October 13th, 2014 by Elma Jane

Non-cash payments volumes are expected to increase by nearly 10% percent to reach 366 billion transactions in 2013, fueled by strong growth in developing markets and mobile payments.

Overall, more than half of global non-cash payment growth comes from developing countries despite them only making up one quarter of the market size at 93 billion transactions. China remains a relatively underdeveloped market for non-cash transactions but its population and growth rate suggest in certain conditions that it could soon outstrip the US and Euro-zone within the next five years.

China is one to watch over the coming years, with the report showing that if growth rates remain at the current high level, it could become the largest market for non-cash transactions within just five years. These soaring growth rates in key markets put pressure on the global payments arena to innovate to meet rapidly increasing consumer demand.

Increased use of tablets and smartphones is creating a convergence of e- and m- payments, posing new challenges for Payments Services Providers (PSPs). In 2015, m-payments are projected to grow at 60.8% while e-payments growth is forecast to decelerate to 15.9% annually over the next year, as more people use mobile devices to make payments.

This trend is adding to the pressure on PSPs to modernize their payments processing infrastructures, ideally based around a single integrated payments platform for corporate and retail payments and a central hub.

The growth of the industry coupled with the fast pace of new regulation requires flexibility from PSPs to adapt, initiatives such as real-time payments, pressure on card interchange fees and improved payments governance as examples of cascading regulation.

Posted in Best Practices for Merchants Tagged with: card, card interchange fees, consumer, e-payments, global payments, m-payments, Mobile Devices, Mobile Payments, Non-cash payments, payments platform, payments processing, Payments Services Providers, psps, real-time payments, retail payments, Smartphones, tablets, transactions

September 19th, 2014 by Elma Jane

MasterCard is claiming a 98% success rate for pilot trials of a biometric verification system combining both voice and facial recognition.

It recently held a closed pilot to understand the consumer experience around voice and facial recognition.

A beta mobile app was tested in an e-commerce environment on over 14,000 transactions. The test group, used both Android and iOS operating systems. The results, yielding a successful verification rate of 98%, mixing a combination of voice and facial recognition. The process usually took less than 10 seconds.

With the first wave of apps utilising Apple’s TouchID fingerprint recognition system coming to market – both US neo-bank Simple and PFM outfit Mint have shipped their first iOS upgrades to incorporate the technology. Biometric verification is beginning to gain currency among businesses and consumers as a useful tool in the fight against fraud.

The launch of Apple Pay will start to bring true scale to the next generation of payments authentication. The challenge is to take lessons from the different applications of biometrics already in place and elevate them into the next generation of authentication, not just for one platform, but for the mass market globally.

MasterCard already has first hand experience of a mass-market implementation of biometric card technology with the recent launch of the Nigerian eIDcard, which combines payment card functionality with a mix of fingerprint, facial and iris recognition.

Posted in Best Practices for Merchants, EMV EuroPay MasterCard Visa, Visa MasterCard American Express Tagged with: Android, Android and iOS operating systems, Apple Pay, Apple's TouchID, beta mobile app, biometric card, biometric card technology, biometric verification, biometric verification system, card, card technology, consumer, currency, e-commerce, facial recognition, fingerprint recognition, fingerprint recognition system, fraud, iOS, iOS operating systems, iris recognition, mass market, MasterCard, mobile app, payments authentication, platform, rate, transactions, verification rate, verification system, voice and facial recognition

September 12th, 2014 by Elma Jane

Over the last couple of years, Big Data has become a huge buzzword in the business world. Whether this data comes from social networks, purchase histories, Web browsing patterns or surveys.

The vast amount of consumer information that brands can gather and analyze has allowed them to improve and personalize their customers’ experiences. But for all the attention Big Data has received, many companies tend to forget about one application of it…Employee Engagement.

When done in the right way, tracking, analyzing and sharing employee performance metrics can be very beneficial for both you and your staff. One of the things that is very powerful is being able to analyze real-time information, boil it down into performance data and empower employees with reports from that data. If you can provide employees with data to do their job better in a succinct, actionable way, it’s very motivating.

The more Big Data can be incorporated into an intimate individual experience, the better. This demonstrates to the employee that the experience is not just off the shelf and that it is relevant to the person. This personal relevance is shown to deliver higher engagement.

