances under which the policy is granted. A gap in this record creates doubt. What was said during this time? If a customer is claiming a policy is mis-sold or they were misinformed in some way, a complete record to refute this claim no longer exists. Because of situations such as this, the insurance industry has an inherent dependence on contact centres and person-to-person interaction when selling policies, though in the process has to somehow comply with both regulations. But how? One way is to get the sensitive card information directly and securely to the bank’s payment gateway without storing it. Online, this is done quite easily, insurers can embed a secure payment page into a website and the customer can enter information securely that way. By phone a similar method can be used. A caller can input information directly on their telephone keypad and the tones are only transmitted to the credit card payment gateway not the contact centre. This solves the paradox of the conflicting regulations.

Insurance contact centres need to walk a very fine line, ensuring that they comply with all of the relevant regulations from multiple regulators – even those that, at first glance, contradict each other.

Posted in Best Practices for Merchants, Credit Card Security, Payment Card Industry PCI Security Tagged with: (FCA), card information, compliance, contact centres, credit card payment, credit-card, customer, Financial Conduct Authority, financial services industry, insurance industry, payment gateway, payment process, PCI-DSS, phone, regulations, secure payment, taxing, telephone keypad, transactions, website

May 8th, 2014 by Elma Jane

The complexity derives from PCI’s Data Security Standards (DSS), which include up to 13 requirements that specify the framework for a secure payment environment for companies that process, store or transmit credit card transactions.

Make PCI DSS Assessment Easier

Training and educating employees. Technical employees should obtain any certifications or training classes necessary so that they can operate and monitor the security control set in place. Non-technical employees must be trained on general security awareness practices such as password protection, spotting phishing attacks and recognizing social engineering. All the security controls and policies in the world will provide no protection if employees do not know how to operate the tools in a secure manner. Likewise, the strongest 42-character password with special characters, numbers, mixed case, etc. is utterly broken if an employee writes it on a sticky note attached to their monitor.

For an organization to effectively manage its own risk, it must complete a detailed risk analysis on its own environment. Risk analysis goal is to determine the threats and vulnerabilities to services performed and assets for the organization. As part of a risk assessment, organization should define critical assets including hardware, software, and sensitive information and then determine risk levels for those components. This in turn allows the organization to determine priorities for reducing risk. It is important to note that risks should be prioritized for systems that will be in-scope for PCI DSS and then other company systems and networks.

Once the risk assessment has been completed the organization should have a much clearer view of its security threats and risks and can begin determining the security posture of the organization. Policies and procedures form the foundation of any security program and comprise a large percentage of the PCI DSS requirements. Business leaders and department heads should be armed with the PCI DSS requirements and the results of the risk analysis to establish detailed security policies and procedures that address the requirements but are tailored to business processes and security controls within the organization.

Building upon the foundation of security policies, the committee of business leaders and department heads should now review the PCI DSS requirements in detail and discuss any potential compliance gaps and establish a remediation plan for closing those gaps. This is where it is important to have the full support of business leaders who can authorize necessary funds and manpower to implement any remediation activities.

This is also the time to schedule the required annual penetration testing. These are typically performed by third parties, but is not required to be performed by third parties, and can take some time to schedule, perform, and remediate (if necessary). The results of a PCI DSS assessment will be delayed until the penetration test is completed so now is the time to schedule the test.

At this point the organization is ready for a full-scale PCI DSS assessment and can now enter a maintenance mode where periodic internal audits occur and regular committee meetings are held to perform risk assessments and update policies, procedures, and security controls as necessary to respond to an ever changing threat landscape. PCI DSS must become integrated into the everyday operation of the organization so that the organization remains secure and to ease the burden of the annual assessments.

Payment Card Industry (PCI) compliance assessment is a major task for any size organization, but you can make it easier.

Posted in Best Practices for Merchants, Credit Card Security, Payment Card Industry PCI Security Tagged with: assets, card, card transactions, compliance, compliance assessment, credit card transactions, credit-card, data security standards, DSS, networks, password protection, payment, Payment Card Industry, PCI, Phishing, process, risk, risk analysis, risk assessment, secure payment, Security, security control, security policy, transactions, transmit

May 6th, 2014 by Elma Jane

Which fee structure works best remains unclear despite the recent high-profile data security breaches that are emphasizing the need for security measures. Acquirers charge fees – or not – based on what’s best for their business model and their security objectives

Some charge merchants that comply, others charge merchants that fail to comply and a few charge both. Some Independent Sales Organizations (ISOs) don’t charge merchants a fee for helping them comply with the Payment Card Industry data security standards (PCIS DSS).