Applying Big Data analytics to employees’ performance helps identify and acknowledge not only the top performers, but the struggling or unhappy workers as well.

If you want to introduce analytics technology to your employee engagement strategies, below are a few tips to help you.

Find a program that integrates with your current systems. For any new software that you implement within your company, it’s important to make the transition as seamless and simple for your employees as possible.

The software has to work where the employees work already. You can’t make them switch tasks and go to another platform to aggregate the data stream. The software should genuinely assist the end user. Your choice of software should be a grassroots decision, and you should have buy-in from your employees before you ask them to use the new system.

Consider how employees will view themselves and others. Once you introduce performance and engagement analytics into your company, you’ll have to consider how that program fits into employee relationships and workplace culture as a whole.

A company needs to take into consideration the actions of the employee’s co-workers and how to make these data points of interest to the employee. This helps to foster a respected and trusting engagement experience and data needs to be used to build trust. No matter what solution you choose, an analytics program moves you away from the traditional manual reporting process of performance measurement; helping make your staff more efficient, motivated and engaged.

Business software is in the beginning stages of being useful for performance measurement. Businesses have not pushed for innovation as hard as consumers have, but now that’s starting to change. Think about business processes in a different way and gather data in a way that matters.

Select and focus on the most important metrics.Analytics programs can pull and process data for a large number of metrics. Even when applying Big Data to customer service, many businesses struggle to keep up with the volume of information pouring in. Narrowing down your focus to only the most important key performance indicators (KPIs). Don’t introduce too many metrics, it becomes too difficult and confusing. If you can boil it down to some very simple statistics, like a score that incorporates the elements you want, everyone can focus on consolidated KPIs.

Posted in Best Practices for Merchants Tagged with: big data, Business software, consumer, customer, customer service, data, key performance indicators, program, service, social networks, software, web, Web browsing patterns

September 5th, 2014 by Elma Jane

Businesses are rapidly adopting a third-party operations model that can put payment data at risk. Today, the PCI Security Standards Council, an open global forum for the development of payment card security standards, published guidance to help organizations and their business partners reduce this risk by better understanding their respective roles in securing card data. Developed by a PCI Special Interest Group (SIG) including merchants, banks and third-party service providers, the information supplement provides recommendations for meeting PCI Data Security Standard (PCI DSS) requirement 12.8 to ensure payment data and systems entrusted to third parties are maintained in a secure and compliant manner.

Breach reports continue to highlight security vulnerabilities introduced by third parties as a leading cause of data compromise. The leading mistake organizations make when entrusting sensitive and confidential consumer information to third-party vendors is not applying the same level of rigor to information security in vendor networks as they do in their own. Per PCI DSS Requirement 12.8, if a merchant or entity shares cardholder data with a third- party service provider, certain requirements apply to ensure continued protection of this data will be enforced by such providers. The Third-Party Security Assurance Information Supplement focuses on helping organizations and their business partners achieve this by implementing a robust third-party assurance program.

Produced with the expertise and real-world experience of more than 160 organizations involved in the Special Interest Group, the guidance includes practical recommendations on how to:

Conduct due diligence and risk assessment when engaging third party service providers to help organizations understand the services provided and how PCI DSS requirements will be met for those services.

Develop appropriate agreements, policies and procedures with third-party service providers that include considerations for the most common issues that arise in this type of relationship.

Implement a consistent process for engaging third-parties that includes setting expectations, establishing a communication plan, and mapping third-party services and responsibilities to applicable PCI DSS requirements.

Implement an ongoing process for maintaining and managing third-party relationships throughout the lifetime of the engagement, including the development of a robust monitoring program.

The guidance includes high-level suggestions and discussion points for clarifying how responsibilities for PCI DSS requirements may be shared between an entity and its third-party service provider, as well as a sample PCI DSS responsibility matrix that can assist in determining who will be responsible for each specific control area.

PCI Special Interest Groups are PCI community-selected and developed initiatives that provide additional guidance and clarifications or improvements to the PCI Standards and supporting programs. As part of its initial proposal, the group also made specific recommendations that were incorporated into PCI DSS requirements 12.8 and 12.9 in version 3.0 of the standard.One of the big focus areas in PCI DSS 3.0 is security as a shared responsibility. This guidance is an excellent companion document to the standard in helping merchants and their business partners work together to protect consumers’ valuable payment information.

Posted in Best Practices for Merchants, Credit Card Security, Payment Card Industry PCI Security Tagged with: banks, Breach, card, card data, cardholder, consumer, data, data security, Merchant's, networks, payment, payment card security, payment data, payment information, PCI, PCI-DSS, provider's, Security, Security Assurance, security standards, security standards council, Service providers, services

June 23rd, 2014 by Elma Jane

How online payments can help improve health care efficacy? 76 percent of providers said that it took more than one month to collect from a patient. However, patients have made it clear that they prefer to have the option of making payments online. Consumer responsibility is also increasing, but many providers still rely on paper-based, manual payment collection and posting processes. As a result of waiting for those payments, providers are spending more money and more time to collect, yet still accumulating a large amount of bad debt.

The majority of providers 76 percent did say that they offered the option of online payments to their patients. As providers and their clients increasingly rely on consumer payments for revenue, many have started to use more consumer-centered strategies, like payment plans, to collect payments. However, they will have to implement best practices and policies, including automating payments and communications and ensuring payment data is secure, to improve collection processes.

Posted in Uncategorized Tagged with: consumer, health care, online payments, payment data, payments, provider's

June 20th, 2014 by Elma Jane

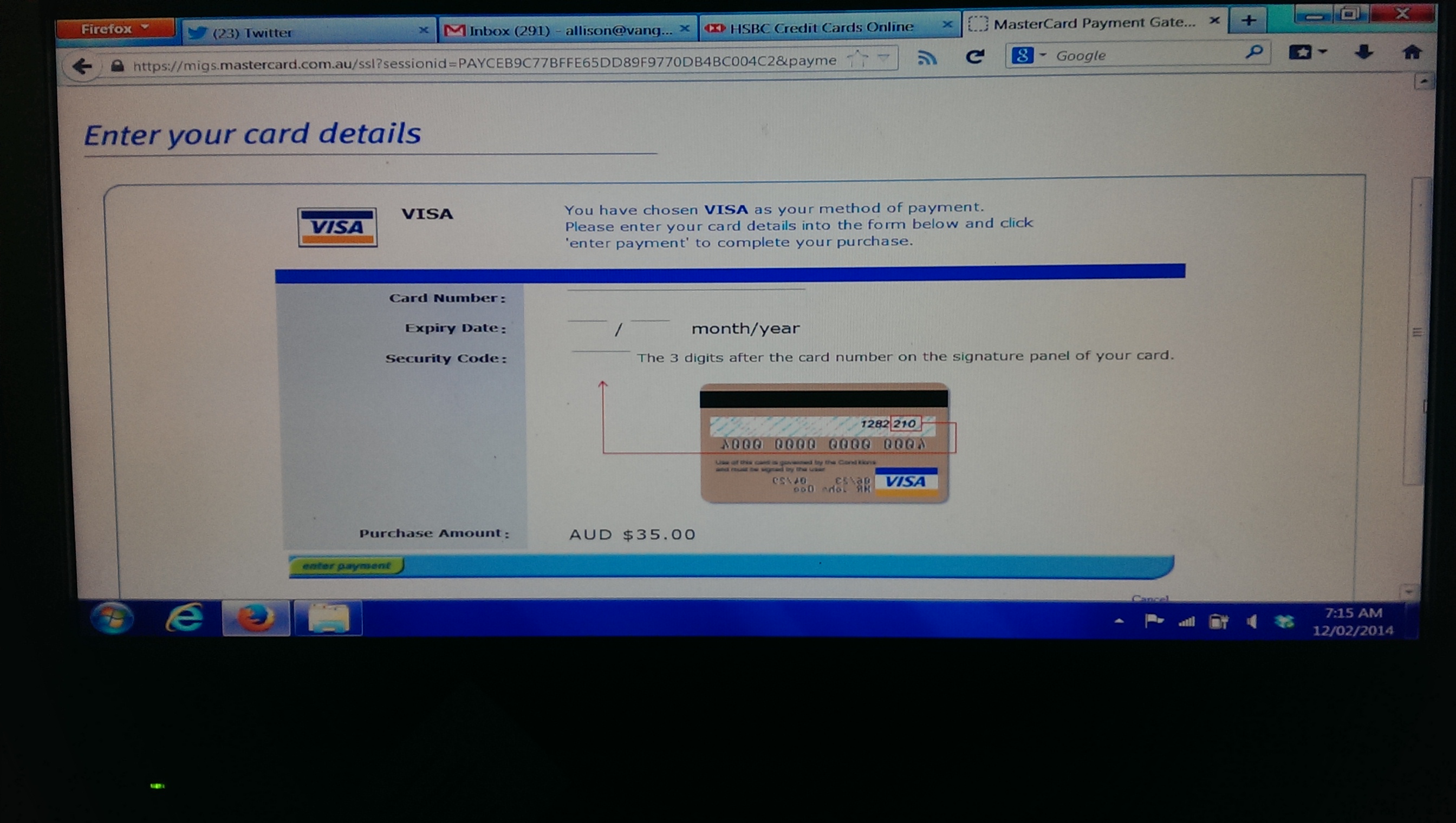

A recent survey said, 82 percent of e-commerce merchants who currently do not employ a consumer authentication solution are afraid that such solutions will scare off online shoppers, but with more and more fraud expected to migrate online in the coming years, the payments industry needs to do a better job of informing merchants why authentication in the card-not-present realm is crucial to data security.

While a majority of payment service companies employ some type of 3-D Secure online authentication, and most large merchants do likewise, the rest of the merchant population, especially in North America, apparently do not. 55 percent of merchants surveyed, a majority of which are U.S.-based, do not use online authentication, noting that North America is the only world region where less than half of merchants use the technology. The reason so many U.S. merchants eschew consumer authentication is they see it as a sales killer.