If there is any trend, it’s that more banks are finding that some sort of funding is necessary to run a program that gets any results. That funding covers costs for security assessments and compliance assistance as well as internal resources for acquirers. When it comes to covering those costs and creating incentives for compliance, no one fee structure is ideal.

Non-compliance fees encourage merchants to comply so they can save money, but the fees may not accomplish that. Unless you charge exorbitantly, it’s not going to have the effect you want it to have, and by the time you charge that much, the merchant’s just going to move to a different ISO.

ISOs charging non-compliance fees often claim the fee revenue goes into an account designated for use in case of a breach. Non-compliance fees can also reward acquirers for doing nothing to increase compliance. You get this situation where a bank has a revenue stream. Their objective is not to increase the revenue stream but to increase compliance, when they increase compliance, the revenue stream goes down.

It is recommended to some acquirers that they consider charging merchants fees for doing things like storing card data, which could be checked with a scanning tool. Merchants that do store data or fail to run the scan would be charged a fee. That is something that could really decrease risk, because if you’re not storing card data, even if you are breached, there’s nothing to get.

Simplifying the compliance verification process, by making assessment questionnaires available on its merchant portal and by teaching merchants about PCI, will minimize the potential impact of fraud by increasing compliance, which saves the company money in the long run versus a more laissez-faire approach of fees without education and compliance tools.

It’s more important to educate the merchant, it’s the spirit and intent of PCI-DSS supported by the card associations. Visa and MasterCard support it because of the severe impact of a breach or other data compromise, not as a revenue source.

ISOs and other players in the payments chain that do not work to help merchants comply are also putting themselves at risk. Breached merchants may be unable to pay fines that come with a data compromise, potentially leaving ISOs responsible for paying them. Merchants that go out of business because of a data breach also stop providing the ISO with revenue.

Plus, when merchants ask why they’re being charged a non-compliance fee, point them to the questionnaire and explain that they’ll stop being charged as soon as they demonstrate they comply with PCI.

Posted in Best Practices for Merchants, Credit Card Security, Merchant Account Services News Articles, Payment Card Industry PCI Security Tagged with: card associations, card data, compliance, compliance fee, data, data security standards, ISOs, MasterCard, Merchant's, Payment Card Industry, portal, security breaches, visa

May 5th, 2014 by Elma Jane

The Payment Card Industry (PCI) Data Security Standard (DSS) has come under criticism as high profile data breaches continue to expose flaws in retailers’ data security systems. But telecommunications firm Verizon Wireless concluded that the PCI DSS is working.

Some Responses to Criticisms

Nilson Report research from August 2013 that said card fraud cost the global payments market over $11 billion in 2012. Verizon added that the frequency of fraud schemes that the PCI DSS was designed to avoid is in fact growing. And yet most businesses are not fully compliant at the time of assessment. Only 51.1 percent of the companies it had audited had passed seven of the 12 requirements of the PCI DSS and only 11.1 percent of said companies had passed all 12.

Verizon addressed some of the criticisms leveled at the PCI DSS. One concern is that the standard promotes compliance as a test to be passed and forgotten, which distracts companies from focusing on improving security. Verizon responded by stating that breached businesses were less likely to be PCI DSS compliant than unaffected companies. It also said businesses improve their chances of not being breached by having the standard in place, and of minimizing the damage of a breach should one occur.

Another common complaint leveled at the standard is that it is too cumbersome and slow moving in relation to the quickly evolving threat landscape and nimble fraudsters ready to try new tactics. Verizon countered that the PCI DSS is meant to be a set of baseline security protocols. Achieving compliance with any standard is simply not enough, organizations must take responsibility for protecting both their reputation and their customers. Most attacks on networks are of the simple variety, with 78 percent of hacking techniques considered low or very low in sophistication. Data Breach Investigations Report (DBIR) research shows that while perpetrators are upping the ante, trying new techniques and leveraging far greater resources, less than 1 percent of the breaches use tactics rated as high on the VERIS (Verizon’s Data breach Analysis Database) difficulty scale for initial compromise.