The main reason appears to be fear, uncertainty and doubt (FUD) about how consumer authentication will impact sales conversion and user experience, 43 percent of merchant respondents are FUD-preoccupied, with 20 percent concerned about the effect of the technology on sales conversion, 13 percent worried about changing the user experience and 10 percent simply want nothing to do with consumer authentication. Beyond the FUD concerns, there is also a very real perception with merchants and service providers that integration is long and difficult, adding that 21 percent of merchants who do not employ authentication, citing the time and/or cost of integration as the barrier.

End to FUD

The solution to merchant adoption of some form of 3-D Secure technology is apparently education. Many FUD concerns are related to a hangover effect caused by bad experiences with previous iterations of consumer authentication. But the report provides evidence that the FUD factor can be overcome because of the happiness factor that authentication-using merchants express. 81 percent of merchant respondents showing satisfaction with the solutions they have employed.

The report said nearly half of merchants surveyed said authentication had no effect on sales conversion, either positive or negative; however, almost 20 percent believe it has had a positive effect on sales. The positive result seems to be related to merchants who use authentication selectively, on specific transactions rather than on all of them. Additionally, the technology results in many merchants experiencing lower numbers of chargebacks. Amongst merchants, 59 percent overall say the authentication program brought a decrease in chargebacks and this is true for more than half of merchants from each geographic region.

FYI on FUD

The adoption is very low because not many people understand it. Online verification does retard the checkout process as a second screen pops up that consumers must navigate in order to proceed with the purchase. However, these barriers can be overcome with education and simply getting people comfortable with the technology. If we had this solution from day one on all e-commerce sites today nobody would be complaining because people would be used to doing it. It is a question of achieving ubiquity rather than taking a piecemeal approach to implementation. It is a matter of if you do it at one place or every place. If you have to do it at only one location that makes that site really secure. If all sites ask the same question, you get used to it.

Consumer authentication is also something that requires buy-in from issuers, acquirers and merchants. It is a participation solution where the issuer and the acquirer have to be participating in it. If you are an e-commerce site and you are certified with Verified by Visa the card brands proprietary version of 3-D Secure, if the card issuer has not embraced that, then the security will not happen.

Increasing number and frequency of breaches is slowly eroding consumers’ trust in the safety of e-commerce It’s not good for the whole ecosystem. At some point people will come back and say, this is too risky to do online transactions with cards. Before that point is reached, businesses should improve their online defenses, and consumer authentication is central to that defense. With the U.S. payments infrastructure in the process of transitioning to the Europay/MasterCard/Visa (EMV) chip card standard at the physical POS, fraud in the United States will sharpen its focus on the less secure online channel. EMV will do a lot of good in terms of card present security, but it does not do anything for card-not-present environments. So how are we going to contain the online fraud? We have to go to a 3-D Secure type solution

Posted in Best Practices for Merchants Tagged with: 3-D Secure online authentication, card, card present security, card-not-present, chargebacks, chip, chip card, consumer, data security, e-commerce, e-commerce merchants, EMV, Europay/MasterCard/Visa, fraud, Merchant's, online authentication, online channel, online fraud, online shoppers, online transactions, payment service, payments industry, POS, sales conversion, technology, Verified, visa

June 16th, 2014 by Elma Jane

Visa announced yesterday a new designation for consumer reload-able prepaid products that aims to simplify and clarify fees, step-up consumer protections and make prepaid solutions a valid tool for getting onto stronger financial footing. Consumers have been confused by an often complex prepaid landscape. As a prepaid leader, it is important to go beyond current requirements in the marketplace and bring transparency to this growing product area. This Visa designation will signify a new level of simplicity, protection and opportunity, enabling cardholders to confidently manage their spending every day.

To qualify for the Visa prepaid designation, prepaid programs must offer things like simplified fees and transparent disclosures of them. The new designation also bans some types of feeing such as transaction decline fees, customer service fees or overdraft protection (which is not to be offered) fees among others. Once designated, cards products will receive a seal that will be visible on card packaging and materials.

Visa’s efforts to raise the bar on quality in the prepaid industry by building Compass Principles are vital because millions of Americans are searching for tools to help them reduce financial friction, and prepaid cards can be a valuable option.

Posted in Best Practices for Merchants, EMV EuroPay MasterCard Visa, Visa MasterCard American Express Tagged with: consumer, customer service fees, overdraft protection fees, prepaid products, prepaid solutions, simplified fees, transaction decline fees, visa

April 7th, 2014 by Elma Jane

Business-to-business ecommerce describes Internet-enabled transactions between businesses, such as a manufacturer and a wholesaler, a wholesaler and a retailers, or a wholesaler and a business user. The B-to-B ecommerce market was expected to exceed $550 billion in the U.S. last year, offering great opportunities for distributors and manufacturers to streamline sales, boost profits, and engage with new customers.

Since the late 1990s, businesses have been using the Electronic Data Interchange (EDI) system to transfer purchase orders and similar structured information electronically, representing, if you will, a form of B-to-B ecommerce.

Separately, some B-to-B sellers have created websites on which business customers can make purchases as if they were shopping on a business-to-consumer site. This category of B-to-B ecommerce may enjoy the most growth and offer the most opportunity.

Important points to consider of running a B-to-B ecommerce site.

B-to-B Customers Are also B-to-C Customers

B-to-B sites often trail consumer sites in technology, function, capabilities, and design. Typically not good enough.

As an example, the U.S. B-to-B site for a major multinational manufacturer, which includes information for dealers in the U.S., can only be viewed on Internet Explorer, and won’t work in any other browser, including Firefox, Chrome, Opera, or Safari. And don’t even think about visiting this site on a mobile device. It just won’t work.

This is a ridiculous business decision. It forgets a fundamental fact about B-to-B ecommerce customers. They are also B-to-C ecommerce customers.

It is extremely likely that the professional shopper on an ecommerce-enabled B-to-B website has had at least some experience shopping on consumer ecommerce sites, which all have compelling product photography, good navigation, good search capabilities, and good content.

A B-to-B ecommerce site must provide the same visual and functional experience as the best B-to-C ecommerce sites.

Personalization Is Vital

B-to-B shoppers may require a greater level of personalization than B-to-C customers, since businesses may have contract prices, special payment terms, or negotiated shipping rates.

Business relationships may be very deep and complicated. It is not unusual for B-to-B ecommerce sites to require registration before showing prices or shipping rates or offering a quote. This login requirement allows the B-to-B ecommerce site to personalize almost every aspect of the transaction.