Recommendations

There’s an initial dip in compliance whenever a major update to the standard is released, so organizations will have to put in additional effort to prepare for achieving compliance with DSS 3.0.

The newest version of the standard, PCI DSS 3.0, went into effect Jan. 1, 2014. Businesses have until Jan. 1, 2015, to implement it. The updated standard has new requirements and clarifications to version 2.0 that will take time for businesses to understand and implement, and this will result in more organizations being out of compliance.

To help businesses deal with their PCI DSS compliance obligations the firm offered five approaches:

Don’t leave compliance to information technology security teams, but enlist application developers, system administrators, executives and other staff in helping further along the process.

Embed compliance in everyday business practices so that it is sustainable.

Integrate compliance programs into enterprise-wide governance, risk and compliance strategies.

Learn how to reduce the scope of organizations’ compliance responsibilities, chiefly by figuring out how to store less data on fewer systems.

Think of compliance as an opportunity to improve overall business processes, rather than as a burden.

Posted in Best Practices for Merchants, Credit card Processing, Credit Card Security, Electronic Payments, Payment Card Industry PCI Security, Visa MasterCard American Express Tagged with: attacks on networks, Breach, breached, business processes, compliance, compliant, data breach investigators, data breaches, data security systems, database, DSS, fraud schemes, global payments, hacking, information technology, Payment Card Industry, PCI, retailers, Security, security protocols, standard, system administrators, wireless

December 5th, 2013 by Elma Jane

Three key benefits mPOS can provide PSPs. mPOS:

1. Maintains A Continuity Of Operations

mPOS solutions also ease the process of accepting and approving payments, according to the white paper. By enabling face-to-face card present transactions, mPOS allows transactions to be conducted in a highly secure manner. Further, once the encrypted transaction data is decrypted securely by the PSP at the payment gateway (with no access granted to the merchant), the onward presentation of the data into the acquiring network is consistent with that used historically for traditional POS terminals.

2. Simplifies Merchant Support

Thales suggests the biggest benefit to PSPs is that mPOS reduces the variety of costs PSPs need to cover to support merchants, cutting expenses related to equipment, security and PCI DSS compliance. This, the white paper says, allows PSPs that utilize mPOS to better allocate resources toward handling higher transaction volumes and acquiring business.

3. Supports Both Magnetic Stripe and EMV Cards

Another benefit to PSPs is that mPOS, despite its recent entrance to the market, is already widely available. The white paper explains that since the mPOS revolution quickly migrated from the U.S. abroad, mPOS solutions now exist to serve the unique needs of both markets. While this means challenges for merchants operating globally, PSPs benefit from being able to address the needs of merchants who want to opt for any and all available market solutions.

Much has been said about the recent explosion of the mobile point-of-sale (mPOS) market and how micromerchants are driving this payments revolution. But, what this story doesn’t communicate effectively is that small merchants aren’t the only stakeholders benefiting from the ongoing mPOS migration.

Payment service providers (PSPs) are another member of the mPOS value chain that can gain flexibility and security through these solutions, new research from data protection solution provider Thales suggests.

“Both merchants and PSPs have operational and logistical issues with traditional POS terminals associated mainly with the highly controlled and certified environment in which they must be used,” Thales writes in its latest white paper on the topic, “mPOS: Secure Mobile Card Acceptance.”

The 27-page white paper provides an extensive overview of the ongoing POS revolution, explaining how mPOS can reduce friction and costs for merchants, illustrating how the technology works step-by-step and highlighting the roles that each stakeholder plays along the value chain.

Posted in Electronic Payments, Mobile Payments, Mobile Point of Sale, Payment Card Industry PCI Security, Point of Sale, Smartphone Tagged with: acceptance, acquiring network, card present, compliance, decrypted, DSS, emv cards, encrypted, face-to-face, magnetic stripe, merchant, micromerchants, migration, mobile card, mobile point of sale, MPOS, payment gateway, payment service providers, payments, PCI, POS, psps, secure, securely, Security, terminals, transactions