A good B-to-B ecommerce site may take a little longer to launch since the system for handling relatively complex business relationships can take some time. But once it is in place, this personalization will mean that the relationship could be longer lasting.

Sales people Are the Primary Marketing Vehicle

While it is both possible and likely that B-to-B ecommerce sites will be able to acquire new customers simply by making products easy to order online, salespeople who contact customers are probably the B-to-B ecommerce seller’s primary and best marketing channel.

Salespeople can attract new customers or deepen relationships with existing shoppers. Sometimes, it can be enough to follow up after a B-to-B sale with a call to make certain that the transaction went as expected.

Shopping Is Part of Your Customer’s Profession

One of the most significant differences between B-to-B and B-to-C ecommerce is that shopping is part of the B-to-B ecommerce customer’s daytime job.

This means that the stakes can be higher for the B-to-B seller. If the shopper has a good experience, that shopper is likely to return and reorder repeatedly – even suggesting the seller to co-workers or other divisions. But if something goes wrong, particularly something that would cause the shopper to miss deadlines at work or appear in some way to have done a poor job, that shopper will likely blame the B-to-B seller. Depending on the unhappy shopper’s influence, the B-to-B seller might lose the entire account, including many individual buyers or divisions.

This means that order handling and transactional communications must be top notch. Some B-to-B ecommerce sellers will call customers to confirm orders or shipments when the customer has ordered a large quantity, very expensive items, or requested express shipping, since these orders may represent important transactions to the customer.

What Ecommerce Can Do for your B-to-B Business

If you sell to other businesses, ecommerce should have three potential benefits for your business.

First, it may help new customers find you. Having an easy-to-find and use ecommerce site means that new customers – customers with a need – will be able to locate your business regardless of geography or prior relationships.

Second, B-to-B ecommerce may streamline sales for existing customers. Some of your current customers will appreciate the ability to order online, 24 hours a day 7 days a week. The process may also be faster than sending emails or, even worse, faxed orders.

Finally, B-to-B ecommerce may improve margins and boost profits. It may be possible to provide customers with a better ordering experience and better customer service using ecommerce while spending less on labor and order processing. Any cost savings that B-to-B ecommerce brings may drop straight to your business’s bottom line.

Posted in Credit card Processing, e-commerce & m-commerce, Electronic Payments, Internet Payment Gateway, Mobile Payments, Mobile Point of Sale, Small Business Improvement Tagged with: account, b-to-b, b-to-c, better ordering experience, boost profits, business-to-business, business-to-consumer, business's bottom line, communication, consumer, cost savings, customer service, e-commerce, ecommerce, ecommerce sites, electronic data interchange, faxed orders, growth, improve margins, new customers, online, order handling, order processing, personalization, profits, purchase orders, salespeople, seller, sending emails, shopper, special payment terms, transaction, wholesaler

December 19th, 2013 by Elma Jane

NTC’s BIG DATA

Improving Collection and Analytics tools to Create Value from Relevant Data.

Big data is a popular term used to describe the exponential growth and availability of data, both structured and unstructured. And big data may be as important to business…and society… as the Internet has become. Why? More data may lead to more accurate analyses. More accurate analyses may lead to more confident decision making, and better decisions can mean greater operational efficiencies, cost reductions and reduced risk.

With NTC Virtual Merchant product, it captures email addresses at the Point-of-Sale (POS) into a database to assist merchants and consumer stay connected, and for future Marketing.

In understanding Big Data For Merchants, NTC’s President Mark Fravel, provided a general overview of how online merchants can use Big Data. Large amounts of seemingly random data from many sources…can be used to create competitive advantages.

Necessity of Analytical Tools

Collecting Big Data is the easy part. Storing, organizing, and analyzing it is much more complex. One seam of data that several experts identify as a particularly rich, emerging source of information can be as diverse as CRM software, AdWords, and your own website. Mobile communications, including text messages and social media posts such as Facebook and Twitter. Making sense of it can be overwhelming without analytical tools. These tools facilitate the examination of large amounts of different types of data to reveal hidden patterns and correlations that are not otherwise easily discernible.

A good example is NTC, they could analyze data on visitor browsing patterns, login counts, phone calls, and responses to promotions…they can monitor to eliminate what isn’t working and focus on what does. Some of the off-the-shelf analytic solutions are so finely tuned, they can tell a vendor whether it needs to offer a 25 percent discount or if a 15 percent discount will suffice for a particular customer.

Association rule learning is another analytics method that is a good fit with Big Data. This could be, for example, a shopping cart analysis, in which a merchant can determine which products are frequently bought together and use this information for marketing purposes.

Uses of Big Data Analytics:

Big Data can be most useful in analyzing a customer’s shopping and purchasing experience, which can help a merchant in the following four ways.

Become more efficient by alerting you to merchandising efforts that are ineffective, and products that are not selling.

Encourage more purchases by presenting existing customers with complementary items to what they’ve purchased previously.

Enhance inventory management by eliminating slow-moving items and increasing the supply of fast-moving merchandise.

Example: A top marketing executive at a sizable U.S. retailer recently found herself perplexed by the sales reports she was getting. A major competitor was steadily gaining market share across a range of profitable segments. Despite a counterpunch that combined online promotions with merchandising improvements, her company kept losing ground….The competitor had made massive investments in its ability to collect, integrate, and analyze data from each store and every sales unit and had used this ability to run myriad real-world experiments. At the same time, it had linked this information to suppliers’ databases, making it possible to adjust prices in real time, to reorder hot-selling items automatically, and to shift items from store to store easily. By constantly testing, bundling, synthesizing, and making information instantly available across the organization…the rival company had become a different, far nimbler type of business.

Increase conversion rates by better identification of successful sales transactions.

Is Big Data Analysis Affordable?

NTC Data Storage is also a good alternative for small ecommerce merchants because it is relatively inexpensive and is scalable it can expand as data requirements grow.

Relying on data-driven decision-making is crucial in industries in which profit margins are slim. Amazon, which earns increasingly thin profit margins, is one of the most effective users of data analytics. As more Big Data solutions for small online businesses come to market and more online merchants incorporate Big Data into their business tool set, employing Big Data will become a necessity for all Merchants.

Using data wisely has the potential to boost margins and increase conversions for online merchants, and investors are banking on it.

This is Big Data for NTC we know WHO, WHAT,WHEN, AND WHERE a purchase took place.

Posted in Best Practices for Merchants, Credit card Processing, e-commerce & m-commerce, Electronic Payments, Internet Payment Gateway, Mobile Payments, Mobile Point of Sale, Point of Sale, Visa MasterCard American Express Tagged with: analyses, analytic, big data, communications, competitive, consumer, cost, database, decision, ecommerce, email, internet, marketing, Merchant's, mobile, monitor, ntc, online, orgainizing, patterns, point of sale, POS, profit margins, promotions, risk, scalable, solutions, storing, text messages, virtual merchant, website

December 12th, 2013 by Elma Jane

The Consumer Financial Protection Bureau is reviewing whether credit card rewards program are misleading to credit card users.

Results of the review may be new. Strict rules about the transparency of rewards programs, including details about cash back offers, mileage awards and how these rewards must be redeemed.

In an email to Bloomberg News, CFPB Director Richard Cordray said, we will be reviewing whether rewards disclosures are being made in a clear and transparent manner, and we will consider whether additional protections are needed.

Credit card issuers like American Express, Bank of America, Chase, Citi and Discover rely on rewards programs to attract new customers as well as increasing the use of their cards by existing cardholders. Rewards are the No. 1 reason why customers select the card, and there’s almost a battle to provide the highest rewards.

What we’ve learned over time is, our best customers value rewards. Their spend behaviour changes based on rewards, said Edward Gilligan, the President of American Express.

The CFPB’s restrictions could put a damper on each company’s ability to draw in new cardholders.

While there are no apparently abuse issues with rewards programs at this time, the CFPB is taking the initiative to catch a problem before it happens.

Keep an eye out for notices from your credit card issuer about changes in your rewards program. Changes, or at least clarifications, could come as a result of this examination.

Posted in Gift & Loyalty Card Processing, Visa MasterCard American Express Tagged with: American Express, Bank of America, cardholders, Chase, Citi, consumer, credit-card, Discover, financial, issuer, protection, rewards